|

市场调查报告书

商品编码

1750353

聚酮(PK)市场机会、成长动力、产业趋势分析及2025-2034年预测Polyketone (PK) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

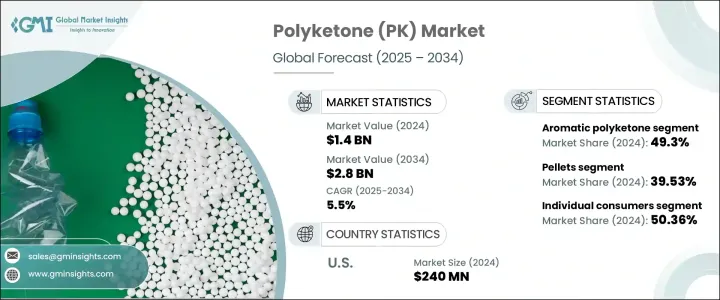

2024年,全球聚酮市场规模达14亿美元,预计到2034年将以5.5%的复合年增长率成长,达到28亿美元,这得益于各行各业对高性能聚合物的需求不断增长。这一成长主要源自于人们对先进材料替代品的探索,这些材料具有优异的耐化学性、低吸湿性和更佳的耐磨性。这些特性使聚酮成为聚酰胺和聚甲醛等传统材料的有力替代品。其应用领域不断扩展,尤其是在需要满足严格性能和监管标准的材料领域。日益增强的环保意识以及对轻量化、节能解决方案的追求推动了其应用。

聚酮的市场表现强劲,尤其是对耐用性和耐化学性要求较高的领域。像聚酮这样的轻质聚合物越来越多地应用于高压力环境,例如燃油系统和汽车结构部件。它们帮助製造商满足严格的排放标准,同时提升产品性能并减轻车辆总重。聚酮在极端条件下仍能保持机械强度,使其成为传统工程塑胶的宝贵替代品,尤其是在经常接触燃料、润滑剂和高温的环境中。该材料具有多种形态,例如颗粒、纤维、片材和薄膜,这进一步扩大了其在电子、消费品和运输等行业的吸引力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 14亿美元 |

| 预测值 | 28亿美元 |

| 复合年增长率 | 5.5% |

2024年,颗粒材料市场占据了39.53%的市场份额,这得益于其易于加工且与挤出和注塑等标准製造流程相容。颗粒材料均匀、吸湿性低且尺寸稳定性优异,能够精确製造复杂零件。此外,其对腐蚀性化学物质和碳氢化合物的强烈耐受性使其成为暴露于恶劣环境的部件的首选。这些优势使颗粒材料成为汽车等高要求行业的首选材料,因为这些行业对性能、安全性和合规性的要求至关重要。

同时,消费者对环保替代品的认知推动了个人消费领域的需求,到2024年,这一比例将达到50.36%。人们倾向于在日常用品中使用永续材料,这一趋势与聚酮的可回收和环保特性相得益彰。消费者观念的转变不仅推动了绿色产品的销售,也鼓励企业使用高性能永续聚合物来改进现有产品。这种转变为聚酮在体育用品、可穿戴技术、厨具和个人配件等产品的生产中开闢了新的机会——在这些领域,用户如今期待环保设计,同时又不牺牲耐用性或功能性。

2024年,美国聚酮 (PK) 市场规模达2.4亿美元,并将继续快速成长,这得益于其强大的产业框架、以创新为核心的发展模式以及对先进材料的旺盛需求。由于电子、航太和汽车行业的蓬勃发展,北美仍然是PK应用的主要中心。当地对永续技术和先进聚合物科学的重视,对巩固聚酮在该地区的地位发挥重要作用。

聚酮 (PK) 产业的参与者包括 Nexeo Plastics、Ensinger、晓星、三井塑胶和 Avient。为了巩固市场地位,各公司正大力投资研发,专注于产品创新和拓展应用领域。与汽车和电子行业製造商建立策略合作伙伴关係有助于提升商业应用。企业也在提升供应链效率,并引入永续的生产流程。透过开发客製化等级和多元化产品组合,他们正在满足不断变化的终端用户需求,并增强长期竞争力。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 贸易统计(HS编码)

