|

市场调查报告书

商品编码

1750465

癫痫监测设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Epilepsy Monitoring Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

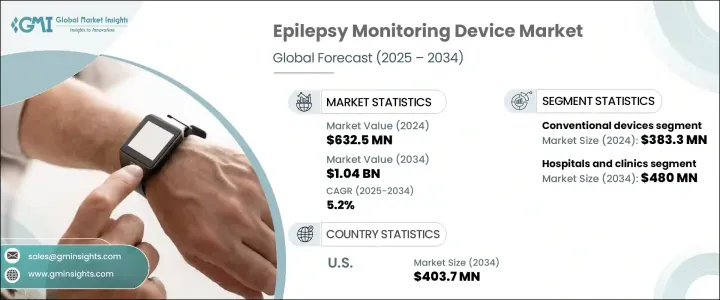

2024年,全球癫痫监测设备市场规模达6.325亿美元,预计到2034年将以5.2%的复合年增长率成长,达到10.4亿美元。全球癫痫负担日益加重,精准诊断工具的需求日益增长,是推动该市场发展的关键因素。医疗保健机构正在采用先进技术监测癫痫患者的大脑活动,从而更好地进行诊断和治疗。这些工具有助于检测大脑中不规则的电讯号,为了解癫痫发作模式提供宝贵的见解,并支持个人化治疗方案。此外,穿戴式装置、即时资料追踪和人工智慧系统等新一代技术的整合,增强了诊断能力,并拓展了其在家庭护理、门诊和医院环境中的应用。

持续的创新正在塑造癫痫监测的格局。如今,设备的准确性、便携性和便利性均有所提升,使其更易于获取,也更方便患者使用。随着对非侵入式即时监测的需求不断增长,这些进步正推动其在各种临床环境中得到更广泛的应用。人们对早期诊断的认识不断提高,以及对长期癫痫发作管理的需求也加速了市场的扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 6.325亿美元 |

| 预测值 | 10.4亿美元 |

| 复合年增长率 | 5.2% |

2024年,传统癫痫监测设备市场规模达3.833亿美元。其强大的临床表现、增强的诊断功能以及对多样化医疗需求的适应性,继续巩固了其市场主导地位。这些设备已发展到具备基于人工智慧的癫痫发作检测、云端连接和持续脑电波追踪等功能,使其成为药物研究和临床诊断中不可或缺的一部分。脑电图系统凭藉其非侵入性和即时脑活动映射功能,仍然是癫痫监测的核心,并推动了该市场的持续成长。

预计到2034年,医院和诊所细分市场将创造4.8亿美元的收入,这得益于其在管理癫痫等复杂神经系统疾病方面发挥的关键作用。这些医疗机构为患者提供一体化的照护环境,使其成为先进癫痫监测技术的理想之选。这些机构配备了神经影像系统、集中式资料管理平台和高风险护理单元等专业工具,能够对癫痫进行全天候监测和精准诊断。

预计到2034年,美国癫痫监测设备市场规模将达到4.037亿美元,这得益于不断增长的癫痫病例以及全球最先进的医疗保健体系。随着人们对神经系统健康的认识不断提高,加上优惠的报销政策和远距医疗的普及,诊断技术的可近性正在不断扩大。美国各地的主要参与者和研究机构正在积极投资下一代解决方案,包括基于人工智慧的分析、便携式脑电图系统和即时云端连接平台。

该领域的领先公司包括 Cadwell Industries、NeuroWave Systems、美敦力、日本光电株式会社、Seer Medical、Zeto、Medpage、Natus Medical Incorporated、波士顿科学公司、The Magstim、Masimo Corporation、Compumedics、荷兰皇家飞利浦、Stratus 和 Empatica。为了巩固市场地位,主要公司专注于策略性倡议,例如透过人工智慧整合和穿戴式解决方案扩展产品组合、与医疗保健提供者建立合作伙伴关係以及投资下一代监测技术的研发。他们还在扩大製造能力并改善设备连接性,以支援远端患者管理。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 癫痫盛行率不断上升

- 穿戴式装置的使用日益增多

- 癫痫监测技术的技术进步

- 人们对神经退化性疾病的认识不断提高

- 产业陷阱与挑战

- 复杂的癫痫监测程序和设备成本高昂

- 不利的报销政策

- 成长动力

- 成长潜力分析

- 监管格局

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 各国应对措施

- 对产业的影响

- 供应方影响(製造成本)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(消费者成本)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(製造成本)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 穿戴式装置

