|

市场调查报告书

商品编码

1750471

暖通空调阀门市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测HVAC Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

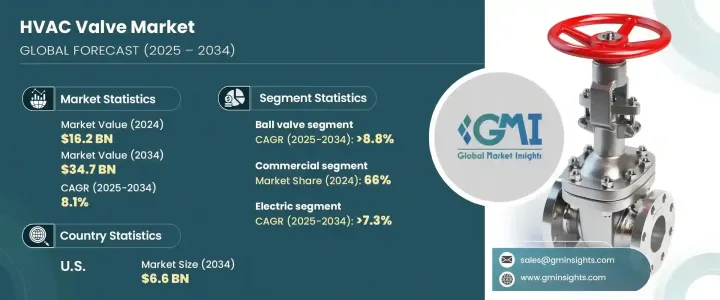

2024年,全球暖通空调阀门市场价值为162亿美元,预计到2034年将以8.1%的复合年增长率成长,达到347亿美元。这主要得益于全球建筑活动的激增,从而导致住宅、商业和工业领域对暖气、通风和空调 (HVAC) 系统的需求增加。阀门在这些系统中发挥着至关重要的作用,它透过调节流体流量、压力和温度来确保最佳性能和能源效率。

节能智慧建筑的趋势正在推动暖通空调阀门市场的发展。新建筑将先进的暖通空调系统与智慧阀门相结合,这些阀门配备感测器、连接和分析功能,可实现即时监控和控制。这些智慧阀门使设施管理人员能够优化能耗、及早发现故障并进行预测性维护,从而降低营运成本并延长设备使用寿命。将物联网 (IoT) 技术整合到暖通空调系统中,加速了对自动化和智慧阀门解决方案的需求。这些智慧阀门提供即时监控、远端存取和高级控制功能,使设施管理人员能够优化能源使用并提高系统响应能力。随着商业和工业建筑越来越多地采用智慧建筑框架,对能够与建筑管理系统 (BMS) 无缝通讯的阀门的需求也日益增长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 162亿美元 |

| 预测值 | 347亿美元 |

| 复合年增长率 | 8.1% |

2024年,球阀在暖通空调(HVAC)阀门市场占据了相当大的份额,达到4.3%。球阀之所以受欢迎,是因为它结构简单、关闭严密,并且适用于暖通空调系统中的气流和流体流量管理。球阀因其低扭矩、密封性和高耐用性而被广泛应用于新建和改造项目,这有助于提高供暖和製冷应用的效率和安全性。此外,球阀支援自动化技术,使其与智慧暖通空调系统相容。

2024年,商业领域占据暖通空调阀门市场的主导地位,占66%。办公室、购物中心、医院、饭店、资料中心和学校等商业建筑需要复杂的暖通空调系统来精确调节流体和气流。这些建筑采用智慧节能的暖通空调系统,是为了满足政府标准、降低成本并获得LEED等绿色认证。这一趋势推动了对先进暖通空调阀门的需求,这些阀门能够提供精确的控制并与楼宇管理系统整合。

2024年,美国暖通空调阀门市场占据67%的市场份额,预计到2034年将达到66亿美元,这得益于严格的能源效率法规和永续发展倡议,例如能源之星计画和加拿大的《能源效率法规》。这些法规鼓励采用高效的暖通空调系统,包括智慧阀门和基于物联网的阀门,以节省能源并符合环境标准。该地区对智慧建筑和自动化的关注进一步刺激了对兼容楼宇管理系统 (BMS) 的暖通空调阀门的需求。此外,旧建筑中现有暖通空调系统的改造也推动了对先进阀门解决方案的需求成长。

全球暖通空调阀门产业的主要参与者包括霍尼韦尔、江森自控、施耐德电气、西门子、搏力谋、丹佛斯、滨特尔、AVK、福斯、穆勒工业、Samson、Taco、Bray、Nexus 和 IDC。这些公司专注于产品创新、策略合作以及併购,以增强其市场影响力。开发具有智慧功能和增强性能的先进暖通空调阀门是领先製造商的重点关注领域。此外,各公司正在投资研发,以开发环保节能的解决方案,以满足对永续暖通空调系统日益增长的需求。

为了巩固市场地位,暖通空调阀门产业的企业正在采取多项关键策略。这些策略包括透过创新和技术进步来扩展产品组合,例如推出新的阀门设计和功能,以满足客户不断变化的需求。物联网和自动化等智慧技术的整合是市场的一个重要趋势,使製造商能够提供具有即时监控和控制功能的先进解决方案。与技术供应商、暖通空调系统製造商和分销商建立策略合作伙伴关係,使企业能够增强产品供应并覆盖更广泛的客户群。此外,併购也是市场整合和进入新市场和新技术的常见策略。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 製造商

