|

市场调查报告书

商品编码

1750489

碳纤维注入聚合物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Carbon Fiber-Infused Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

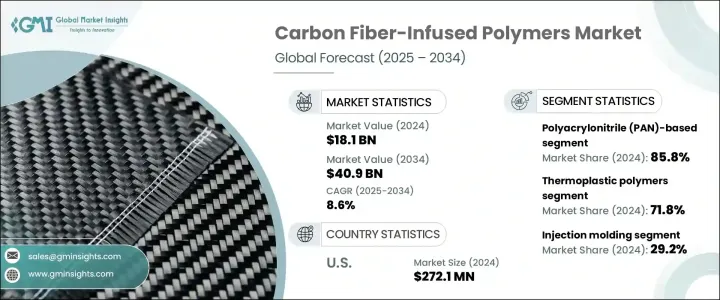

2024年,全球碳纤维注入聚合物市场价值为181亿美元,预计2034年将以8.6%的复合年增长率成长,达到409亿美元,这得益于汽车、航太、国防和再生能源等各行各业日益增长的需求。碳纤维注入聚合物的独特性能——例如高强度重量比、耐腐蚀性和热稳定性——使其成为需要轻质耐用材料的应用的理想选择。在汽车产业,这些材料有助于提高燃油效率并减少排放,符合严格的环境法规。

同样,在航太和国防领域,采用这些复合材料可以提高性能并降低营运成本。再生能源产业,尤其是风电领域,正持续受益于将碳纤维复合材料整合到涡轮叶片生产中。这些材料可以製造更轻、更耐用的叶片,在捕获风能的同时提高运作效率。其较高的强度重量比支持更长叶片的设计,从而在不损害结构完整性的情况下实现更大的能量输出——这对于陆上和海上大型风力发电设施至关重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 181亿美元 |

| 预测值 | 409亿美元 |

| 复合年增长率 | 8.6% |

在碳纤维注入聚合物市场中,按聚合物类型细分,突出了热塑性和热固性两种聚合物。热塑性聚合物在2024年占据了71.8%的市场份额,因其可回收性、快速加工时间以及耐受反覆加热和重塑的能力而受到青睐。这些特性使其在汽车和航太製造业的大批量应用领域颇具吸引力,在这些领域,永续性和成本效益正变得越来越重要。

注塑成型凭藉其能够大规模生产精密耐用的零件,在2024年占据了29.2%的市场。汽车产业尤其受益于这项工艺,因为它能够生产轻质且坚固的结构部件,有助于提高车辆性能和燃油效率。注塑成型对复杂几何形状的适应性以及与热塑性复合材料的兼容性进一步增强了其市场相关性。

受美国对创新和先进製造业策略投资的推动,美国碳纤维注入聚合物市场在2024年将占85%的市场。公共和私营部门的资金支持建立了专门的研究中心和试验平台,致力于优化复合材料的生产。这些努力旨在降低碳纤维的成本,并提高其在商业用途的性能,尤其是在国防、交通和清洁能源等关键领域。

全球碳纤维注入聚合物市场的主要公司包括东丽株式会社、帝人株式会社、赫氏株式会社、西格里碳素公司和索尔维公司。这些公司处于创新前沿,专注于开发先进材料和製造工艺,以满足各行各业日益增长的需求。为了巩固市场地位,碳纤维注入聚合物产业的公司正在采取多项策略倡议,包括投资研发以创新和改进材料性能、建立合资企业和合作伙伴关係以扩大市场覆盖范围,以及提升製造能力以满足日益增长的需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 原物料供应商

- 製造商

- 经销商

- 最终用途

- 利润率分析

- 新冠疫情导致的价值链中断

- 川普政府关税的影响—结构化概述

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 贸易统计(HS编码)

- 主要出口国

- 主要进口国

註:以上贸易统计仅针对重点国家。

- 利润率分析

- 重要新闻和倡议

- 技术格局

- 传统製造技术

- 先进製造技术

- 新兴技术

- 专利分析

- 监管格局

- 市场动态

- 市场驱动因素

- 汽车和航太工业对轻质材料的需求不断增加

- 越来越关注燃油效率和减排

- 在运动和休閒应用的采用率不断上升

- 扩大再生能源领域

- 製造工艺的技术进步

- 产业陷阱与挑战

- 生产成本高

- 复杂的製造工艺

- 回收和报废挑战

- 供应链漏洞

- 市场驱动因素

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 市占率分析

- 竞争仪錶板

- 策略倡议

- 併购

- 合资企业

- 产品发布

- 扩张计划

- 研发投资

- 竞争基准测试

- 供应商采用矩阵

- 竞争定位矩阵

第五章:市场估计与预测:按聚合物类型,2021 - 2034 年

- 主要趋势

- 热塑性聚合物

- 聚酰胺(PA)

