|

市场调查报告书

商品编码

1750323

慢性病管理市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Chronic Disease Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

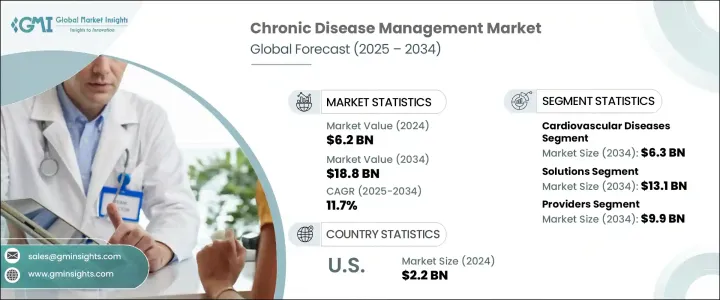

2024年,全球慢性病管理市场规模达62亿美元,预计2034年将以11.7%的复合年增长率成长,达到188亿美元。这主要得益于糖尿病、心血管疾病和高血压等慢性病的日益流行,这些疾病亟需有效的管理策略。此外,远距医疗服务、远距监控设备和电子健康记录等数位医疗技术的进步,也彻底改变了慢性病照护的格局。这些技术进步不仅增强了护理协调和临床决策能力,还支持采取主动干预措施,从而预防病情进展、最大限度地减少再入院率并提高治疗依从性,最终改变慢性病护理的提供方式,并提高全系统的效率。

此外,它们还能为医疗服务提供者提供即时资料洞察,简化患者与护理团队之间的沟通,并促进及时调整药物,所有这些都有助于提供更敏捷、以患者为中心的护理和长期健康管理。这些工具还透过促进自我监测、教育和问责来提高患者参与度,这对于有效管理复杂且长期的疾病至关重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 62亿美元 |

| 预测值 | 188亿美元 |

| 复合年增长率 | 11.7% |

2024年,心血管疾病市场规模达22亿美元,预计2034年将达63亿美元。冠状动脉疾病、心臟衰竭和高血压等疾病发生率的上升,增加了对综合管理解决方案的需求。远距医疗平台、穿戴式装置和远端监控系统有助于追踪血压和心率等生命体征,促进及时干预,并提高患者对治疗方案的依从性。

2024年,医疗服务提供者占据市场主导地位,占53.8%的份额,预计2025年至2034年的复合年增长率将达到11.5%。医疗保健服务提供者,包括医院、诊所和专科护理中心,是慢性病管理服务的核心。整合数位医疗技术使服务提供者能够提供持续护理、监测患者病情进展并根据需要调整治疗方案,从而改善患者的治疗效果和满意度。

美国慢性病管理市场规模在2024年达到22亿美元,预计2025年至2034年期间的复合年增长率将达到11.1%。美国先进的医疗基础设施、数位医疗技术的广泛应用以及支持性的报销政策促进了这一增长。美国人口中慢性病盛行率的不断上升进一步推动了对有效管理解决方案的需求。

全球慢性病管理市场的主要参与者包括 ResMed、Veradigm、IBM Corporation、Amwell、Oracle Corporation、Teladoc Health、Cerner Corporation、HealthSnap、Medtronic 和 Koninklijke Philips NV。这些公司专注于开发创新解决方案,以增强慢性病管理。他们正在采取诸如扩展远距医疗服务、整合人工智慧进行预测分析以及与医疗保健提供者建立合作伙伴关係等策略,以增强其市场影响力。此外,研发投入旨在提高病患参与度和治疗效果,从而使这些公司在不断发展的医疗保健领域中保持持续成长。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 慢性病盛行率上升

- 远距医疗和远端监控的不断进步

- 不断扩大的数位医疗领域

- 政府为创新解决方案提供的措施和资金

- 产业陷阱与挑战

- 实施成本高

- 资料隐私和安全问题

- 成长动力

- 成长潜力分析

- 监管格局

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:依疾病类型,2021 年至 2034 年

- 主要趋势

- 心血管疾病(CVD)

- 糖尿病

- 慢性呼吸道肺部疾病(COPD)

