|

市场调查报告书

商品编码

1750268

呋喃基聚合物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Furan-based Polymer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

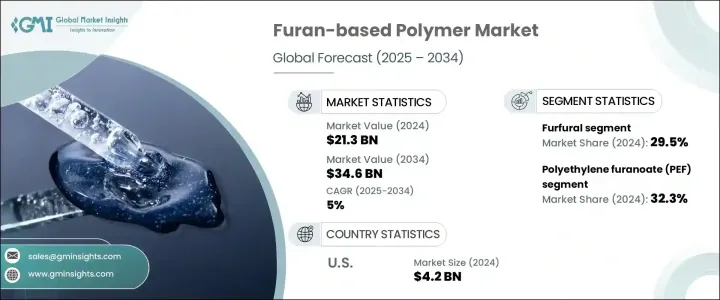

2024年,全球呋喃基聚合物市场规模达213亿美元,预计到2034年将以5%的复合年增长率成长,达到346亿美元。生物衍生聚合物主要由再生资源生产,例如玉米芯和甘蔗渣等农业废弃物。由糠醛和5-羟甲基糠醛(HMF)等中间体生产的呋喃基聚合物因其可持续性以及与全球环保材料趋势的契合而日益受到关注。

呋喃基聚合物已在各行各业中广泛应用,尤其是在食品和饮料行业,它们作为传统包装材料的可持续替代品正日益受到欢迎。与石油基塑胶相比,这些聚合物是更环保的选择,因为它们源自于农业废弃物等可再生资源。它们的使用符合消费者和监管机构日益增长的对绿色产品和包装解决方案的追求。除了永续性之外,呋喃基聚合物还具有出色的耐热性,使其成为在极端条件下需要高耐久性应用的理想选择。在铸造等行业中,这些聚合物尤其重要。例如,呋喃树脂因其耐高温且性能稳定而被广泛用于砂型铸造型芯的黏合。其极低的毒性和稳定的热性能使其成为精密铸造金属生产和其他高性能应用的必备材料。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 213亿美元 |

| 预测值 | 346亿美元 |

| 复合年增长率 | 5% |

聚呋喃甲酸乙二醇酯 (PEF) 的需求尤其强劲,到 2024 年,该聚合物细分市场将占据 32.3% 的市场份额。 PEF 的可回收性、阻隔性和生物基特性使其成为食品和饮料包装中聚对苯二甲酸乙二醇酯 (PET) 的理想替代品。另一个值得关注的应用是涂料和复合材料,其中聚糠醇的耐腐蚀性确保了其在化学加工等行业的稳定需求。呋喃基聚酰胺因其耐用性、强度以及增强的热稳定性(进而提高燃油效率)而越来越多地应用于汽车製造。

糠醛市场细分领域涵盖5-羟甲基糠醛 (HMF)、糠醛、糠醇和2,5-呋喃二甲酸 (FDCA) 等衍生物,其中糠醛占据主导地位,2024年市场份额达29.5%。糠醛广泛应用于树脂、溶剂和润滑剂等工业领域,使其成为市场基石。利用农业残留物生产糠醛符合更广泛的生物经济目标,即减少对不可再生资源的依赖。

2024年,美国呋喃基聚合物市场产值达42亿美元。美国对生物经济政策、现代化生物精炼系统以及不断增加的公私投资的重视,为呋喃基聚合物的发展创造了一个良好的环境。美国市场也受到美国农业部「生物优先计画」(BioPreferred Program)等计画的推动,该计画鼓励使用生物基产品,使呋喃基聚合物成为寻求永续解决方案的行业具有竞争力且经济可行的选择。

Avantium、Bitrez、Swicofil、Sulzer和圣泉集团等公司处于呋喃基聚合物市场的前沿。这些公司正在采取各种策略来增强其市场地位,包括投资先进的生物精炼技术以及扩大其可再生基材料的生产能力。 Avantium和Bitrez专注于扩大生物基聚合物的生产规模并提高其成本效益,而Swicofil和圣泉集团则透过策略合作伙伴关係扩大其市场覆盖范围。 Sulzer正在透过整合满足各行各业需求的可持续解决方案来增强其产品组合。这些公司正在共同推动创新,并加速呋喃基聚合物在全球的应用。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 贸易统计(HS编码)

