|

市场调查报告书

商品编码

1740979

电磁地球物理服务市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Electromagnetic Geophysical Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

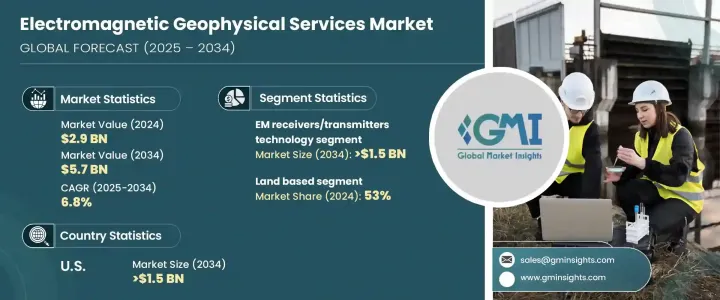

2024年,全球电磁地球物理服务市场规模达29亿美元,预计2034年将以6.8%的复合年增长率成长,达到57亿美元。这得归功于对先进地下测绘技术需求的激增,尤其是在矿物探测、地下水勘探和环境监测等领域。随着各行各业优先考虑永续开采和资源管理,对高精度地质洞察的需求比以往任何时候都更加迫切。电磁地球物理服务正迅速发展,因为它们能够实现更快、更详细、更非侵入性的地下评估。

能源转型趋势的演变、采矿活动的增加以及环境法规的日益严格,进一步推动勘探公司转向精度更高、生态影响更小的电磁勘探技术。政府在基础建设和能源安全方面的投资不断增加,也刺激了对可靠地质勘探的需求。随着各机构寻求更智慧、数据驱动的勘探解决方案,人工智慧、机器学习和进阶分析技术与电磁勘探的融合正在彻底改变地下资料的采集、处理和解释方式,为未来十年充满活力且竞争激烈的全球市场奠定基础。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 29亿美元 |

| 预测值 | 57亿美元 |

| 复合年增长率 | 6.8% |

技术创新是推动市场成长的主要催化剂,解析度、讯号清晰度和更深的地形穿透能力都有所提升。地理空间工具和资料视觉化领域的新发展正在彻底改变地质评估,使企业即使在最具挑战性的环境中也能进行更快、更准确的勘测。投资友善的监管环境以及政府推动勘探和负责任土地利用的倡议,为成熟企业和新兴企业创造了有利的环境。企业正在扩展服务组合,并组成策略合资企业以开拓新市场,力求在快速发展的市场中占据领先地位。

预计到2034年,电磁接收器和发射器市场规模将达到15亿美元。这些核心系统能够产生和探测电磁讯号,这对于绘製地下电导率变化至关重要。随着感测器灵敏度、讯号处理和传输范围的最新突破,这些仪器如今即使在复杂的地质地形中也能提供前所未有的分辨率和深度穿透能力。它们在矿产勘探、地下水探测、环境评估和地热能项目等领域的多功能性使其成为现代勘探工作中不可或缺的工具。

2024年,陆基电磁勘探占据了53%的市场份额,预计到2034年将以6.5%的复合年增长率成长。其无与伦比的灵活性、可扩展性和成本效益使其成为矿产勘探、基础设施规划和环境修復项目的首选。便携式接收器、行动资料系统和无人机辅助勘探等创新技术正在进一步提升其在大型区域勘探和特定场地研究中的有效性。

2024年,美国电磁地球物理服务市场规模达9.532亿美元。人工智慧驱动的资料处理和三维地震成像技术正在提升地下探测能力,同时扩大海上勘探活动,从而推动对海上勘探的需求成长。然而,关税波动推高了感测器等关键进口零件的成本,导致利润率收紧,并减缓了一些创新投资。

塑造全球竞争格局的主要参与者包括 PGS、SLB、Geotech、西门子、TGS、Spectrem Air、Applus+、CGG、EGS、Ramboll Group、Weatherford、Fugro、Abitibi Geophysics、SkyTEM、AKS Geoscience、Paradigm Group、中海油田服务股份有限公司和 Dawson Geophysical。领先的公司专注于策略联盟、强大的研发投入以及数位转型计划,例如基于云端的处理和机器学习集成,以在全球范围内提供经济高效、高解析度的勘探解决方案。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 监管格局