- 主要出口国

- 主要进口国

註:以上贸易统计仅针对重点国家。

- 监管格局

- 衝击力

- 成长动力

- 汽车产业需求不断成长

- 电动车(EV)与永续旅行的兴起

- 对高性能材料的需求不断增加

- 产业陷阱与挑战

- 生产成本高

- 监管和环境问题

- 成长动力

- 政策参与

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按类型,2021-2034

- 主要趋势

- 芳香聚酮

- 脂肪族聚酮

- 共聚物聚酮

第六章:市场估计与预测:依形式,2021-2034

- 主要趋势

- 颗粒

- 纤维

- 电影

- 工作表

第七章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 汽车零件

- 电气和电子产品

- 产业机械

- 消费品

- 涂料和黏合剂

- 医疗器材

- 包装

- 其他的

第八章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- AKRO-PLASTIC

- Avient

- Distrupol

- Ensinger

- HYOSUNG

- KD Feddersen

- LEHVOSS

- MITSUI PLASTICS

- Nexeo Plastics

- POLYOLS & POLYMERS

- Rochling

- Specialist Engineering Plastics

- Technoform

The Global Polyketone Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 2.8 billion by 2034 due to increasing demand for high-performance polymers across several industries. This growth is largely fueled by the search for advanced material alternatives that offer superior chemical resistance, low moisture absorption, and improved wear properties. These characteristics position polyketones as a competitive substitute for traditional materials like polyamides and polyoxymethylene. Their applications continue to expand, especially in sectors requiring materials that meet stringent performance and regulatory standards. Rising environmental consciousness and the push for lightweight, fuel-efficient solutions drive adoption.

Polyketone's market performance has been strong, particularly in segments that demand durability and chemical resistance. Lightweight polymers like PK are increasingly used in high-stress environments, such as fuel systems and structural automotive components. They help manufacturers meet strict emissions standards while improving product performance and reducing overall vehicle weight. Polyketone's ability to maintain mechanical strength under extreme conditions makes it a valuable alternative to conventional engineering plastics, especially where exposure to fuels, lubricants, and high temperatures is common. The material's adaptability in various forms-like pellets, fibers, sheets, and films-has further widened its appeal across industries, including electronics, consumer goods, and transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 5.5% |

The pellets segment accounted for 39.53% share in 2024 due to their ease of processing and compatibility with standard manufacturing techniques such as extrusion and injection molding. Their uniformity, low moisture absorption, and excellent dimensional stability allow precision in manufacturing complex parts. Additionally, their strong resistance to harsh chemicals and hydrocarbons makes them a preferred choice for components exposed to aggressive environments. These advantages make pellets the go-to form in demanding sectors like automotive, where performance, safety, and compliance with regulations are non-negotiable.

Meanwhile, consumer awareness of eco-friendly alternatives has pushed demand within the individual consumer segment, representing a 50.36% share in 2024. People lean toward sustainable materials in everyday products, a trend that aligns well with polyketone's recyclable and environmentally conscious profile. The shift in consumer mindset is not only driving sales of green products but also encouraging companies to reformulate existing goods using high-performance sustainable polymers. This shift has opened new opportunities for polyketone in the production of items such as sporting goods, wearable tech, kitchenware, and personal accessories-areas where users are now expecting eco-conscious design without compromising on durability or function.

United States Polyketone (PK) Market was valued at USD 240 million in 2024 and continues to grow rapidly, backed by a robust industrial framework, innovation-focused development, and a high demand for advanced materials. North America remains a major hub for PK applications due to strong activity in the electronics, aerospace, and automotive sectors. Local emphasis on sustainable technologies and advanced polymer science plays a significant role in reinforcing polyketone's presence in the region.