- 主要出口国

- 主要进口国

註:以上贸易统计仅针对重点国家。

- 利润率分析

- 重要新闻和倡议

- 技术进步与创新

- 监管格局

- 全球生物基聚合物法规

- 生物基材料的国际标准

- ASTM标准

- ISO 标准

- EN标准

- 生物降解性和可堆肥性标准

- 区域监理框架

- 环境法规

- 碳足迹法规

- 废弃物管理法规

- 报废处理法规

- 监管影响分析

- 对产品开发的影响

- 对市场进入障碍的影响

- 对定价策略的影响

- 衝击力

- 成长动力

- 柔性电子和穿戴式科技的应用日益广泛

- 扩大储能设备的应用,特别是超级电容器和全聚合物电池

- 汽车应用需求不断成长,尤其是电动车的成长

- 人们对智慧纺织品和生物医学应用的兴趣日益浓厚

- 产业陷阱与挑战

- 原料供应变化

- 来自成熟聚合物的竞争

- 监管障碍

- 市场机会

- 对永续材料的需求不断增长

- 包装产业转型

- 政府支持和激励措施

- 企业永续发展承诺

- 新兴应用程式开发

- 技术进步

- 成长动力

- 成长潜力分析

- 2021 - 2034 年价格分析(美元/吨)

- 影响定价的因素

- 原料成本

- 能源成本

- 生产规模

- 技术成熟度

- 市场竞争

- 石油基替代品定价

- 影响定价的因素

- 产业趋势和最终用途偏好

- 转向可持续材料

- 包装产业趋势

- 汽车产业趋势

- 建筑业趋势

- 消费品趋势

- 波特的分析

- PESTEL分析

- 价值链分析

- COVID-19对市场的影响

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司热图分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

- Expansion

- Mergers & acquisition

- Collaborations

- New product launches

- Research & development

- 竞争格局

- 市场集中度分析

- 竞争定位和策略

- 合併、收购和策略伙伴关係

- 新产品发布和创新

- 行销和促销策略

- 主要参与者的最新发展和影响分析

- 公司分类

- 参与者概述

- 财务表现

- 来源基准测试

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 聚呋喃甲酸乙二醇酯(PEF)

- 聚糠醇(PFA)

- 呋喃树脂

- 聚(2,5-呋喃二甲醚琥珀酸酯)(PFS)

- 呋喃基聚酯

- 呋喃基聚酰胺

- 其他的

第六章:市场估计与预测:按衍生性商品,2021 - 2034

- 主要趋势

- 5-羟甲基糠醛(HMF)

- 2,5-呋喃二甲酸(FDCA)

- 糠醛

- 糠醇

- 其他的

第七章:市场估计与预测:依生物质原料来源,2021 - 2034 年

- 主要趋势

- 农业残留物

- 林业残留物

- 食物浪费

- 甘蔗渣

- 玉米棒

- 其他的

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 包装

- 瓶子和容器

- 薄膜和层压板

- 食品包装

- 饮料包装

- 其他的

- 复合材料

- 汽车复合材料

- 建筑复合材料

- 航太复合材料

- 海洋复合材料

- 其他的

- 涂料和黏合剂

- 工业涂料

- 木器涂料

- 木製品用黏合剂

- 其他的

- 铸造厂

- 砂黏合剂

- 模具和型芯製造

- 其他的

- 纺织品和纤维

- 技术纺织品

- 服饰

- 其他的

- 汽车

- 内装部件

- 引擎盖下

- 外部元件

- 其他的

- 电子产品

- 电路板

- 电子元件

- 其他的

- 医疗保健

- 医疗器材

- 医药包装

- 其他的

- 其他的

- 农业

- 消费品

- 新兴应用

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- AVA Biochem

- Avantium

- Bitrez

- Globe Carbon Industries

- KANTO CHEMICAL

- Origin Materials

- Penn A Kem

- Shengquan Group

- Sulzer

- Swicofil

- TransFurans Chemicals

The Global Furan-based Polymer Market was valued at USD 21.3 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 34.6 billion by 2034, as bio-derived polymers are primarily produced from renewable sources such as agricultural residues, including corn cobs and sugarcane bagasse. Furan-based polymers, produced from intermediates like furfural and 5-hydroxymethylfurfural (HMF), are gaining traction due to their sustainability and alignment with the global trend towards eco-friendly materials.