- 聚丙烯(PP)

- 聚醚醚酮(PEEK)

- 聚苯硫醚(PPS)

- 聚醚酰亚胺(PEI)

- 其他的

- 热固性聚合物

- 环氧树脂

- 聚酯纤维

- 乙烯基酯

- 聚氨酯

- 其他的

第六章:市场估计与预测:依碳纤维类型,2021 - 2034 年

- 主要趋势

- 聚丙烯腈(PAN)基

- 标准模量

- 中间模量

- 高模量

- 基于音调

- 人造丝基

- 再生碳纤维

第七章:市场估计与预测:按製造工艺,2021 - 2034 年

- 主要趋势

- 射出成型

- 压缩成型

- 树脂传递模塑

- 拉挤成型

- 纤维缠绕

- 增材製造

- 其他的

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 航太与国防

- 飞机部件

- 空间应用

- 国防装备

- 汽车

- 结构部件

- 内装部件

- 动力总成部件

- 电动汽车应用

- 风能

- 刀片

- 机舱

- 其他组件

- 运动与休閒

- 自行车

- 网球拍

- 高尔夫球桿

- 其他的

- 建造

- 加固材料

- 结构部件

- 其他的

- 海洋

- 船体结构

- 甲板组件

- 其他的

- 医疗的

- 义肢

- 影像设备

- 其他的

- 工业设备

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Carbon Fiber Composite Design

- Composite Horizons LLC

- Cytec Industries Inc.

- DowAksa

- Formosa Plastics Corporation

- Hexcel Corporation

- Hyosung Advanced Materials

- Kureha Corporation

- Mitsubishi Chemical Holdings Corporation

- Nippon Carbon Co., Ltd.

- Plasan Carbon Composites

- SABIC

- SGL Carbon

- Sigmatex

- Solvay SA

- Teijin Limited

- Toho Tenax Co., Ltd.

- Toray Industries, Inc.

- Zhongfu Shenying Carbon Fiber Co., Ltd.

- Zoltek Companies, Inc.

The Global Carbon Fiber-Infused Polymers Market was valued at USD 18.1 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 40.9 billion by 2034, driven by the increasing demand across various industries, including automotive, aerospace, defense, and renewable energy sectors. The unique properties of carbon fiber-infused polymers-such as high strength-to-weight ratios, corrosion resistance, and thermal stability-make them ideal for applications requiring lightweight and durable materials. In the automotive industry, these materials contribute to fuel efficiency and reduced emissions, aligning with stringent environmental regulations.

Similarly, in aerospace and defense, adopting these composites enhances performance and reduces operational costs. The renewable energy industry, especially the wind power segment, continues to gain from integrating carbon fiber composites into turbine blade production. These materials allow lighter, more durable blades that capture wind energy while enhancing operational efficiency. Their high strength-to-weight ratio supports the design of longer blades, which leads to greater energy output without compromising structural integrity-an essential factor for large-scale wind installations both onshore and offshore.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.1 Billion |

| Forecast Value | $40.9 Billion |

| CAGR | 8.6% |

Within the carbon fiber-infused polymers market, segmentation by polymer type highlights thermoplastic and thermoset variants. The thermoplastic polymers segment held 71.8% share in 2024, favored for their recyclability, fast processing times, and ability to withstand repeated heating and reshaping. These features make them attractive for high-volume applications in automotive and aerospace manufacturing, where sustainability and cost-efficiency are becoming increasingly important.

The injection molding segment held a 29.2% share in 2024 due to its ability to deliver precise, durable parts at scale. The automotive sector, in particular, benefits from this process, as it enables the production of lightweight yet robust structural parts that contribute to improved vehicle performance and fuel efficiency. Injection molding's adaptability to complex geometries and compatibility with thermoplastic composites further amplify its market relevance.

United States Carbon Fiber-Infused Polymers Market held 85% share in 2024, driven by the nation's strategic investment in innovation and advanced manufacturing. Public and private sector funding has facilitated the establishment of dedicated research centers and test beds focused on optimizing composite material production. These efforts aim to lower the cost of carbon fiber and improve its performance for commercial use, particularly in key sectors like defense, mobility, and clean energy.

