|

市场调查报告书

商品编码

1750265

两轮车悬吊系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Two-Wheeler Suspension System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

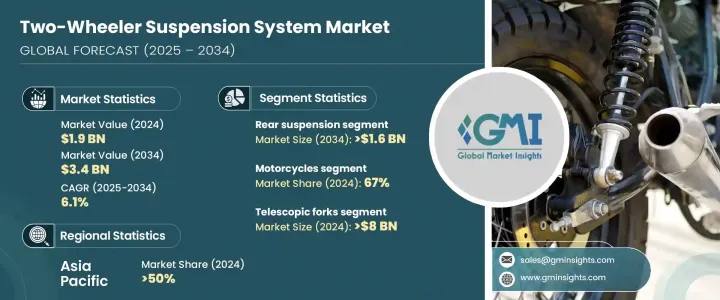

2024年,全球两轮车悬吊系统市场规模达19亿美元,预计2034年将以6.1%的复合年增长率成长,达到34亿美元。这主要得益于发展中国家两轮车使用量的持续成长。这些国家的城市密度不断上升、公共交通选择有限,以及中等收入人口的不断增长,使得人们强烈偏好经济实惠且省油的出行解决方案。随着个人交通在城市和半城市地区蓬勃发展,对耐用高性能悬吊系统的需求也日益增长。驾驶者希望获得更平稳的操控性、更舒适的驾驶体验和更佳的安全性,因此製造商优先考虑能够满足监管标准和不断变化的用户期望的悬吊创新。

前后悬吊技术的演变——尤其是向先进的单减震器装置、轻量化材料和电子控制系统的转变——正在塑造市场。消费者的选择性越来越强,要求系统能够提供更好的驾驶动态,尤其是在维护不良的道路上。随着对配备精良悬吊部件的中檔和通勤两轮车的需求不断增长,各公司正将重点转向提供更具适应性的解决方案。能够根据地形或速度自动调整的智慧悬吊正在成为一种性能提升功能,吸引着注重安全的用户。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 19亿美元 |

| 预测值 | 34亿美元 |

| 复合年增长率 | 6.1% |

前后悬吊系统在提升整体驾驶体验方面继续发挥着至关重要的作用,其中后悬吊单元在市场上占据着显着的领先地位。 2024年,后悬吊市场规模达10亿美元,预计2034年将达到16亿美元。这一增长归功于这些单位在吸收道路衝击、确保驾驶舒适度和提高车辆稳定性方面的重要作用,尤其是在基础设施欠发达的地区。在欠发达的城市和半城市地区,道路经常磨损,后悬吊系统对于减少不平路面对整体驾驶品质的影响至关重要。

2024年,摩托车在两轮车悬吊系统市场的占有率为67%。由于製造商越来越多地将单减震后悬吊整合到中阶车型中,预计该领域将保持领先地位。这些系统曾经仅限于高性能摩托车,如今已应用于日常使用的摩托车,以提升操控性、转弯性能和道路舒适度。对性能、燃油效率和价格实惠的重视促使原始设备製造商重新校准减震器系统,以满足日常通勤者在崎岖地形中行驶的需求。

2024年,亚太地区两轮车悬吊系统市场占50%的市场份额,其中中国占主导地位。中国庞大的两轮车用户群体,加上严重的城市交通拥堵,推动了对高性能悬吊系统的需求。随着城市交通量的增加,两轮车因其经济实惠和操控性而成为个人出行的必备工具。日益壮大的中产阶级正在寻求经济高效的出行解决方案,这进一步推动了对可靠悬吊系统的需求成长。在此背景下,悬吊系统不仅对安全性至关重要,而且对于提供舒适稳定的驾驶体验也至关重要,使其成为两轮车设计和製造的关键特性。

KYB、Endurance Technologies、Showa、Gabriel India、WP Suspension、Mando、Tenneco、Fox Factory、BITUBO 和重庆川动避震器等领先的市场参与者正在透过专注的研发投入、策略合作和新产品的推出来提升其市场地位。这些公司不断完善其产品线,为不同等级的摩托车提供更强大的悬吊性能。许多公司优先考虑轻量化、耐用的材料和电子自适应解决方案。与原始设备製造商 (OEM) 和售后市场供应商的合作使企业能够强化其分销管道,而全球扩张策略和技术差异化则有助于他们在不断变化的出行格局中保持竞争力。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 原物料供应商