Furan-based polymers have seen significant adoption in various industries, especially in the food and beverage sector, where they are becoming increasingly popular as sustainable alternatives to conventional packaging materials. These polymers offer a more environmentally friendly option compared to petroleum-based plastics, as they are derived from renewable resources like agricultural residues. Their use aligns with the growing consumer and regulatory push for greener products and packaging solutions. In addition to their sustainability, furan-based polymers also boast impressive thermal resistance, making them ideal for applications that require high durability in extreme conditions. In industries like the foundry sector, these polymers are particularly valuable. Furan resins, for example, are widely used in sand casting core binding due to their ability to withstand high temperatures without compromising performance. Their minimal toxicity and stable thermal properties make them essential in the production of precision casting metals and other high-performance applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Billion |

| Forecast Value | $34.6 Billion |

| CAGR | 5% |

The demand for polyethylene furanoate (PEF) is particularly strong, with this polymer segment accounting for a 32.3% share in 2024. PEF's recyclability, barrier properties, and bio-based nature make it a favorable alternative to polyethylene terephthalate (PET) in food and beverage packaging. Another notable application is in coatings and composites, where polyfurfuryl alcohol's resistance to corrosion ensures its stable demand in industries like chemical processing. Furan-based polyamides are increasingly being used in automotive manufacturing due to their durability, strength, and ability to enhance thermal stability, which in turn boosts fuel efficiency.

The market is segmented by derivatives such as 5-hydroxymethylfurfural (HMF), furfural, furfuryl alcohol, and 2,5-furandicarboxylic acid (FDCA), with furfural leading the segment, holding 29.5% share in 2024. Furfural's extensive use in industrial applications like resins, solvents, and lubricants has positioned it as a cornerstone in the market. Its production from agricultural residues aligns with the broader bioeconomy goals of reducing dependency on non-renewable resources.

United States Furan-based Polymer Market generated USD 4.2 billion in 2024. The country's focus on bioeconomy policies, modern biorefinery systems, and increasing public-private funding has fostered a supportive environment for the growth of furan-based polymers. The U.S. market is also driven by programs like the USDA's BioPreferred Program, which encourages the use of biobased products, making furan-based polymers a competitive and economically viable option for industries seeking sustainable solutions.

Companies like Avantium, Bitrez, Swicofil, Sulzer, and Shengquan Group are at the forefront of the furan-based polymer market. These companies are adopting various strategies to strengthen their market presence, including investments in advanced biorefinery technologies and expanding their production capabilities for renewable-based materials. Avantium and Bitrez are focused on scaling up the production of bio-based polymers and improving their cost-effectiveness, while Swicofil and Shengquan Group are expanding their market reach through strategic partnerships. Sulzer is enhancing its product portfolio by incorporating sustainable solutions that cater to a variety of industrial sectors. Together, these companies are driving innovation and accelerating the adoption of furan-based polymers globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Technological advancements and innovations

- 3.7 Regulatory landscape

- 3.7.1 Global bio-based polymers regulations

- 3.7.2 International standards for bio-based materials

- 3.7.2.1 ASTM standards

- 3.7.2.2 ISO standards

- 3.7.2.3 EN standards

- 3.7.2.4 Biodegradability and compostability standards

- 3.7.3 Regional regulatory frameworks

- 3.7.4 Environmental regulations

- 3.7.4.1 Carbon footprint regulations

- 3.7.4.2 Waste management regulations

- 3.7.4.3 End-of-life disposal regulations

- 3.7.5 Regulatory impact analysis

- 3.7.5.1 Impact on product development

- 3.7.5.2 Impact on market entry barriers

- 3.7.5.3 Impact on pricing strategies

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising adoption in flexible electronics and wearable technology

- 3.8.1.2 Expanding applications in energy storage devices, particularly supercapacitors and all-polymer batteries

- 3.8.1.3 Increasing demand in automotive applications, especially with the growth of electric vehicles

- 3.8.1.4 Growing interest in smart textiles and biomedical applications

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Feedstock supply variability