The Polyketone (PK) industry players include Nexeo Plastics, Ensinger, HYOSUNG, MITSUI PLASTICS, and Avient. To secure a stronger position in the market, companies are heavily investing in research and development, focusing on product innovations and expanding application areas. Strategic partnerships with manufacturers across the automotive and electronics sectors help boost commercial adoption. Businesses are also improving supply chain efficiency and introducing sustainable manufacturing processes. By developing custom grades and diversifying product portfolios, they're addressing evolving end-user needs and reinforcing long-term competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.3 Supply-side impact (raw materials)

- 3.2.3.1 Price volatility in key materials

- 3.2.3.2 Supply chain restructuring

- 3.2.3.3 Production cost implications

- 3.2.4 Demand-side impact (selling price)

- 3.2.4.1 Price transmission to end markets

- 3.2.4.2 Market share dynamics

- 3.2.4.3 Consumer response patterns

- 3.2.5 Key companies impacted

- 3.2.6 Strategic industry responses

- 3.2.6.1 Supply chain reconfiguration

- 3.2.6.2 Pricing and product strategies

- 3.2.6.3 Policy engagement

- 3.2.7 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Growing demand in the automotive industry

- 3.5.1.2 Rise of electric vehicles (EVs) and sustainable mobility

- 3.5.1.3 Increasing demand for high-performance materials

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 High production costs

- 3.5.2.2 Regulatory & environmental concerns

- 3.5.1 Growth drivers

- 3.6 Policy engagement

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Aromatic polyketone

- 5.3 Aliphatic polyketone

- 5.4 Copolymer polyketone

Chapter 6 Market Estimates and Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Pellets

- 6.3 Fibers

- 6.4 Films

- 6.5 Sheets

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive components

- 7.3 Electrical & electronics

- 7.4 Industrial machinery

- 7.5 Consumer goods

- 7.6 Coatings & adhesives

- 7.7 Medical devices

- 7.8 Packaging

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 AKRO-PLASTIC

- 9.2 Avient

- 9.3 Distrupol

- 9.4 Ensinger

- 9.5 HYOSUNG

- 9.6 K.D. Feddersen

- 9.7 LEHVOSS

- 9.8 MITSUI PLASTICS

- 9.9 Nexeo Plastics

- 9.10 POLYOLS & POLYMERS

- 9.11 Rochling

- 9.12 Specialist Engineering Plastics

- 9.13 Technoform

酮类全球市场规模、份额、趋势和成长分析报告(2026-2034)

酮类全球市场规模、份额、趋势和成长分析报告(2026-2034) 酮类市场:按类型、形态、应用、最终用户和分销管道划分-2026-2032年全球市场预测芳香酮聚合物市场:依产品类型、形态、製造流程、应用和最终用途产业划分-2026-2032年全球预测

酮类市场:按类型、形态、应用、最终用户和分销管道划分-2026-2032年全球市场预测芳香酮聚合物市场:依产品类型、形态、製造流程、应用和最终用途产业划分-2026-2032年全球预测 2026年全球酮类市场报告脂肪族聚酮市场按等级、形态、应用和最终用途产业划分-2026-2032年全球预测

2026年全球酮类市场报告脂肪族聚酮市场按等级、形态、应用和最终用途产业划分-2026-2032年全球预测 2018-2034年全球芳香酮聚合物市场需求及预测分析

2018-2034年全球芳香酮聚合物市场需求及预测分析 全球环酮市场

全球环酮市场 全球脂肪族聚酮市场:市场占有率和排名、总收入和需求预测(2025-2031)

全球脂肪族聚酮市场:市场占有率和排名、总收入和需求预测(2025-2031) 美国酮市场:市场规模、份额、趋势分析(按应用)、细分市场预测(2025-2030 年)全球酮市场:市场规模、占有率、趋势、产业分析(依产品、应用和地区)、未来预测(2025-2034)

美国酮市场:市场规模、份额、趋势分析(按应用)、细分市场预测(2025-2030 年)全球酮市场:市场规模、占有率、趋势、产业分析(依产品、应用和地区)、未来预测(2025-2034)