|

市场调查报告书

商品编码

1750430

牙科显微外科市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Dental Microsurgery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

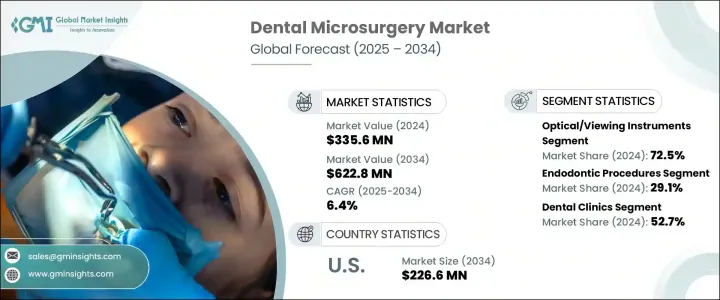

2024年,全球牙科显微外科市场规模达3.356亿美元,预估年复合成长率为6.4%,到2034年将达到6.228亿美元。该市场将采用先进的外科技术进行精准手术,同时最大程度地减少组织损伤并缩短癒合时间。此领域高度依赖手术显微镜、微型器械和精细缝线等专用工具,以实现精细的放大手术。全球老龄化人口的不断增长对该市场的扩张发挥着重要作用,因为牙龈萎缩、牙齿脱落和慢性牙周炎等与年龄相关的牙科疾病需要高度精准的外科手术干预。此外,龋齿和牙周炎等口腔健康问题的增加也加剧了对牙科显微外科的需求。

口腔卫生不良、不健康的饮食习惯以及糖尿病和高血压等慢性疾病的盛行率上升等因素,都显着加剧了口腔健康问题的恶化。这些因素不仅加速了蛀牙、牙周炎和牙龈疾病等疾病的发展,也使这些问题变得更加棘手。随着这些口腔健康问题在全球范围内持续上升,对精准、高效、恢復时间更快的先进外科手术解决方案的需求也日益增长。牙科显微外科手术已成为许多专业人士的首选,因为它能够进行高度可控的微创手术,并具有更好的视觉清晰度,这在复杂病例中尤其重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3.356亿美元 |

| 预测值 | 6.228亿美元 |

| 复合年增长率 | 6.4% |

2024年,光学和观察仪器市场占72.5%的份额。牙科手术显微镜、放大镜和内视镜对于提高手术精确度和临床疗效至关重要。这些设备可以增强放大倍率和照明效果,使医生能够观察复杂的细节,从而改善诊断并减少错误。高清影像和人体工学设计等创新技术正在加速这些工具的普及,尤其是在根管治疗领域。

市场的另一个关键驱动力是牙髓治疗领域,该领域在2024年占据了最大的市场份额,达到29.1%。牙髓坏死和根尖周围疾病的增加使得根管治疗等精准干预措施成为必要,从而推动了该领域对显微外科手术的需求。先进的显微外科可视化辅助设备的使用提高了这些治疗的成功率,从而引发了市场日益增长的兴趣。

美国牙科显微外科市场在2024年创收1.236亿美元,预计2034年将达到2.266亿美元。根尖手术和牙周再生等先进手术的需求不断增长是推动其成长的主要动力。这些服务在美国,尤其是在老龄化人口中的高普及率,进一步加速了市场的成长。随着越来越多的牙科专业人士采用显微外科技术,预计美国市场将继续在全球市场中占据主导地位。

该行业的主要参与者包括 B. Braun Melsungen、Dentsply Sirona、MediThinQ、Microsurgery Instruments、Kerr、Global Surgical、Henry Schein、Peter LAZIC、Zeiss International、Microsurgical Technology、Zut Biomet、Institut Straumann、Hu-Friedy 和 Danaher。牙科显微外科市场的公司为巩固其地位而采用的关键策略包括不断创新先进的手术器械、更加註重用户友好型设计以及扩展其产品种类以满足各种牙科手术的需求。此外,与牙科诊所和教育机构的合作有助于提高牙科员工的意识和培训,从而提高市场渗透率。对研发技术和设备的投资进一步增强了他们的竞争优势,并确保他们在快速发展的市场中始终处于领先地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球牙科疾病盛行率不断上升

- 全球老龄人口不断增加

- 微创牙科手术的需求不断增长

- 牙科手术显微镜和视觉化技术的进步

- 产业陷阱与挑战

- 有限的报销政策

- 显微外科设备及手术费用高昂

- 成长动力

- 成长潜力分析

- 监管格局

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 各国应对措施

- 对产业的影响

- 供应方影响(製造成本)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(消费者成本)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(製造成本)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 光学/观测仪器

- 显微外科器械

- 其他产品

第六章:市场估计与预测:按程序,2021 - 2034 年

- 主要趋势

- 牙种植体

- 诊断程序

- 根尖切除术

- 牙周手术

- 根管治疗

- 其他程式

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 牙医诊所

- 医院

- 其他最终用途

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- B. Braun Melsungen

- Danaher

- Dentsply Sirona

- Global Surgical

- Henry Schein

- Hu-Friedy

- Institut Straumann

- Kerr

- MediThinQ

- Microsurgery Instruments

- Microsurgical Technology

- Peter LAZIC

- Zeiss International

- Zimmer Biomet

The Global Dental Microsurgery Market was valued at USD 335.6 million in 2024 and is estimated to grow at a 6.4% CAGR, to reach USD 622.8 million by 2034, driven using advanced surgical techniques to perform precise procedures while minimizing tissue damage and enhancing healing times. This field relies heavily on specialized tools such as surgical microscopes, micro-instruments, and fine sutures, allowing detailed, magnified operations. The increasing global aging population plays a significant role in this market's expansion, as age-related dental conditions like gum recession, tooth loss, and chronic periodontitis require highly accurate surgical interventions. Additionally, the rise in oral health issues, including tooth decay and periodontitis, contributes to the demand for dental microsurgery.

