|

市场调查报告书

商品编码

1750279

传染病治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Infectious Disease Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

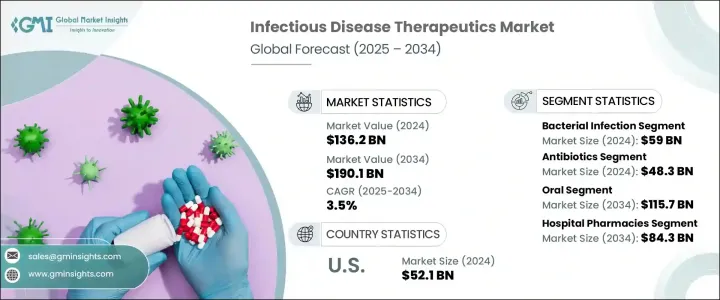

2024年,全球传染病治疗市场规模达1,362亿美元,预计到2034年将以3.5%的复合年增长率成长,达到1,901亿美元,这得益于全球传染病发病率的不断上升。针对细菌、病毒感染、真菌和寄生虫病等感染性疾病的治疗手段正得到更广泛的应用,尤其是在人口增长和医疗保健覆盖面不断扩大的情况下。这些疗法包括抗菌药物和疫苗,它们透过针对病因或增强免疫力来治疗或预防疾病。

此外,人畜共通传染病由动物传播给人类日益普遍,导致全球医疗体系的治疗需求激增。都市化、森林砍伐和密集畜牧业等因素导致这些感染的发生率上升。值得注意的是,爱滋病毒等逆转录病毒疾病的全球持续负担,持续催生了对先进抗病毒疗法的强劲需求,从而巩固了市场的上升势头。随着宣传活动的有效性和诊断技术的进步,早期检测率正在不断攀升。这一趋势,加上成熟经济体和发展中经济体医疗基础设施和保险覆盖范围的扩大,正在加速人们获得治疗的途径,并推动市场稳步成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1362亿美元 |

| 预测值 | 1901亿美元 |

| 复合年增长率 | 3.5% |

2024年,细菌感染领域产值达590亿美元。细菌性疾病易感性增加,很大程度上与营养不良、久坐不动的生活方式、人口老化以及糖尿病和癌症等慢性疾病的流行导致的免疫系统受损有关。在世界许多地区,尤其是在中低收入国家,卫生设施不足、水源污染以及食品卫生标准低下,持续加剧了细菌病原体的传播。这些因素构成了持续的医疗保健挑战,刺激了对有效抗生素、联合疗法和下一代治疗方案的持续需求。

2024年,抗生素市场规模达483亿美元。这些药物仍是治疗常见及严重细菌性疾病的基石。然而,传统抗生素抗药性的日益加剧,促使人们寻求新的治疗方案和下一代抗生素的开发。抗药性菌株的治疗难度越来越大,这使得药物创新和更广泛的抗菌药物研发管道更加紧迫。

2024年,美国传染病治疗市场规模达521亿美元。多种因素巩固了这一领先地位,包括老龄人口增长、抗菌素抗药性病原体的传播以及强劲的创新生态系统。医疗保健产业对先进生物製剂和标靶病原体免疫疗法开发的持续投资,进一步提升了美国的市场地位。治疗平台(尤其是疫苗研发和交付)的科学突破,塑造了疾病的预防和治疗策略。

全球传染病治疗市场的主要公司正优先考虑研发创新、策略合作伙伴关係和监管审批,以扩大其产品供应和全球影响力。辉瑞和吉利德科学正在推进mRNA和抗病毒疗法,而默克和葛兰素史克则正在加强疫苗研究。罗氏製药和强生公司继续投资标靶生物製剂和下一代抗病毒药物。赛诺菲和阿斯特捷利康正在与研究机构合作,以加速药物开发。诺华和拜耳正致力于透过收购和授权协议来实现产品组合多元化。同时,山德士国际和勃林格殷格翰则利用生物相似药途径来增强其竞争优势。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 传染病发生率上升

- 创新疗法的不断发展

- 诊断技术的进步

- 产业陷阱与挑战

- 抗生素抗药性导致治疗费用高昂

- 严格的监管审批

- 成长动力

- 成长潜力分析

- 监管格局

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 管道分析

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按感染类型,2021 - 2034 年

- 主要趋势

- 细菌感染

- 病毒感染

- 逆转录病毒感染(HIV/AIDS)

