|

市场调查报告书

商品编码

1741027

脑血氧监测市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Cerebral Oximetry Monitoring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

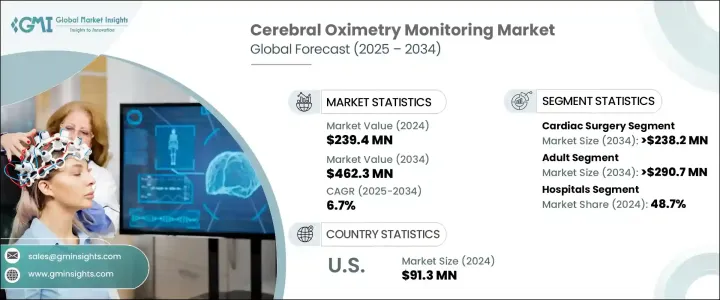

2024 年全球脑血氧监测市场价值为 2.394 亿美元,预计到 2034 年将以 6.7% 的复合年增长率成长至 4.623 亿美元。这一增长轨迹是由全球外科手术数量的增加和神经系统疾病盛行率的上升所驱动的。随着全球人口老化和与年龄相关的疾病变得越来越普遍,对有助于确保病患安全(尤其是在高风险临床环境中)的先进非侵入性监测解决方案的需求日益增长。随着越来越多的医疗保健提供者重视避免脑血氧去饱和和改善手术效果,脑血氧监测系统已成为现代手术室和重症监护病房的重要组成部分。技术创新和先进监测设备的引入进一步推动了应用,而对患者护理标准的意识提高继续增强了市场潜力。医院现在优先考虑整合脑氧监测技术,以防止复杂手术期间的神经损伤,患者也越来越多地寻求提供这些先进护理解决方案的机构。

老化人口中心血管和神经系统疾病的发生率不断上升,是该市场最重要的成长动力之一。随着预期寿命的延长,外科手术的需求也随之成长,尤其是需要脑功能监测的手术。脑血氧仪可在手术过程中提供即时回馈,使医护人员能够快速回应脑部氧合程度的变化。此外,全球手术数量的激增,尤其是涉及心臟和血管系统的手术,也带来了对这些监测系统的持续需求。手术方案的变化以及医疗专业人员对患者监测技术日益增长的支持,也为市场的扩张增添了动力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 2.394亿美元 |

| 预测值 | 4.623亿美元 |

| 复合年增长率 | 6.7% |

从应用角度来看,脑血氧监测主要用于心臟和血管手术等。仅心臟手术领域,预计复合年增长率将达到6.6%,到2034年将超过2.382亿美元。由于使用人工心肺机有脑灌注降低的潜在风险,因此在心臟手术中,脑氧监测尤其重要。随着外科手术方法的日益先进,确保手术过程中脑部氧合不间断变得越来越重要,这直接推动了对脑血氧仪的需求。

依年龄层分析,市场分为成人和儿童两部分。成人市场预计复合年增长率为6.4%,到2034年底市场规模预计将超过2.907亿美元。中风、心臟併发症和神经退化性疾病等成人特有疾病的发生率不断上升,这推动了脑部监测在医疗过程中的应用。此外,用于成人脑部监测的新型血氧仪的监管审批和上市也进一步促进了该领域的成长。

就终端用户而言,医院占据脑血氧监测市场的最大份额,占2024年总收入的48.7%。医院的主导地位源于其专科护理的可及性以及在手术和重症监护期间使用高端监测系统的优势。医院越来越多地采用脑血氧监测工具,以满足复杂手术的需求并提高病人安全标准。这些机构不仅拥有必要的基础设施,还吸引了那些在医疗过程中寻求最高水准护理和技术支援的患者。需要密切监测的医院和诊所就诊人数的增加,持续推动着该领域的发展。

从地区来看,美国在该领域仍占据主导地位。 2023年,美国脑血氧监测市场规模为8,550万美元,2024年将增加至9,130万美元。预计2025年至2034年期间,美国脑血氧监测市场的复合年增长率将达到5.9%。推动这一强劲成长的因素包括庞大的老龄化人口、先进的医疗基础设施以及领先医疗器械公司的存在。此外,美国还受益于大量的外科手术、对病人安全的高度重视以及支持采用创新技术的优惠医疗政策。

脑血氧监测产业整合程度适中,前五大厂商占约55%至60%的市占率。由于参与者数量有限,市场呈现可控竞争的特征,占主导地位的公司往往专注于特定的技术领域。许多主要厂商正在投资新产品开发,而其他厂商则透过收购和合作扩大业务范围。各厂商透过在其设备中提供差异化功能以及瞄准采用率仍在增长的新兴市场来定位自身。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 神经系统疾病盛行率不断上升