- 原物料供应商

- 配销通路

- 川普政府关税的影响

- 贸易影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(客户成本)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 贸易影响

- 利润率分析

- 技术与创新格局

- 重要新闻和倡议

- 监管格局

- 对部队的影响

- 成长动力

- 不断发展的建筑业

- 都市化与智慧城市计划

- 气候变迁和极端天气

- 产业陷阱与挑战

- 初始成本高

- 对新兴市场的认知有限

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 产业结构与集中度

- 竞争强度评估

- 公司市占率分析

- 竞争定位矩阵

- 产品定位

- 性价比定位

- 地理分布

- 创新能力

- 战略仪表板

- 竞争基准测试

- 製造能力

- 产品组合实力

- 分销网络

- 研发投资

- 策略性倡议评估

- 关键参与者的 SWOT 分析

- 未来竞争前景

第五章:市场估计与预测:依阀门类型,2021 - 2034 年

- 主要趋势

- 球阀

- 截止阀

- 蝶阀

- 止回阀

- 闸阀

- 洩压阀

- 控制阀

- 电磁阀

- 其他的

第六章:市场估计与预测:按营运类型,2021 - 2034 年

- 主要趋势

- 手动的

- 气动

- 油压

- 电的

- 智慧/互联

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 暖气系统

- 冷却系统

- 通风系统

- 区域供冷

- 冷藏

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 住宅

- 商业的

- 办公大楼

- 零售

- 热情好客

- 卫生保健

- 教育机构

- 其他的

- 工业的

- 石油和天然气

- 製造业

- 食品和饮料

- 製药

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第十章:公司简介

- AVK

- Belimo

- Bray

- Danfoss

- Flowserve

- Honeywell

- IDC

- Johnson Controls

- Mueller Industries

- Nexus

- Pentair

- Samson

- Schneider Electric

- Siemens

The Global HVAC Valve Market was valued at USD 16.2 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 34.7 billion by 2034 driven by the surge in construction activities worldwide, leading to increased demand for heating, ventilation, and air conditioning (HVAC) systems across residential, commercial, and industrial sectors. Valves play a crucial role in these systems by regulating fluid flow, pressure, and temperature, ensuring optimal performance and energy efficiency.

The trend toward energy-efficient and smart buildings is propelling the HVAC valve market. New constructions incorporate advanced HVAC systems with intelligent valves featuring sensors, connectivity, and analytics for real-time monitoring and control. These smart valves enable facility managers to optimize energy consumption, detect faults early, and perform predictive maintenance, reducing operational costs and extending equipment lifespan. Integrating Internet of Things (IoT) technology into HVAC systems accelerates the demand for automated and intelligent valve solutions. These smart valves offer real-time monitoring, remote access, and advanced control capabilities, allowing facility managers to optimize energy usage and improve system responsiveness. As commercial and industrial buildings increasingly adopt smart building frameworks, the need for valves that seamlessly communicate with Building Management Systems (BMS) is rising.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.2 Billion |

| Forecast Value | $34.7 Billion |

| CAGR | 8.1% |

In 2024, ball valves held a significant share of the HVAC valve market, accounting for 4.3%. Their popularity is attributed to their simple structure, tight shut-off action, and suitability for airflow and fluid flow management in HVAC systems. Ball valves are widely used in new installations and retrofitting projects due to their low torque operation, close seal, and high durability, which contribute to the efficiency and asepsis of heating and cooling applications. Additionally, ball valves support automation technologies, making them compatible with smart HVAC systems.

The commercial sector dominated the HVAC valve market in 2024, representing a 66% share. Commercial buildings such as offices, shopping malls, hospitals, hotels, data centers, and schools require complex HVAC systems to regulate fluid and air flow accurately. The adoption of smart and energy-efficient HVAC systems in these buildings is driven by the need to comply with government standards, reduce costs, and achieve green certifications like LEED. This trend fuels the demand for advanced HVAC valves that offer precise control and integration with building management systems.

United States HVAC Valve Market held a 67% share in 2024 and is projected to generate USD 6.6 billion by 2034, driven by stringent energy efficiency regulations and sustainability initiatives, such as the Energy Star program and Canada's Energy Efficiency Regulations. These regulations are encouraging the adoption of efficient HVAC systems, including intelligent and IoT-based valves, to conserve energy and comply with environmental standards. The focus on smart buildings and automation in the region further supports the demand for Building Management System (BMS)-compatible HVAC valves. Additionally, the retrofitting of existing HVAC systems in older buildings is contributing to the increased demand for advanced valve solutions.