- 零件製造商

- OEM (原始设备製造商)

- 技术提供者

- 售后市场供应商和经销商

- 川普政府关税的影响

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 主要材料价格波动

- 供应链重组

- 价格传导至终端市场

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 对贸易的影响

- 利润率分析

- 技术与创新格局

- 重要新闻和倡议

- 成本細項分析

- 定价分析

- 产品

- 地区

- 专利分析

- 监管格局

- 衝击力

- 成长动力

- 新兴经济体对两轮车的需求不断增长

- 悬吊系统的技术进步

- 更加重视骑士的安全和舒适度

- 相较于短途航班,人们越来越倾向选择公路旅行

- 产业陷阱与挑战

- 新兴市场的价格敏感度

- 跨模型的标准化有限

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依暂停分类,2021 - 2034 年

- 主要趋势

- 前悬吊

- 后悬吊

第六章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 伸缩叉

- 单震

- 双减震器

- 弹簧和避震器单元

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 摩托车

- 踏板车

- 电动两轮车

第八章:市场估计与预测:依销售管道,2021 - 2034 年

- 主要趋势

- OEM (原始设备製造商)

- 售后市场

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第十章:公司简介

- BITUBO

- Chongqing Chuandong Shock Absorber

- Duro Shox

- Endurance Technologies

- Fox Factory

- Fras-le

- Gabriel

- Hagon Shocks

- JRi Shocks

- K-Tech Suspension

- KYB

- Mando

- Matris Dampers

- Norton Motorcycle

- Penske Racing Shocks

- Showa

- Tenneco

- Touratech

- WP Suspension

- ZF Friedrichshafen

The Global Two-Wheeler Suspension System Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 3.4 billion by 2034, driven by rising two-wheeler usage across developing nations, where increasing urban density, limited public transit options, and a growing middle-income population have created a strong preference for affordable and fuel-efficient mobility solutions. As personal transportation gains momentum in urban and semi-urban areas, the demand for durable and high-performance suspension systems is climbing. Riders want smoother handling, enhanced comfort, and improved safety, leading manufacturers to prioritize suspension innovations that meet regulatory standards and evolving user expectations.

The evolution of rear and front suspension technologies-especially the shift toward advanced mono-shock setups, lightweight materials, and electronically controlled systems-helps shape the market. Consumers are becoming more selective, demanding systems that offer better ride dynamics, particularly on poorly maintained roads. As demand grows for mid-range and commuter two-wheelers with refined suspension components, companies are shifting their focus to provide more adaptable solutions. Intelligent suspensions that adjust automatically to terrain or speed are emerging as performance-enhancing features that appeal to safety-conscious users.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 6.1% |

Front and rear suspension systems continue to play a crucial role in enhancing the overall riding experience, with rear suspension units taking a significant lead in the market. In 2024, the rear suspension segment generated USD 1 billion, with projections indicating that this value will reach USD 1.6 billion by 2034. This growth is attributed to the vital function these units serve in absorbing road shocks, ensuring rider comfort, and improving vehicle stability, especially in regions with underdeveloped infrastructure. In less-developed urban and semi-urban areas, where roads often face wear and tear, rear suspension systems are essential for reducing the impact of rough surfaces on the overall ride quality.

The Motorcycles segment in the two-wheeler suspension system market held 67% share in 2024. This segment is expected to maintain its leadership, thanks to manufacturers increasingly integrating mono-shock rear suspension into mid-segment models. These systems, once reserved for high-performance bikes, are now featured in daily-use motorcycles to improve handling, cornering, and road comfort. The emphasis on performance, fuel efficiency, and affordability has pushed OEMs to recalibrate shock absorber systems for everyday commuters navigating rugged terrains.

Asia Pacific Two-Wheeler Suspension System Market held 50% share in 2024, with China leading the way. The large population of two-wheeler users in China, paired with heavy urban congestion, has driven the demand for high-performance suspension systems. As urban traffic increases, two-wheelers have become an essential mode of personal transportation due to their affordability and maneuverability. The growing middle class, which is seeking cost-effective mobility solutions, has further contributed to the increased demand for reliable suspension systems. In this context, suspension systems are critical not just for safety but also for offering a comfortable and stable ride, making them a key feature in two-wheeler design and manufacturing.

