|

市场调查报告书

商品编码

1750302

固定剂量复合式吸入器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Fixed-dose Combination Inhalers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

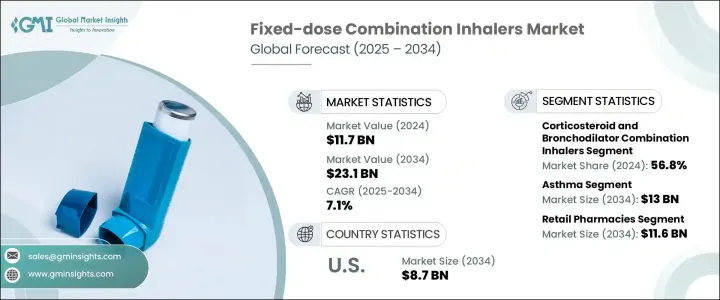

2024 年全球固定剂量复合吸入器市值为 117 亿美元,预计到 2034 年将以 7.1% 的复合年增长率成长至 231 亿美元。这些吸入器透过单一设备以预设比例输送两种或两种以上的活性药物成分,为管理慢性呼吸系统疾病的患者提供简化的方法。随着气喘和慢性阻塞性肺病 (COPD) 等呼吸系统疾病在全球日益流行,对联合疗法的需求显着增长。不断发展的临床指南、医生越来越严格地遵守联合治疗方案、越来越多的监管部门批准以及吸入器技术的进步进一步推动了这一趋势。由于呼吸系统疾病需要持续和长期的管理,特别是在中度至重度病例中,与使用多个单独的吸入器相比,固定剂量吸入器提供了更高的便利性和依从性。

国际临床指南的更新也推动了向联合疗法的转变,指南现在建议即使症状轻微的患者也使用联合吸入器。这导致所有严重程度的吸入器使用量均显着上升。这些固定剂量吸入器透过皮质类固醇消炎,同时使用支气管扩张剂改善气流,进而增强治疗效果。单一设备给药的便利性在提高处方治疗依从性方面发挥关键作用。随着慢性呼吸系统疾病负担的加重,医疗保健提供者正在优先考虑联合疗法,以提供更好的临床疗效并最大限度地降低病情恶化的风险。市场也受益于吸入器设计的持续创新,这些创新简化了患者和照护者的使用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 117亿美元 |

| 预测值 | 231亿美元 |

| 复合年增长率 | 7.1% |

就组合类型而言,市场分为皮质类固醇和支气管扩张剂组合吸入器、长效β受体激动剂 (LABA) 和吸入性皮质类固醇 (ICS) 吸入器、三联组合吸入器以及其他组合。 2024 年,皮质类固醇和支气管扩张剂组合吸入器占据了最大的收入份额,达到 56.8%,这得益于临床广泛倾向于将这些剂型用于治疗持续性呼吸道症状。这些吸入器在减少呼吸道发炎和改善气流方面尤其有效,而这对于气喘和慢性阻塞性肺病 (COPD) 的治疗至关重要。双重作用不仅可以改善症状控制,还可以减少对急救药物的需求,使其成为医疗保健提供者的首选。

根据适应症,市场细分为气喘、慢性阻塞性肺病和其他疾病。气喘领域在2024年占据最大份额,为57.4%,预计到2034年将达到130亿美元的市场价值。全球气喘确诊人数不断增加,尤其是儿童气喘患者,显着增强了该领域的市场主导地位。气喘是一种慢性復发性疾病,即使在症状稳定期间也常常需要持续治疗。这推动了固定剂量吸入器的重复购买,并支持了持续的收入成长。此外,按需使用复方吸入器的临床方法的更新扩大了符合条件的患者群体,进一步推动了该领域的成长。

这些吸入器的分销主要透过零售药局、医院药局和线上药局进行。其中,零售药局占据市场主导地位,预计到2034年其价值将达到116亿美元。慢性呼吸系统疾病需要定期补充药物,而零售药局提供的便利性和可近性正是满足这些持续需求的关键。它们遍布城乡地区,确保患者能够轻鬆获得处方并获得药剂师咨询,从而提高患者依从性并支持市场稳定成长。

从区域来看,北美继续保持领先市场地位,其中美国占据主导地位。 2024年,美国固定剂量复方吸入器市场规模达45亿美元,预计2034年将成长至87亿美元。气喘和慢性阻塞性肺病(COPD)的高发生率,以及患者对临床治疗方案的严格遵从性,正在推动市场需求。美国医师遵循实证治疗策略,优先考虑复方吸入器,因此处方率较高。此外,遍布全国的药房网路提高了产品的可及性和续药便利性,从而促进了复方吸入器使用率的提高。