- 川普政府关税对贸易和整体产业的影响

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 战略仪表板

- 创新与永续发展格局

第五章:市场规模及预测:依技术分类,2021 - 2034 年

- 主要趋势

- 电磁接收器/发射器

- 时域/频域非均质模型

- 大地电磁法(MT)

- 其他的

第六章:市场规模及预测:依调查类型,2021 - 2034 年

- 主要趋势

- 陆基

- 以海洋为基础

- 空中

第七章:市场规模及预测:依最终用途,2021 - 2034

- 主要趋势

- 石油和天然气

- 矿业

- 农业

- 其他的

第八章:市场规模及预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 挪威

- 俄罗斯

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 中东和非洲

- 阿联酋

- 沙乌地阿拉伯

- 伊拉克

- 伊朗

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第九章:公司简介

- Abitibi Geophysics

- AKS Geoscience

- Applus

- CGG

- China Oilfield Services

- Dawson Geophysical

- EGS

- Fugro

- Geotech

- Paradigm Group

- PGS

- Ramboll Group

- Siemens

- SkyTEM

- SLB

- Spectrem Air

- TGS

- Weatherford

The Global Electromagnetic Geophysical Services Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 5.7 billion by 2034, driven by the surging demand for advanced subsurface mapping technologies, particularly across industries focusing on mineral detection, groundwater exploration, and environmental monitoring. As industries prioritize sustainable extraction and resource management, the need for highly accurate geological insights has become more critical than ever. Electromagnetic geophysical services are gaining rapid traction as they enable faster, more detailed, and non-invasive subsurface assessments.

Evolving energy transition trends, heightened mining activities, and stricter environmental regulations are further pushing exploration companies toward electromagnetic surveying techniques that offer enhanced precision with reduced ecological impact. Rising government investments in infrastructure development and energy security are also fueling demand for reliable geological surveys. As organizations seek smarter, data-driven exploration solutions, the integration of AI, machine learning, and advanced analytics into electromagnetic surveys is transforming how subsurface data is captured, processed, and interpreted, setting the stage for a dynamic and highly competitive global market over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 6.8% |

Technological innovation is a major catalyst propelling market growth, with improvements in resolution, signal clarity, and deeper terrain penetration capabilities. New developments in geospatial tools and data visualization are revolutionizing geological assessments, allowing companies to conduct faster, more accurate surveys even in the most challenging environments. Investment-friendly regulatory environments and government initiatives promoting exploration and responsible land use are creating a favorable climate for both established companies and emerging players. Firms are expanding service portfolios and forming strategic joint ventures to tap into new markets, positioning themselves as leaders in a rapidly evolving landscape.

The electromagnetic receivers and transmitters segment is expected to reach USD 1.5 billion by 2034. These core systems generate and detect electromagnetic signals critical for mapping subsurface conductivity variations. With recent breakthroughs in sensor sensitivity, signal processing, and transmission range, these instruments are now capable of delivering unprecedented resolution and depth penetration, even in complex geological terrains. Their versatility across mineral exploration, groundwater detection, environmental assessments, and geothermal energy projects has made them indispensable tools for modern exploration efforts.

Land-based electromagnetic surveys held a commanding 53% market share in 2024 and are projected to grow at a CAGR of 6.5% through 2034. Their unmatched flexibility, scalability, and cost efficiency make them the preferred choice for mineral exploration, infrastructure planning, and environmental remediation projects. Innovations like portable receivers, mobile data systems, and drone-assisted surveys are further enhancing their effectiveness across large regional surveys and targeted site-specific studies.

The United States Electromagnetic Geophysical Services Market generated USD 953.2 million in 2024. AI-driven data processing and 3D seismic imaging are advancing subsurface detection capabilities while expanding offshore exploration activities, which are driving higher demand for marine-based surveys. However, tariff fluctuations have raised the costs of critical imported components such as sensors, tightening margins and slowing down some innovation investments.