- 脑血氧仪的技术进步

- 病人安全和脑部去氧饱和意识不断增强

- 非侵入性脑监测系统需求不断成长

- 产业陷阱与挑战

- 测量波动且缺乏准确性

- 设备成本高

- 成长动力

- 成长潜力分析

- 监管格局

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 技术格局

- 差距分析

- 波特的分析

- PESTEL分析

- 价值链分析

- 使用脑血氧仪监测脑缺血的展望

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 心臟手术

- 血管外科

- 其他应用

第六章:市场估计与预测:依年龄组,2021 年至 2034 年

- 主要趋势

- 成人

- 儿科

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 门诊手术中心

- 其他最终用途

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- CASMED

- Edwards

- GE HealthCare

- HAMAMATSU

- Honeywell

- Masimo

- Medtronic

- Mespere LIFE SCIENCES

- mindray

- NIHON KOHDEN

- NONIN

- sentec

- TERUMO

The Global Cerebral Oximetry Monitoring Market was valued at USD 239.4 million in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 462.3 million by 2034. This growth trajectory is driven by a rising number of surgical procedures worldwide and an increasing prevalence of neurological conditions. With the global population aging and age-related medical conditions becoming more common, there is a growing demand for advanced non-invasive monitoring solutions that help ensure patient safety, especially in high-risk clinical settings. As more healthcare providers place an emphasis on avoiding cerebral desaturation and improving surgical outcomes, cerebral oximetry monitoring systems have become an essential component of modern operating rooms and intensive care units. Technological innovations and the introduction of sophisticated monitoring devices are further fueling adoption, while greater awareness of patient care standards continues to enhance market potential. Hospitals are now prioritizing the integration of brain oxygen monitoring technologies to prevent neurological damage during complex surgeries, and patients are increasingly seeking out institutions that offer these advanced care solutions.

The increasing frequency of cardiovascular and neurological disorders among the aging population is one of the most significant growth drivers in this market. As life expectancy rises, so does the need for surgical interventions, particularly those requiring brain function monitoring. Cerebral oximeters provide real-time feedback during procedures, allowing medical professionals to respond quickly to changes in brain oxygenation levels. In addition, the surge in global surgeries-especially those involving the heart and vascular system-creates an ongoing demand for these monitoring systems. Changes in surgical protocols and growing support for patient monitoring technologies among healthcare professionals are also adding momentum to this market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $239.4 Million |

| Forecast Value | $462.3 Million |

| CAGR | 6.7% |

From an application standpoint, cerebral oximetry monitoring is primarily used in cardiac and vascular surgeries, among other uses. The cardiac surgery segment alone is forecast to grow at a CAGR of 6.6%, reaching over USD 238.2 million by 2034. The need for brain oxygen monitoring is particularly critical during heart operations due to the potential risk of reduced brain perfusion when a heart-lung machine is used. As surgical approaches become more advanced, ensuring uninterrupted brain oxygenation during these procedures becomes more essential, which directly boosts the demand for cerebral oximeters.

When analyzed by age group, the market is divided into adult and pediatric segments. The adult segment is anticipated to experience a CAGR of 6.4%, with a market value expected to surpass USD 290.7 million by the end of 2034. The increasing incidence of adult-specific conditions, including stroke, cardiac complications, and neurodegenerative diseases, is encouraging the use of cerebral monitoring during medical procedures. Additionally, the regulatory clearance and availability of new oximetry devices for adult brain monitoring further contribute to segment growth.

In terms of end users, hospitals hold the largest share of the cerebral oximetry monitoring market, accounting for 48.7% of total revenue in 2024. Their dominance stems from the availability of specialized care and the use of high-end monitoring systems during surgeries and critical care. Hospitals are increasingly adopting cerebral oximetry tools to meet the demands of complex procedures and elevate patient safety standards. These facilities not only have the necessary infrastructure but also attract patients who are seeking the highest levels of care and technological support during medical treatment. The increase in hospital and clinic visits for conditions requiring intensive monitoring continues to propel the segment forward.

Regionally, the United States remains a dominant player in this space. The cerebral oximetry monitoring market in the US was valued at USD 85.5 million in 2023 and rose to USD 91.3 million in 2024. Between 2025 and 2034, the market in the US is expected to grow at a CAGR of 5.9%. Factors contributing to this robust growth include a large aging population, advanced healthcare infrastructure, and the presence of leading medical device companies. The US also benefits from a high volume of surgical procedures, a strong focus on patient safety, and favorable healthcare policies supporting the adoption of innovative technologies.

The cerebral oximetry monitoring industry is moderately consolidated, with the top five players controlling roughly 55% to 60% of the market. With only a limited number of participants, the market shows characteristics of controlled competition, where dominant companies tend to specialize in specific technological niches. Many major players are investing in new product development, while others are expanding their reach through acquisitions and partnerships. Companies are positioning themselves by offering differentiated features in their devices and by targeting emerging markets where adoption rates are still growing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of neurological disorders

- 3.2.1.2 Technological advancements in cerebral oximeters

- 3.2.1.3 Growing awareness regarding patient safety and cerebral desaturation

- 3.2.1.4 Rising demand for non-invasive brain monitoring systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuation and lack of accuracy in measurement

- 3.2.2.2 High cost of devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Value chain analysis

- 3.11 Outlook on monitoring cerebral ischemia using cerebral oximetry

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiac surgery

- 5.3 Vascular surgery

- 5.4 Other applications

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 CASMED

- 9.2 Edwards

- 9.3 GE HealthCare

- 9.4 HAMAMATSU

- 9.5 Honeywell

- 9.6 Masimo

- 9.7 Medtronic

- 9.8 Mespere LIFE SCIENCES

- 9.9 mindray

- 9.10 NIHON KOHDEN

- 9.11 NONIN

- 9.12 sentec

- 9.13 TERUMO