|

市场调查报告书

商品编码

1750455

结缔组织疾病治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Connective Tissue Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

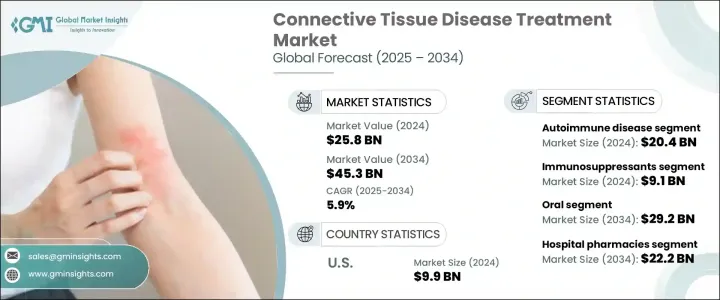

2024年,全球结缔组织疾病治疗市场规模达258亿美元,预计到2034年将以5.9%的复合年增长率增长,达到453亿美元,这主要得益于类风湿性关节炎、硬皮病和系统性红斑狼疮等自体免疫疾病的日益普及。全球老年人口尤其容易患上这些疾病,因为免疫系统会随着年龄增长而减弱,从而增加了结缔组织疾病的风险。此外,人们的认知度提高和诊断能力的提升使得人们能够更早发现和治疗结缔组织疾病,这进一步推动了市场的成长。

结缔组织疾病的治疗涉及多种药物的综合组合,旨在控制症状、减轻发炎并延缓病情进展。这些治疗方案包括用于快速缓解症状的皮质类固醇、用于调节人体免疫反应的免疫抑制剂、用于标靶干预的生物製剂、用于长期控制疾病的改善病情的抗风湿药物 (DMARD),以及用于改善患者舒适度的止痛疗法。由于这些疾病通常是慢性的,并且会影响多个器官和系统,因此通常会采用联合疗法来确保更有效、更持久的疗效。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 258亿美元 |

| 预测值 | 453亿美元 |

| 复合年增长率 | 5.9% |

结缔组织疾病治疗市场中的自体免疫疾病细分市场在2024年创收204亿美元。类风湿性关节炎等慢性疾病推动了这项需求,因为它们通常需要终身治疗和密切监测。全球自体免疫性结缔组织疾病的盛行率不断上升,以及寻求早期介入的患者群体不断扩大,持续支持着该细分市场的扩张。标靶疗法的不断发展以及新型生物製剂的问世,促进了更个人化和有效的治疗,从而减少了疾病发作和长期併发症。

在各类药物中,免疫抑制剂领域在2024年创造了91亿美元的市场规模,因为这类药物在抑制人体免疫系统攻击健康结缔组织(自体免疫疾病的标誌)方面发挥关键作用。对于病情进展迅速或多器官受影响的患者,免疫抑制剂的重要性尤其突出。免疫抑制剂有助于限制长期损害和住院治疗,凸显了其在治疗方案中的持续重要性。製剂和给药策略的改进也提高了免疫抑制剂的安全性,促进了其更广泛的应用。

2024年,北美结缔组织疾病治疗市场规模达99亿美元,这得益于先进的医疗体系、较高的诊断率以及专注于自体免疫疾病和发炎性疾病的强大研发管线。政府支持的计画和公私合作持续资助早期筛检、药物研发和病患支持计画的创新。这种投资水准不仅改善了临床疗效,也提高了整个北美大陆患者获得高效治疗方案的可近性。

全球结缔组织疾病治疗市场的主要参与者包括艾伯维、安进、勃林格殷格翰、礼来公司、葛兰素史克、Ingenus Pharmaceutical、杨森製药、默克、诺华、辉瑞、赛诺菲和梯瓦製药。这些公司积极参与开发和商业化旨在治疗影响结缔组织的自身免疫性和遗传性疾病的疗法。为了巩固市场地位,结缔组织疾病治疗领域的公司正在采取多项策略措施。这些措施包括投资研发以创新和推出新疗法,建立策略合作伙伴关係和合作关係以扩大产品组合和市场范围,以及专注于个人化医疗方法以满足患者的特定需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 结缔组织疾病盛行率上升

- 生物製剂和标靶治疗的进展

- 不断增加的研发投资

- 药物传输技术创新

- 产业陷阱与挑战

- 治疗费用高昂

- 副作用和长期安全问题

- 成长动力

- 成长潜力分析

- 监管格局

- 管道分析

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:依疾病类型,2021 年至 2034 年

- 主要趋势

- 自体免疫疾病

- 类风湿关节炎

- 硬皮症

- 混合结缔组织疾病

- 遗传性疾病

第六章:市场估计与预测:依药物类型,2021 年至 2034 年

- 主要趋势

- 免疫抑制剂

- 皮质类固醇

- 非类固醇抗发炎药

- 抗疟药物

- 其他药物类型

第七章:市场估计与预测:依管理路线,2021 年至 2034 年

- 主要趋势

- 口服

- 注射剂

第八章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 网路药局

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- AbbVie

- Amgen

- Azurity Pharmaceuticals

- Boehringer Ingelheim

- Eli Lilly and Company

- GlaxoSmithKline

- Ingenus Pharmaceutical

- Janssen Pharmaceutical

- Merck

- Novartis

- Pfizer

- Sanofi

- Teva Pharmaceutical

The Global Connective Tissue Disease Treatment Market was valued at USD 25.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 45.3 billion by 2034, driven by the increasing prevalence of autoimmune disorders such as rheumatoid arthritis, scleroderma, and systemic lupus erythematosus. The aging global population is particularly susceptible to these conditions, as the immune system weakens with age, heightening the risk of developing connective tissue diseases. Additionally, heightened awareness and improved diagnostic capabilities have led to earlier detection and treatment, further propelling market growth.