Factors such as inadequate oral hygiene, unhealthy dietary habits, and the rising prevalence of chronic conditions like diabetes and hypertension are significantly contributing to the worsening of oral health issues. These factors not only accelerate the development of conditions like tooth decay, periodontitis, and gum disease but also make these issues more challenging. As these oral health problems continue to rise globally, the demand for advanced surgical solutions that offer precision, efficiency, and quicker recovery times is growing. Dental microsurgery has become a preferred choice for many professionals because it allows for highly controlled, minimally invasive procedures with better visual clarity, which is especially important in complex cases.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $335.6 Million |

| Forecast Value | $622.8 Million |

| CAGR | 6.4% |

The optical and viewing instruments segment held a 72.5% share in 2024. Dental operating microscopes, loupes, and endoscopes are critical for improving surgical precision and clinical outcomes. These devices enhance magnification and lighting, enabling practitioners to view intricate details, improving diagnosis and reducing errors. Innovations like high-definition imaging and ergonomic designs are accelerating the adoption of these tools, especially for root canal procedures.

Another key driver in the market is the endodontic procedures segment, which accounted for the largest share of USD 29.1% in 2024. The rise in pulp necrosis and periapical diseases necessitates precise interventions like root canal therapy, driving the demand for microsurgery in this area. The use of advanced microsurgical visualization aids has enhanced the success rates of these treatments, leading to growing market interest.

United States Dental Microsurgery Market generated USD 123.6 million in 2024 and is expected to reach USD 226.6 million by 2034. The growing demand for advanced procedures such as root-end surgeries and periodontal regeneration is a major driver of this expansion. The high adoption rates of these services in the U.S., particularly among the aging population, are further accelerating market growth. As more dental professionals embrace microsurgical techniques, the U.S. market is expected to remain a dominant player in the global landscape.

Major players in the industry include B. Braun Melsungen, Dentsply Sirona, MediThinQ, Microsurgery Instruments, Kerr, Global Surgical, Henry Schein, Peter LAZIC, Zeiss International, Microsurgical Technology, Zimmer Biomet, Institut Straumann, Hu-Friedy, and Danaher. Key strategies employed by companies in the Dental Microsurgery Market to strengthen their position include continuous innovation in advanced surgical instruments, increasing their focus on user-friendly designs, and expanding their product offerings to cater to diverse dental procedures. Additionally, partnerships with dental practices and educational institutions help enhance awareness and training of the dental workforce, boosting market penetration. Investment in R&D to develop technologies and devices further strengthens their competitive edge and ensures they remain at the forefront of the rapidly evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of dental disorders globally

- 3.2.1.2 Increasing elderly population worldwide

- 3.2.1.3 Rising demand for minimally invasive dental procedures

- 3.2.1.4 Advancements in dental operating microscopes and visualization technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited reimbursement policies

- 3.2.2.2 High cost of microsurgical equipment and procedures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Optical/viewing instruments

- 5.3 Microsurgical instrumentation

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By Procedure, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dental implants

- 6.3 Diagnostic procedures

- 6.4 Apicoectomy

- 6.5 Periodontal surgery

- 6.6 Endodontic procedures

- 6.7 Other procedures

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Dental clinics

- 7.3 Hospitals

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B. Braun Melsungen

- 9.2 Danaher

- 9.3 Dentsply Sirona

- 9.4 Global Surgical

- 9.5 Henry Schein

- 9.6 Hu-Friedy

- 9.7 Institut Straumann

- 9.8 Kerr

- 9.9 MediThinQ

- 9.10 Microsurgery Instruments

- 9.11 Microsurgical Technology

- 9.12 Peter LAZIC

- 9.13 Zeiss International

- 9.14 Zimmer Biomet

显微外科器械市场:按材料、应用、最终用户和销售管道划分-2026-2032年全球市场预测

显微外科器械市场:按材料、应用、最终用户和销售管道划分-2026-2032年全球市场预测 2026年全球膜铲市场报告

2026年全球膜铲市场报告 全球显微外科市场规模、份额、趋势和成长分析报告(2026-2034)全球显微外科市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球显微外科市场规模、份额、趋势和成长分析报告(2026-2034)全球显微外科市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 显微外科器械市场规模、份额及成长分析(依产品类型、显微外科手术类型、最终用户及地区划分)-2026-2033年产业预测

显微外科器械市场规模、份额及成长分析(依产品类型、显微外科手术类型、最终用户及地区划分)-2026-2033年产业预测 显微外科手术:全球市场份额和排名、总销售额和需求预测(2025-2031 年)

显微外科手术:全球市场份额和排名、总销售额和需求预测(2025-2031 年) 牙科显微外科市场-全球产业规模、份额、趋势、机会及预测(按产品、手术、地区和竞争细分,2020-2030 年)

牙科显微外科市场-全球产业规模、份额、趋势、机会及预测(按产品、手术、地区和竞争细分,2020-2030 年) 显微外科及超显微外科的全球市场:各终端用户,设备,手术,各地区 - 2032年前的预测分析

显微外科及超显微外科的全球市场:各终端用户,设备,手术,各地区 - 2032年前的预测分析 牙科果冻市场规模、份额、趋势分析报告:按产品、程序、地区、细分市场预测,2025-2030 年全球显微外科市场规模:按地区、范围和预测

牙科果冻市场规模、份额、趋势分析报告:按产品、程序、地区、细分市场预测,2025-2030 年全球显微外科市场规模:按地区、范围和预测