- 癌症

- 神经系统疾病

- 其他疾病类型

第六章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 解决方案

- 基于 Web 的解决方案

- 基于云端的解决方案

- 本地解决方案

- 服务

- 疾病管理计划和服务

- 监控服务

- 咨询和支援服务

- 其他服务类型

第七章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 提供者

- 付款人

- 其他最终用途

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Active Health Technologies

- Amwell

- Apollo TeleHealth

- Epic Systems

- HealthSnap

- IBM

- Koninklijke Philips NV

- Medicross

- Medtronic

- Oracle

- ResMed

- ScienceSoft USA

- Teladoc

- TimeDoc Health

- Topcon Healthcare

- Veradigm

- ZEISS

The Global Chronic Disease Management Market was valued at USD 6.2 billion in 2024 and is estimated to grow at a CAGR of 11.7% to reach USD 18.8 billion by 2034, driven by the increasing prevalence of chronic conditions such as diabetes, cardiovascular diseases, and hypertension, which necessitate effective management strategies. Additionally, advancements in digital health technologies, including telehealth services, remote monitoring devices, and electronic health records, have transformed the landscape of chronic care. These technological advancements not only enhance care coordination and clinical decision-making but also support proactive interventions that prevent disease progression, minimize hospital readmissions, and increase treatment adherence, ultimately transforming chronic care delivery and boosting system-wide efficiency.

Additionally, they empower healthcare providers with real-time data insights, streamline communication between patients and care teams, and facilitate timely medication adjustments, all of which contribute to more responsive, patient-centered care and long-term health management. These tools also foster greater patient engagement by promoting self-monitoring, education, and accountability, which are essential for managing complex, long-duration conditions effectively.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.2 Billion |

| Forecast Value | $18.8 Billion |

| CAGR | 11.7% |

The cardiovascular diseases segment was valued at USD 2.2 billion in 2024 and is anticipated to reach USD 6.3 billion by 2034. The rising incidence of conditions like coronary artery disease, heart failure, and hypertension has increased the demand for comprehensive management solutions. Telehealth platforms, wearable devices, and remote monitoring systems help in tracking vital signs such as blood pressure and heart rate, facilitating timely interventions, and enhancing patient compliance with treatment regimens.

In 2024, the providers segment dominated the market, accounting for 53.8% of the share, and is expected to grow at a CAGR of 11.5% from 2025 to 2034. Healthcare providers, including hospitals, clinics, and specialized care centers, are central to chronic disease management services. Integrating digital health technologies allows providers to offer continuous care, monitor patient progress, and adjust treatment plans as needed, leading to improved patient outcomes and satisfaction.

U.S. Chronic Disease Management Market accounted for USD 2.2 billion in 2024 and is projected to grow at a CAGR of 11.1% between 2025 and 2034. The country's advanced healthcare infrastructure, widespread adoption of digital health technologies, and supportive reimbursement policies contribute to this growth. The increasing prevalence of chronic conditions among the U.S. population further drives the demand for effective management solutions.

Key players in the Global Chronic Disease Management Market include ResMed, Veradigm, IBM Corporation, Amwell, Oracle Corporation, Teladoc Health, Cerner Corporation, HealthSnap, Medtronic, and Koninklijke Philips N.V. These companies are focusing on developing innovative solutions to enhance chronic disease management. Strategies such as expanding telehealth services, integrating artificial intelligence for predictive analytics, and forming partnerships with healthcare providers are being employed to strengthen their market presence. Additionally, investments in research and development aim to improve patient engagement and treatment outcomes, positioning these companies for sustained growth in the evolving healthcare landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic disease

- 3.2.1.2 Growing advancements in telehealth and remote monitoring

- 3.2.1.3 Expanding digital health sector

- 3.2.1.4 Government initiatives and funding for innovative solution

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation costs

- 3.2.2.2 Data privacy and security concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiovascular diseases (CVD)

- 5.3 Diabetes

- 5.4 Chronic respiratory pulmonary diseases (COPD)

- 5.5 Cancer

- 5.6 Neurological disorders

- 5.7 Other disease types

Chapter 6 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Solutions

- 6.2.1 Web-based solutions

- 6.2.2 Cloud-based solutions

- 6.2.3 On-premises solutions

- 6.3 Services

- 6.3.1 Disease management program and services

- 6.3.2 Monitoring services

- 6.3.3 Counseling and support services

- 6.3.4 Other service types

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Providers

- 7.3 Payers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Active Health Technologies

- 9.2 Amwell

- 9.3 Apollo TeleHealth

- 9.4 Epic Systems

- 9.5 HealthSnap

- 9.6 IBM

- 9.7 Koninklijke Philips N.V.

- 9.8 Medicross

- 9.9 Medtronic

- 9.10 Oracle

- 9.11 ResMed

- 9.12 ScienceSoft USA

- 9.13 Teladoc

- 9.14 TimeDoc Health

- 9.15 Topcon Healthcare

- 9.16 Veradigm

- 9.17 ZEISS