- 流感

- 肝炎

- 其他病毒感染

- 霉菌感染

- 寄生虫感染

第六章:市场估计与预测:按药物类型,2021 - 2034 年

- 主要趋势

- 抗生素

- 抗病毒药物

- 抗真菌药物

- 抗寄生虫药

- 疫苗

- 免疫疗法

第七章:市场估计与预测:按管理模式,2021 - 2034 年

- 主要趋势

- 口服

- 肠外

- 鼻内

第八章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 网路药局

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Abbott Laboratories

- AstraZeneca

- Bayer

- Boehringer Ingelheim International

- Bristol-Myers Squibb

- F. Hoffmann-La Roche

- Gilead Sciences

- GlaxoSmithKline (GSK)

- Johnson & Johnson (Janssen Pharmaceuticals)

- Merck

- Novartis

- Pfizer

- Sandoz International

- Sanofi

The Global Infectious Disease Therapeutics Market was valued at USD 136.2 billion in 2024 and is estimated to grow at a CAGR of 3.5% to reach USD 190.1 billion by 2034, driven by the increasing occurrence of infectious diseases globally. Treatments targeting infectious conditions from bacterial and viral infections to fungal and parasitic diseases are seeing wider adoption, particularly as populations grow and healthcare access expands. These therapies include antimicrobial drugs and vaccines that treat or prevent illnesses by targeting the root cause or strengthening immunity.

Additionally, zoonotic infections transmitted from animals to humans are becoming increasingly common, driving a surge in treatment requirements across global healthcare systems. Factors such as urbanization, deforestation, and intensified livestock farming contribute to the rising incidence of these infections. Notably, the persistent global burden of retroviral diseases like HIV continues to create a strong demand for advanced antiviral therapies, reinforcing the market's upward trajectory. As awareness campaigns grow more effective and diagnostic technologies improve, early detection rates are climbing. This trend, coupled with the expansion of healthcare infrastructure and insurance coverage in both mature and developing economies, is accelerating access to treatment and fueling steady market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $136.2 Billion |

| Forecast Value | $190.1 Billion |

| CAGR | 3.5% |

In 2024, the bacterial infections segment generated USD 59 billion. The increased vulnerability to bacterial illnesses is largely tied to compromised immune systems resulting from poor nutrition, sedentary lifestyles, aging populations, and the prevalence of chronic diseases such as diabetes and cancer. In many parts of the world, particularly in low- and middle-income countries, inadequate sanitation facilities, contaminated water sources, and insufficient food hygiene standards continue to amplify the spread of bacterial pathogens. These conditions create persistent healthcare challenges, spurring consistent demand for effective antibiotics, combination therapies, and next-generation treatment solutions.

The antibiotics segment generated USD 48.3 billion in 2024. These medications remain the cornerstone in managing common and serious bacterial conditions. However, the increasing resistance to traditional antibiotics has triggered a push for novel therapeutic solutions and next-generation antibiotic development. Drug-resistant strains are becoming more difficult to treat, which places greater urgency on pharmaceutical innovation and broader antimicrobial pipelines.

United States Infectious Disease Therapeutics Market generated USD 52.1 billion in 2024. Several factors have reinforced this leadership, including a growing elderly population, the spread of antimicrobial-resistant pathogens, and robust innovation ecosystems. The healthcare sector's continued investment in the development of advanced biologics and pathogen-targeted immunotherapies further enhances the country's market standing. Scientific breakthroughs in treatment platforms, especially in vaccine development and delivery, shape disease prevention and treatment strategies.