全球市场呈现寡占格局,少数几家关键企业主导竞争格局。四大製药公司占据了约75%的市场份额,它们拥有强大的呼吸产品组合和设备专业知识。这些公司持续大力投资研发,以维持竞争优势。同时,仿製药和区域性製造商正透过提供经济高效的替代品,满足价格敏感人群的需求,在新兴经济体中逐渐获得青睐。此外,由于吸入器设备的创新,这些产品提高了可用性并改善了患者疗效,市场也越来越倾向于每日一次的给药方案和三重疗法。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 气喘和慢性呼吸系统疾病发生率不断上升

- 支持使用联合疗法的有利指南

- 吸入器技术的进步

- 联合吸入疗法的认可度不断提高

- 产业陷阱与挑战

- 固定剂量组合吸入器成本高

- 与不当使用和副作用相关的担忧

- 成长动力

- 成长潜力分析

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 技术格局

- 未来市场趋势

- 差距分析

- 专利分析

- 监管格局

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按组合,2021 - 2034 年

- 主要趋势

- 皮质类固醇和支气管扩张剂复合式吸入器

- 长效β受体激动剂和吸入性皮质类固醇复合式吸入器

- 三重组合

- 其他组合

第六章:市场估计与预测:按适应症,2021 - 2034 年

- 主要趋势

- 气喘

- 慢性阻塞性肺病

- 其他适应症

第七章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 零售药局

- 医院药房

- 网路药局

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 日本

- 中国

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- AstraZeneca

- Boehringer Ingelheim

- Chiesi Farmaceutici

- Cipla

- GlaxoSmithKline

- Glenmark Pharmaceuticals

- Hikma Pharmaceuticals

- Lupin

- Mylan (Viatris)

- Novartis

- Orion

- Sun Pharmaceutical Industries

- Teva Pharmaceuticals

- Vectura Group

- Zydus Group

The Global Fixed-Dose Combination Inhalers Market was valued at USD 11.7 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 23.1 billion by 2034. These inhalers deliver two or more active pharmaceutical ingredients in a pre-set ratio through a single device, offering a streamlined approach for patients managing chronic respiratory conditions. With respiratory illnesses like asthma and chronic obstructive pulmonary disease (COPD) becoming more prevalent globally, the demand for combination therapies has grown significantly. This trend is further propelled by evolving clinical guidelines, growing physician adherence to combination treatment protocols, increasing regulatory approvals, and advancements in inhaler technologies. As respiratory conditions require consistent and long-term management, particularly in moderate to severe cases, fixed-dose inhalers offer enhanced convenience and compliance compared to using multiple separate inhalers.

The shift toward combination therapies is also influenced by updates in international clinical guidelines, which now recommend combination inhalers even for patients with mild symptoms. This has led to a noticeable uptick in inhaler usage across all severity levels. These fixed-dose inhalers enhance treatment efficacy by reducing inflammation through corticosteroids while simultaneously improving airflow using bronchodilators. The convenience of single-device administration plays a critical role in increasing adherence to prescribed treatments. With the growing burden of chronic respiratory diseases, healthcare providers are prioritizing combination therapies to deliver better clinical outcomes and minimize the risk of exacerbations. The market is also benefiting from ongoing innovations in inhaler designs that simplify usage for both patients and caregivers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.7 Billion |

| Forecast Value | $23.1 Billion |

| CAGR | 7.1% |

In terms of combination types, the market is categorized into corticosteroid and bronchodilator combination inhalers, long-acting beta-agonist (LABA) and inhaled corticosteroid (ICS) inhalers, triple combination inhalers, and other combinations. In 2024, corticosteroid and bronchodilator combination inhalers held the largest revenue share at 56.8%, driven by widespread clinical preference for these formulations in managing persistent respiratory symptoms. These inhalers are particularly effective in reducing airway inflammation and improving airflow, which are central to managing both asthma and COPD. The dual action not only improves symptom control but also reduces the need for rescue medications, making them a preferred choice among healthcare providers.

Based on indication, the market is segmented into asthma, chronic obstructive pulmonary disorder, and other conditions. The asthma segment accounted for the largest share at 57.4% in 2024 and is projected to reach a value of USD 13 billion by 2034. The increasing number of individuals diagnosed with asthma globally, especially among children, is significantly contributing to this segment's dominance. Asthma is a chronic and relapsing illness that often requires continuous therapy even during periods of symptom stability. This drives repeat purchases of fixed-dose inhalers and supports consistent revenue generation. Additionally, the updated clinical approach of prescribing combination inhalers for as-needed use has expanded the eligible patient base, further propelling growth in this segment.