Leading market players like KYB, Endurance Technologies, Showa, Gabriel India, WP Suspension, Mando, Tenneco, Fox Factory, BITUBO, and Chongqing Chuandong Shock Absorber are advancing their market positions through focused R&D investments, strategic collaborations, and new product rollouts. These companies refine their product lines to offer enhanced suspension performance for various motorcycle classes. Many are prioritizing lightweight, durable materials and electronically adaptive solutions. Partnerships with OEMs and aftermarket suppliers allow firms to strengthen their distribution channels, while global expansion strategies and technological differentiation help them remain competitive in an evolving mobility landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 OEM (Original Equipment Manufacturers)

- 3.2.4 Technology providers

- 3.2.5 Aftermarket suppliers and distributors

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on the Industry

- 3.3.2.1 Price volatility in key materials

- 3.3.2.2 Supply chain restructuring

- 3.3.2.3 Price transmission to end markets

- 3.3.3 Strategic industry responses

- 3.3.3.1 Supply chain reconfiguration

- 3.3.3.2 Pricing and product strategies

- 3.3.1 Impact on trade

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Cost breakdown analysis

- 3.8 Pricing analysis

- 3.8.1 Product

- 3.8.2 Region

- 3.9 Patent analysis

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Growing demand for two-wheelers in emerging economies

- 3.11.1.2 Technological advancements in suspension systems

- 3.11.1.3 Increasing focus on rider safety and comfort

- 3.11.1.4 Increasing preference for road-based travel over short-haul flights

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 Price sensitivity in emerging markets

- 3.11.2.2 Limited standardization across models

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Suspension, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Front suspension

- 5.3 Rear suspension

Chapter 6 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Telescopic forks

- 6.3 Mono shock

- 6.4 Twin shock absorbers

- 6.5 Spring and damper units

Chapter 7 Market Estimates & Forecast, By Vehicles, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Motorcycles

- 7.3 Scooters

- 7.4 Electric two-wheelers

Chapter 8 Market Estimates & Forecast, By Sales Channels, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM (Original Equipment Manufacturers)

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 BITUBO

- 10.2 Chongqing Chuandong Shock Absorber

- 10.3 Duro Shox

- 10.4 Endurance Technologies

- 10.5 Fox Factory

- 10.6 Fras-le

- 10.7 Gabriel

- 10.8 Hagon Shocks

- 10.9 JRi Shocks

- 10.10 K-Tech Suspension

- 10.11 KYB

- 10.12 Mando

- 10.13 Matris Dampers

- 10.14 Norton Motorcycle

- 10.15 Penske Racing Shocks

- 10.16 Showa

- 10.17 Tenneco

- 10.18 Touratech

- 10.19 WP Suspension

- 10.20 ZF Friedrichshafen

摩托车悬吊系统市场:按悬吊类型、组件和型号划分 - 全球市场预测 2026-2032摩托车悬吊售后市场(按悬吊类型、分销管道、摩托车类型、悬吊技术和最终用户划分),全球预测,2026-2032年摩托车电子悬吊市场按车辆类型、分销管道、最终用户和动力类型划分,全球预测(2026-2032年)

摩托车悬吊系统市场:按悬吊类型、组件和型号划分 - 全球市场预测 2026-2032摩托车悬吊售后市场(按悬吊类型、分销管道、摩托车类型、悬吊技术和最终用户划分),全球预测,2026-2032年摩托车电子悬吊市场按车辆类型、分销管道、最终用户和动力类型划分,全球预测(2026-2032年) 摩托车悬吊系统市场规模、份额、成长率及全球市场分析:按类型、应用和地区划分,并提供2026-2034年的洞察和预测

摩托车悬吊系统市场规模、份额、成长率及全球市场分析:按类型、应用和地区划分,并提供2026-2034年的洞察和预测 两轮车悬吊系统市场-全球产业规模、份额、趋势、机会和预测,按悬吊、产品、车辆、销售通路、地区和竞争细分,2020-2030 年

两轮车悬吊系统市场-全球产业规模、份额、趋势、机会和预测,按悬吊、产品、车辆、销售通路、地区和竞争细分,2020-2030 年 摩托车悬吊系统市场报告:趋势、预测和竞争分析(至 2031 年)

摩托车悬吊系统市场报告:趋势、预测和竞争分析(至 2031 年) 2024-2028年马达悬吊系统全球市场

2024-2028年马达悬吊系统全球市场