Key companies in the Global Infectious Disease Therapeutics Market are prioritizing R&D innovation, strategic partnerships, and regulatory approvals to expand their product offerings and global reach. Pfizer and Gilead Sciences are advancing mRNA and antiviral therapies, while Merck and GlaxoSmithKline are enhancing vaccine research. F. Hoffmann-La Roche and Johnson & Johnson continue to invest in targeted biologics and next-gen antivirals. Sanofi and AstraZeneca are collaborating with research institutions to accelerate drug development. Novartis and Bayer are focusing on portfolio diversification through acquisitions and licensing agreements. Meanwhile, Sandoz International and Boehringer Ingelheim leverage biosimilar pathways to strengthen their competitive edge.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidences of infectious diseases

- 3.2.1.2 Increasing development of innovative therapeutics

- 3.2.1.3 Advancement in diagnostic technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs due to antimicrobial resistance

- 3.2.2.2 Stringent regulatory approvals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Infection Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Bacterial infection

- 5.3 Viral infection

- 5.3.1 Retroviral infection(HIV/AIDS)

- 5.3.2 Influenza

- 5.3.3 Hepatitis

- 5.3.4 Other viral infections

- 5.4 Fungal infection

- 5.5 Parasitic infection

Chapter 6 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Antibiotics

- 6.3 Antivirals

- 6.4 Antifungals

- 6.5 Antiparasitic

- 6.6 Vaccines

- 6.7 Immunotherapies

Chapter 7 Market Estimates and Forecast, By Mode of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Parenteral

- 7.4 Intranasal

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 AstraZeneca

- 10.3 Bayer

- 10.4 Boehringer Ingelheim International

- 10.5 Bristol-Myers Squibb

- 10.6 F. Hoffmann-La Roche

- 10.7 Gilead Sciences

- 10.8 GlaxoSmithKline (GSK)

- 10.9 Johnson & Johnson (Janssen Pharmaceuticals)

- 10.10 Merck

- 10.11 Novartis

- 10.12 Pfizer

- 10.13 Sandoz International

- 10.14 Sanofi

感染疾病治疗市场:2026-2032年全球市场预测(依药物类别、给药途径、适应症、最终用户和分销管道划分)

感染疾病治疗市场:2026-2032年全球市场预测(依药物类别、给药途径、适应症、最终用户和分销管道划分) 感染疾病治疗市场分析及预测(至2035年):依类型、产品、服务、技术、应用、最终使用者、设备、流程及解决方案划分

感染疾病治疗市场分析及预测(至2035年):依类型、产品、服务、技术、应用、最终使用者、设备、流程及解决方案划分 感染疾病药物市场规模、份额和成长分析(按类型、治疗方法和地区划分)—2026-2033年产业预测

感染疾病药物市场规模、份额和成长分析(按类型、治疗方法和地区划分)—2026-2033年产业预测 传染病治疗市场-全球产业规模、份额、趋势、机会和预测,依疾病类型、最终用途、地区和竞争格局划分,2020-2030年预测

传染病治疗市场-全球产业规模、份额、趋势、机会和预测,依疾病类型、最终用途、地区和竞争格局划分,2020-2030年预测 2032 年感染疾病药物市场预测:按感染疾病类型、药物类别、给药方式、分销管道、最终用户和地区进行的全球分析

2032 年感染疾病药物市场预测:按感染疾病类型、药物类别、给药方式、分销管道、最终用户和地区进行的全球分析 感染疾病药物市场规模、份额、趋势分析报告:按感染疾病、药物类别、分销管道、地区、细分市场预测,2025-2030 年

感染疾病药物市场规模、份额、趋势分析报告:按感染疾病、药物类别、分销管道、地区、细分市场预测,2025-2030 年 2030 年中东和非洲传染病治疗市场预测 - 区域分析 - 按药物类别、适应症、给药途径和配销通路

2030 年中东和非洲传染病治疗市场预测 - 区域分析 - 按药物类别、适应症、给药途径和配销通路 2030 年亚太地区传染病治疗市场预测 - 区域分析 - 按药物类别、适应症、给药途径和配销通路

2030 年亚太地区传染病治疗市场预测 - 区域分析 - 按药物类别、适应症、给药途径和配销通路 2030 年北美传染病治疗市场预测 - 区域分析 - 按药物类别、适应症、给药途径和配销通路

2030 年北美传染病治疗市场预测 - 区域分析 - 按药物类别、适应症、给药途径和配销通路 2030 年欧洲传染病治疗市场预测 - 区域分析 - 按药物类别、适应症、给药途径和配销通路

2030 年欧洲传染病治疗市场预测 - 区域分析 - 按药物类别、适应症、给药途径和配销通路