- 传统设备

- 深部脑部刺激装置

- 监控设备

- 脑电图设备

- 标准脑电图

- 视讯脑电图

- 其他脑电图设备

- 肌电图设备

- MEG 设备

- 其他监控设备

- 脑电图设备

第六章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院和诊所

- 门诊手术中心

- 神经病学中心

- 诊断中心

- 居家照护环境

第七章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第八章:公司简介

- Boston Scientific Corporation

- Cadwell Industries

- Compumedics

- Empatica

- Koninklijke Philips

- Masimo Corporation

- Medpage

- Medtronic

- Natus Medical Incorporated

- NeuroWave Systems

- NIHON KOHDEN CORPORATION

- Seer Medical

- Stratus

- The Magstim

- Zeto

The Global Epilepsy Monitoring Device Market was valued at USD 632.5 million in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 1.04 billion by 2034, driven by the growing global burden of epilepsy and the increasing demand for accurate diagnostic tools are key drivers of this market. Healthcare providers are adopting advanced technologies to monitor brain activity in patients experiencing seizures, enabling better diagnosis and treatment strategies. These tools help detect irregular electrical signals in the brain, offering valuable insights into seizure patterns and supporting personalized treatment plans. Additionally, the integration of next-generation technologies such as wearable devices, real-time data tracking, and AI-powered systems enhances diagnostic capabilities while expanding their use across homecare, ambulatory, and hospital settings.

Continuous innovation is shaping the landscape of epilepsy monitoring. Devices today offer improved accuracy, portability, and convenience, making them more accessible and patient-friendly. As the demand for non-invasive and real-time monitoring rises, these advancements encourage wider adoption in various clinical environments. The growing awareness about early diagnosis and the need for long-term seizure management accelerate market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $632.5 Million |

| Forecast Value | $1.04 Billion |

| CAGR | 5.2% |

The conventional epilepsy monitoring devices segment generated USD 383.3 million in 2024. Their strong clinical performance, enhanced diagnostic features, and adaptability to diverse medical needs continue to drive their dominance. These devices have evolved to include capabilities like AI-based seizure detection, cloud connectivity, and continuous brainwave tracking, making them indispensable in pharmaceutical research and clinical diagnosis. EEG systems remain the core of epilepsy monitoring due to their non-invasive nature and real-time brain activity mapping, contributing to the sustained growth of this segment.

The hospitals and clinics segment is projected to generate USD 480 million by 2034, driven by their critical role in managing complex neurological conditions like epilepsy. These healthcare settings offer an integrated environment for patient care, making them ideal for advanced epilepsy monitoring technologies. Equipped with specialized tools such as neuroimaging systems, centralized data management platforms, and high-acuity care units, these facilities enable round-the-clock monitoring and precise diagnosis of seizure disorders.

United States Epilepsy Monitoring Device Market is anticipated to reach USD 403.7 million by 2034, supported by a rising number of epilepsy cases and one of the world's most advanced healthcare systems. The increasing awareness of neurological health, paired with favorable reimbursement policies and the adoption of telemedicine, is expanding access to diagnostic technologies. Major players and research institutions across the country are actively investing in next-generation solutions, including AI-based analytics, portable EEG systems, and real-time cloud-connected platforms.

Leading companies in this space include Cadwell Industries, NeuroWave Systems, Medtronic, NIHON KOHDEN CORPORATION, Seer Medical, Zeto, Medpage, Natus Medical Incorporated, Boston Scientific Corporation, The Magstim, Masimo Corporation, Compumedics, Koninklijke Philips, Stratus, and Empatica. To strengthen their market position, key companies focus on strategic initiatives such as expanding product portfolios through AI integration and wearable solutions, forming partnerships with healthcare providers, and investing in R&D for next-gen monitoring technologies. They are also scaling manufacturing capabilities and improving device connectivity to support remote patient management.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of epilepsy

- 3.2.1.2 Rising use of wearable devices

- 3.2.1.3 Technological advancements in epilepsy monitoring technologies

- 3.2.1.4 Growing awareness of neurodegenerative disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of complex epilepsy monitoring procedures and devices

- 3.2.2.2 Unfavorable reimbursement policies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Wearable devices

- 5.3 Conventional devices

- 5.3.1 Deep brain stimulation devices

- 5.3.2 Monitoring devices

- 5.3.2.1 EEG devices

- 5.3.2.1.1 Standard EEG

- 5.3.2.1.2 Video EEG

- 5.3.2.1.3 Other EEG devices

- 5.3.2.2 EMG devices

- 5.3.2.3 MEG devices

- 5.3.2.4 Other monitoring devices

- 5.3.2.1 EEG devices

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals and clinics

- 6.3 Ambulatory surgical centers

- 6.4 Neurology centers

- 6.5 Diagnostic centers

- 6.6 Home care settings

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Boston Scientific Corporation

- 8.2 Cadwell Industries

- 8.3 Compumedics

- 8.4 Empatica

- 8.5 Koninklijke Philips

- 8.6 Masimo Corporation

- 8.7 Medpage

- 8.8 Medtronic

- 8.9 Natus Medical Incorporated

- 8.10 NeuroWave Systems

- 8.11 NIHON KOHDEN CORPORATION

- 8.12 Seer Medical

- 8.13 Stratus

- 8.14 The Magstim

- 8.15 Zeto