The distribution of these inhalers is primarily through retail pharmacies, hospital pharmacies, and online pharmacies. Among these, retail pharmacies dominated the market and are anticipated to reach a value of USD 11.6 billion by 2034. Chronic respiratory diseases necessitate regular medication refills, and retail pharmacies offer the convenience and accessibility required to meet these ongoing needs. Their widespread presence in urban and suburban regions ensures patients have easy access to their prescriptions and pharmacist consultations, which improves adherence and supports steady market growth.

Regionally, North America continues to be a leading market, with the U.S. playing a major role. The fixed-dose combination inhalers market in the U.S. was valued at USD 4.5 billion in 2024 and is projected to grow to USD 8.7 billion by 2034. The high prevalence of asthma and COPD, along with strong compliance with clinical treatment protocols, is fueling demand. Physicians in the U.S. follow evidence-based treatment strategies that prioritize combination inhalers, leading to higher prescription rates. Furthermore, extensive pharmacy networks across the country enhance product availability and refill convenience, contributing to increased usage.

Globally, the market maintains an oligopolistic structure, with a few key players dominating the competitive landscape. Around 75% of the total market share is held by four major pharmaceutical companies with strong respiratory portfolios and device expertise. These firms continue to invest heavily in research and development to maintain their competitive edge. Meanwhile, generic and regional manufacturers are gaining traction in emerging economies by offering cost-effective alternatives, catering to the needs of price-sensitive populations. The market is also witnessing a growing inclination toward once-daily dosing options and triple therapy combinations, supported by innovations in inhaler devices that enhance usability and patient outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of asthma and chronic respiratory diseases

- 3.2.1.2 Favorable guidelines supporting the use of combination therapy

- 3.2.1.3 Advancements in inhaler technologies

- 3.2.1.4 Growing approval of combination inhaler therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of fixed dose combination inhalers

- 3.2.2.2 Concerns related to improper use and side effects

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Patent analysis

- 3.9 Regulatory landscape

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Combination, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Corticosteroid and bronchodilator combination inhalers

- 5.3 Long-acting beta agonist and inhaled corticosteroid combination inhalers

- 5.4 Triple combination

- 5.5 Other combinations

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Asthma

- 6.3 Chronic obstructive pulmonary disorder

- 6.4 Other indications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Retail pharmacies

- 7.3 Hospital pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AstraZeneca

- 9.2 Boehringer Ingelheim

- 9.3 Chiesi Farmaceutici

- 9.4 Cipla

- 9.5 GlaxoSmithKline

- 9.6 Glenmark Pharmaceuticals

- 9.7 Hikma Pharmaceuticals

- 9.8 Lupin

- 9.9 Mylan (Viatris)

- 9.10 Novartis

- 9.11 Orion

- 9.12 Sun Pharmaceutical Industries

- 9.13 Teva Pharmaceuticals

- 9.14 Vectura Group

- 9.15 Zydus Group

吸入药物市场:按器材、适应症、製造商、分销管道和最终用户分類的全球市场预测 – 2026-2032 年吸入疗法雾化器市场:按设备类型、应用、最终用户和分销管道划分-2026-2032年全球市场预测

吸入药物市场:按器材、适应症、製造商、分销管道和最终用户分類的全球市场预测 – 2026-2032 年吸入疗法雾化器市场:按设备类型、应用、最终用户和分销管道划分-2026-2032年全球市场预测 全球吸入药物市场规模、份额、趋势和成长分析报告(2026-2034)全球雾化器市场规模、份额、趋势和成长分析报告(2026-2034年)

全球吸入药物市场规模、份额、趋势和成长分析报告(2026-2034)全球雾化器市场规模、份额、趋势和成长分析报告(2026-2034年) 宠物类固醇市场规模、份额和成长分析:按产品类型、配方类型、动物种类、最终用户和地区划分-2026-2033年产业预测吸入型皮质类固醇市场依适应症、剂型、分子结构、最终用户和通路划分-2026-2032年全球预测

宠物类固醇市场规模、份额和成长分析:按产品类型、配方类型、动物种类、最终用户和地区划分-2026-2033年产业预测吸入型皮质类固醇市场依适应症、剂型、分子结构、最终用户和通路划分-2026-2032年全球预测 全球吸入性药物市场按药物类别、产品类型、应用、分销管道和地区划分

全球吸入性药物市场按药物类别、产品类型、应用、分销管道和地区划分 吸入药物市场、机会、成长动力、产业趋势分析与预测,2024-2032

吸入药物市场、机会、成长动力、产业趋势分析与预测,2024-2032