Major players shaping the global competitive landscape include PGS, SLB, Geotech, Siemens, TGS, Spectrem Air, Applus+, CGG, EGS, Ramboll Group, Weatherford, Fugro, Abitibi Geophysics, SkyTEM, AKS Geoscience, Paradigm Group, China Oilfield Services, and Dawson Geophysical. Leading firms focus on strategic alliances, robust R&D investments, and digital transformation initiatives like cloud-based processing and machine learning integration to deliver cost-effective, high-resolution survey solutions worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Impact of Trump administration tariffs on trade & overall industry

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's Analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL Analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 EM receivers/transmitters

- 5.3 TDEM/FDEM

- 5.4 Magnetotellurics (MT)

- 5.5 Others

Chapter 6 Market Size and Forecast, By Survey Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Land based

- 6.3 Marine based

- 6.4 Aerial based

Chapter 7 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Oil & gas

- 7.3 Mining

- 7.4 Agriculture

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Norway

- 8.3.5 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 Iraq

- 8.5.4 Iran

- 8.5.5 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Abitibi Geophysics

- 9.2 AKS Geoscience

- 9.3 Applus

- 9.4 CGG

- 9.5 China Oilfield Services

- 9.6 Dawson Geophysical

- 9.7 EGS

- 9.8 Fugro

- 9.9 Geotech

- 9.10 Paradigm Group

- 9.11 PGS

- 9.12 Ramboll Group

- 9.13 Siemens

- 9.14 SkyTEM

- 9.15 SLB

- 9.16 Spectrem Air

- 9.17 TGS

- 9.18 Weatherford

2026年全球地球物理服务市场报告2026年全球综合地球物理服务市场报告

2026年全球地球物理服务市场报告2026年全球综合地球物理服务市场报告 全球电磁物理勘探服务市场规模、份额、趋势和成长分析报告(2026-2034年)

全球电磁物理勘探服务市场规模、份额、趋势和成长分析报告(2026-2034年) 地球实体服务市场 - 全球产业规模、份额、趋势、竞争预测、机会(按技术、类型、服务、最终用户、地区和竞争格局划分),2021-2031年地球实体设备市场-全球产业规模、份额、趋势、机会及预测(按设备类型、最终用户、服务类型、研究、地区和竞争格局划分,2021-2031年)磁力地球物理服务市场-全球产业规模、份额、趋势、机会、预测:按技术、研究类型、最终用户、地区和竞争格局划分,2021-2031年

地球实体服务市场 - 全球产业规模、份额、趋势、竞争预测、机会(按技术、类型、服务、最终用户、地区和竞争格局划分),2021-2031年地球实体设备市场-全球产业规模、份额、趋势、机会及预测(按设备类型、最终用户、服务类型、研究、地区和竞争格局划分,2021-2031年)磁力地球物理服务市场-全球产业规模、份额、趋势、机会、预测:按技术、研究类型、最终用户、地区和竞争格局划分,2021-2031年 地球实体服务市场规模、份额和成长分析(按技术、类型、最终用户和地区划分)—2026-2033年产业预测

地球实体服务市场规模、份额和成长分析(按技术、类型、最终用户和地区划分)—2026-2033年产业预测 地球实体服务市场:依服务类型、测量类型、应用和最终用途划分-2025-2032年全球预测地球实体软体服务市场-全球产业规模、份额、趋势、机会和预测(细分、按调查类型、按应用、按部署类型、按地区和竞争,2020-2030 年预测)

地球实体服务市场:依服务类型、测量类型、应用和最终用途划分-2025-2032年全球预测地球实体软体服务市场-全球产业规模、份额、趋势、机会和预测(细分、按调查类型、按应用、按部署类型、按地区和竞争,2020-2030 年预测) 全球地球实体软体服务市场:2032 年预测 - 按软体类型、服务类型、部署方法、应用程式、最终用户和地区进行分析

全球地球实体软体服务市场:2032 年预测 - 按软体类型、服务类型、部署方法、应用程式、最终用户和地区进行分析