- 3.8.2.2 Competition from established polymers

- 3.8.2.3 Regulatory hurdles

- 3.8.3 Market opportunities

- 3.8.3.1 Growing demand for sustainable materials

- 3.8.3.2 Packaging industry transformation

- 3.8.3.3 Government support and incentives

- 3.8.3.4 Corporate sustainability commitments

- 3.8.3.5 Emerging applications development

- 3.8.3.6 Technological advancements

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Pricing analysis (USD/Tons) 2021 - 2034

- 3.10.1 Factors affecting pricing

- 3.10.1.1 Raw material costs

- 3.10.1.2 Energy costs

- 3.10.1.3 Production scale

- 3.10.1.4 Technology maturity

- 3.10.1.5 Market competition

- 3.10.1.6 Petroleum-based alternatives pricing

- 3.10.1 Factors affecting pricing

- 3.11 Industry trends and end use preferences

- 3.11.1 Shift towards sustainable materials

- 3.11.2 Packaging industry trends

- 3.11.3 Automotive industry trends

- 3.11.4 Construction industry trends

- 3.11.5 Consumer goods trends

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Value chain analysis

- 3.15 Impact of COVID-19 on the market

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Company heat map analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Competitive landscape

- 4.7.1 Market concentration analysis

- 4.7.2 Competitive positioning and strategies

- 4.7.3 Mergers, acquisitions, and strategic partnerships

- 4.7.4 New product launches and innovations

- 4.7.5 Marketing and promotional strategies

- 4.8 Recent developments & impact analysis by key players

- 4.8.1 Company categorization

- 4.8.2 Participant’s overview

- 4.8.3 Financial performance

- 4.9 Source benchmarking

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene furanoate (PEF)

- 5.3 Polyfurfuryl alcohol (PFA)

- 5.4 Furan resins

- 5.5 Poly(2,5-furandimethylene succinate) (PFS)

- 5.6 Furan-based polyesters

- 5.7 Furan-based polyamides

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Derivatives , 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 5-Hydroxymethylfurfural (HMF)

- 6.3 2,5-Furandicarboxylic acid (FDCA)

- 6.4 Furfural

- 6.5 Furfuryl alcohol

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Biomass Feedstock Source, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Agricultural residues

- 7.3 Forestry residues

- 7.4 Food waste

- 7.5 Sugarcane bagasse

- 7.6 Corn cobs

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Packaging

- 8.2.1 Bottles and containers

- 8.2.2 Films and laminates

- 8.2.3 Food packaging

- 8.2.4 Beverage packaging

- 8.2.5 Others

- 8.3 Composites

- 8.3.1 Automotive composites

- 8.3.2 Construction composites

- 8.3.3 Aerospace composites

- 8.3.4 Marine composites

- 8.3.5 Others

- 8.4 Coatings and adhesives

- 8.4.1 Industrial coatings

- 8.4.2 Wood coatings

- 8.4.3 Adhesives for wood products

- 8.4.4 Others

- 8.5 Foundry

- 8.5.1 Sand binders

- 8.5.2 Mold and core making

- 8.5.3 Others

- 8.6 Textiles and Fibers

- 8.6.1 Technical Textiles

- 8.6.2 Apparel

- 8.6.3 Others

- 8.7 Automotive

- 8.7.1 Interior components

- 8.7.2 Under-the-hood

- 8.7.3 Exterior components

- 8.7.4 Others

- 8.8 Electronics

- 8.8.1 Circuit boards

- 8.8.2 Electronic components

- 8.8.3 Others

- 8.9 Medical and healthcare

- 8.9.1 Medical devices

- 8.9.2 Pharmaceutical packaging

- 8.9.3 Others

- 8.10 Others

- 8.10.1 Agriculture

- 8.10.2 Consumer goods

- 8.10.3 Emerging applications

- 8.10.4 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AVA Biochem

- 10.2 Avantium

- 10.3 Bitrez

- 10.4 Globe Carbon Industries

- 10.5 KANTO CHEMICAL

- 10.6 Origin Materials

- 10.7 Penn A Kem

- 10.8 Shengquan Group

- 10.9 Sulzer

- 10.10 Swicofil

- 10.11 TransFurans Chemicals