Key players in the Global HVAC Valve Industry include Honeywell, Johnson Controls, Schneider Electric, Siemens, Belimo, Danfoss, Pentair, AVK, Flowserve, Mueller Industries, Samson, Taco, Bray, Nexus, and IDC. These companies focus on product innovation, strategic partnerships, and mergers and acquisitions to strengthen their market presence. Developing advanced HVAC valves with smart features and enhanced performance is a key focus area for leading manufacturers. Additionally, companies are investing in research and development to develop eco-friendly and energy-efficient solutions to meet the growing demand for sustainable HVAC systems.

To strengthen their market presence, companies in the HVAC valve industry are adopting several key strategies. These include expanding their product portfolios through innovation and technological advancements, such as introducing new valve designs and features to cater to the evolving needs of customers. Integrating smart technologies, such as IoT and automation, is a significant trend in the market, enabling manufacturers to offer advanced solutions with real-time monitoring and control capabilities. Strategic partnerships and collaborations with technology providers, HVAC system manufacturers, and distributors enable companies to enhance their product offerings and reach a broader customer base. Additionally, mergers and acquisitions are common strategies for market consolidation and gaining access to new markets and technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Distribution channel

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact on forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing construction industry

- 3.8.1.2 Urbanization and smart city initiatives

- 3.8.1.3 Climate change and weather extremes

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial costs

- 3.8.2.2 Limited awareness in emerging markets

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Industry structure and concentration

- 4.2.1 Competitive intensity assessment

- 4.2.2 Company market share analysis

- 4.2.3 Competitive positioning matrix

- 4.3 Product positioning

- 4.3.1 Price-performance positioning

- 4.3.2 Geographic presence

- 4.3.3 Innovation capabilities

- 4.4 Strategic dashboard

- 4.5 Competitive benchmarking

- 4.5.1 Manufacturing capabilities

- 4.5.2 Product portfolio strength

- 4.5.3 Distribution network

- 4.5.4 R&D investments

- 4.6 Strategic initiatives assessment

- 4.7 SWOT analysis of key players

- 4.8 Future competitive outlook

Chapter 5 Market Estimates & Forecast, By Valve Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Ball valves

- 5.3 Globe valves

- 5.4 Butterfly valves

- 5.5 Check valves

- 5.6 Gate valves

- 5.7 Pressure relief valves

- 5.8 Control valves

- 5.9 Solenoid valves

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Operation Type, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Pneumatic

- 6.4 Hydraulic

- 6.5 Electric

- 6.6 Smart/connected

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Heating systems

- 7.3 Cooling systems

- 7.4 Ventilation systems

- 7.5 district cooling

- 7.6 Refrigeration

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Office buildings

- 8.3.2 Retail

- 8.3.3 hospitality

- 8.3.4 Healthcare

- 8.3.5 Educational institute

- 8.3.6 Others

- 8.4 Industrial

- 8.4.1 Oil and gas

- 8.4.2 Manufacturing

- 8.4.3 Food and beverage

- 8.4.4 Pharmaceuticals

- 8.4.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AVK

- 10.2 Belimo

- 10.3 Bray

- 10.4 Danfoss

- 10.5 Flowserve

- 10.6 Honeywell

- 10.7 IDC

- 10.8 Johnson Controls

- 10.9 Mueller Industries

- 10.10 Nexus

- 10.11 Pentair

- 10.12 Samson

- 10.13 Schneider Electric

- 10.14 Siemens

2025年全球内衬阀门市场报告2025年恆温混合阀(TMV)全球市场报告2025年负载感测阀全球市场报告

2025年全球内衬阀门市场报告2025年恆温混合阀(TMV)全球市场报告2025年负载感测阀全球市场报告 减压阀市场规模、份额、趋势及预测(按类型、工作压力、最终用户和地区),2025 年至 2033 年

减压阀市场规模、份额、趋势及预测(按类型、工作压力、最终用户和地区),2025 年至 2033 年 半导体 PFA 阀门市场(按类型、压力范围、尺寸、端口配置、机制、应用和销售管道)——2025-2030 年全球预测半导体阀门市场:2025-2030 年全球预测(按产品类型、阀门材料、流量、应用和分销管道)矩形头插头市场(按材料类型、尺寸、最终用途产业和分销管道)—2025-2030 年全球预测

半导体 PFA 阀门市场(按类型、压力范围、尺寸、端口配置、机制、应用和销售管道)——2025-2030 年全球预测半导体阀门市场:2025-2030 年全球预测(按产品类型、阀门材料、流量、应用和分销管道)矩形头插头市场(按材料类型、尺寸、最终用途产业和分销管道)—2025-2030 年全球预测 全球减压阀市场全球物联网阀门市场全球比例阀市场

全球减压阀市场全球物联网阀门市场全球比例阀市场