Treatment for connective tissue diseases involves a comprehensive mix of medications designed to control symptoms, reduce inflammation, and slow disease progression. These therapeutic options include corticosteroids for rapid symptom relief, immunosuppressants to regulate the body's immune response, biologics for targeted intervention, disease-modifying antirheumatic drugs (DMARDs) for long-term disease control, and pain-relief therapies to improve patient comfort. Since these disorders are often chronic and impact multiple organs and systems, combination therapies are frequently prescribed to ensure more effective and sustained results.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25.8 Billion |

| Forecast Value | $45.3 Billion |

| CAGR | 5.9% |

The autoimmune disease segment in the connective tissue disease treatment market generated USD 20.4 billion in 2024. Chronic conditions like rheumatoid arthritis drive this demand, as they often require lifelong treatment and close monitoring. The increasing global prevalence of autoimmune-related connective tissue disorders, along with a growing patient base seeking early intervention, continues to support the expansion of this segment. Continuous development in targeted therapies and the availability of new biologics have contributed to more personalized and effective treatments, reducing flare-ups and long-term complications.

Among the different drug classes, the immunosuppressants segment generated USD 9.1 billion in 2024 as these drugs play a critical role by inhibiting the body's immune system from attacking healthy connective tissue, a hallmark of autoimmune diseases. Their importance is particularly evident in patients with aggressive disease progression or multi-organ involvement. The use of immunosuppressants helps limit long-term damage and hospitalizations, underscoring their ongoing relevance in treatment protocols. Advancements in formulation and dosing strategies have also improved their safety profiles, encouraging wider adoption.

North America Connective Tissue Disease Treatment Market accounted for USD 9.9 billion in 2024, driven by the advanced healthcare systems, a high diagnosis rate, and strong R&D pipelines focused on autoimmune and inflammatory diseases. Government-backed programs and public-private collaborations continue to fund innovations in early screening, drug development, and patient support initiatives. This level of investment has not only improved clinical outcomes but has also increased the accessibility of high-efficacy treatment options to patients across the continent.

Key players in the Global Connective Tissue Disease Treatment Market include AbbVie, Amgen, Boehringer Ingelheim, Eli Lilly and Company, GlaxoSmithKline, Ingenus Pharmaceutical, Janssen Pharmaceutical, Merck, Novartis, Pfizer, Sanofi, and Teva Pharmaceutical. These companies are actively involved in developing and commercializing therapies aimed at managing autoimmune and genetic disorders affecting connective tissues. To strengthen their market position, companies in the connective tissue disease treatment sector are adopting several strategic initiatives. These include investing in research and development to innovate and introduce new therapies, forming strategic partnerships and collaborations to expand their product portfolios and market reach, and focusing on personalized medicine approaches to cater to the specific needs of patients.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of connective tissue diseases

- 3.2.1.2 Advancements in biologics and targeted therapies

- 3.2.1.3 Growing research and development investments

- 3.2.1.4 Technological innovations in drug delivery

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Side effects and long-term safety concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Trump administration tariffs

- 3.6.1 Impact on trade

- 3.6.1.1 Trade volume disruptions

- 3.6.1.2 Retaliatory measures

- 3.6.2 Impact on the Industry

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.2.1.1 Price volatility in key materials

- 3.6.2.1.2 Supply chain restructuring

- 3.6.2.1.3 Production cost implications

- 3.6.2.2 Demand-side impact (selling price)

- 3.6.2.2.1 Price transmission to end markets

- 3.6.2.2.2 Market share dynamics

- 3.6.2.2.3 Consumer response patterns

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.3 Key companies impacted

- 3.6.4 Strategic industry responses

- 3.6.4.1 Supply chain reconfiguration

- 3.6.4.2 Pricing and product strategies

- 3.6.4.3 Policy engagement

- 3.6.5 Outlook and future considerations

- 3.6.1 Impact on trade

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Autoimmune diseases

- 5.2.1 Rheumatoid arthritis

- 5.2.2 Scleroderma

- 5.2.3 Mixed connective tissue disease

- 5.3 Genetic disorders

Chapter 6 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Immnuosuppresants

- 6.3 Corticosteroids

- 6.4 NSAIDs

- 6.5 Antimalarial drugs

- 6.6 Other drug types

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectables

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Amgen

- 10.3 Azurity Pharmaceuticals

- 10.4 Boehringer Ingelheim

- 10.5 Eli Lilly and Company

- 10.6 GlaxoSmithKline

- 10.7 Ingenus Pharmaceutical

- 10.8 Janssen Pharmaceutical

- 10.9 Merck

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Teva Pharmaceutical