Key companies operating in the Global Carbon Fiber-Infused Polymers Market include Toray Industries Inc., Teijin Limited, Hexcel Corporation, SGL Carbon, and Solvay S.A. These companies are at the forefront of innovation, focusing on developing advanced materials and manufacturing processes to meet the growing demands of various industries. To strengthen their market position, companies in the carbon fiber-infused polymers industry are adopting several strategic initiatives. These include investing in research and development to innovate and improve material properties, establishing joint ventures and partnerships to expand market reach, and enhancing manufacturing capabilities to meet increasing demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research methodology

- 1.1.1 Initial data exploration

- 1.1.2 Primary research methodology

- 1.1.3 Secondary research methodology

- 1.1.4 Market size estimation approach

- 1.1.5 Data triangulation techniques

- 1.1.6 Research assumptions

- 1.2 Market definition and scope

- 1.2.1 Base year and forecast period

- 1.2.2 Market segmentation

- 1.2.3 Regional scope

- 1.2.4 Currency conversion rates

- 1.3 Information procurement

- 1.3.1 Purchased database

- 1.3.2 GMI's internal database

- 1.3.3 Secondary sources

- 1.3.4 Primary research

- 1.4 Information analysis

- 1.4.1 Data analysis models

- 1.4.2 Market breakdown and data triangulation

Chapter 2 Executive Summary

- 2.1 Carbon fiber-infused polymers industry 3600 synopsis, 2021-2034

- 2.1.1 Business trends

- 2.1.2 Regional trends

- 2.1.3 Polymer type trends

- 2.1.4 Carbon fiber type trends

- 2.1.5 Manufacturing process trends

- 2.1.6 End use industry trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Manufacturers

- 3.1.3 Distributors

- 3.1.4 End use

- 3.1.5 Profit margin analysis

- 3.1.6 Value chain disruptions due to COVID-19

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.5.1 Technology landscape

- 3.5.2 Traditional manufacturing technologies

- 3.5.3 Advanced manufacturing technologies

- 3.5.4 Emerging technologies

- 3.5.5 Patent analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Market dynamics

- 3.7.1 Market drivers

- 3.7.1.1 Increasing demand for lightweight materials in the automotive and aerospace industries

- 3.7.1.2 Growing focus on fuel efficiency and emission reduction

- 3.7.1.3 Rising adoption in sports and leisure applications

- 3.7.1.4 Expanding the renewable energy sector

- 3.7.1.5 Technological advancements in manufacturing processes

- 3.7.2 Industry pitfalls and challenges

- 3.7.2.1 High production costs

- 3.7.2.2 Complex manufacturing processes

- 3.7.2.3 Recycling and end-of-life challenges

- 3.7.2.4 Supply chain vulnerabilities

- 3.7.1 Market drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.9.1 Supplier power

- 3.9.2 Buyer power

- 3.9.3 Threat of new entrants

- 3.9.4 Threat of substitutes

- 3.9.5 Industry rivalry

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis, 2024

- 4.2 Competitive dashboard

- 4.3 Strategic initiatives

- 4.3.1 Mergers & acquisitions

- 4.3.2 Joint ventures

- 4.3.3 Product launches

- 4.3.4 Expansion plans

- 4.3.5 R&D investments

- 4.4 Competitive benchmarking

- 4.5 Vendor adoption matrix

- 4.6 Competitive positioning matrix

Chapter 5 Market Estimates and Forecast, By Polymer Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Thermoplastic polymers

- 5.2.1 Polyamide (PA)

- 5.2.2 Polypropylene (PP)

- 5.2.3 Polyether ether ketone (PEEK)

- 5.2.4 Polyphenylene sulfide (PPS)

- 5.2.5 Polyetherimide (PEI)

- 5.2.6 Others

- 5.3 Thermoset polymers

- 5.3.1 Epoxy

- 5.3.2 Polyester

- 5.3.3 Vinyl ester

- 5.3.4 Polyurethane

- 5.3.5 Others

Chapter 6 Market Estimates and Forecast, By Carbon Fiber Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Polyacrylonitrile (PAN)-based

- 6.2.1 Standard modulus

- 6.2.2 Intermediate modulus

- 6.2.3 High modulus

- 6.3 Pitch-based

- 6.4 Rayon-based

- 6.5 Recycled carbon fiber

Chapter 7 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Injection molding

- 7.3 Compression molding

- 7.4 Resin transfer molding

- 7.5 Pultrusion

- 7.6 Filament winding

- 7.7 Additive manufacturing

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.2.1 Aircraft components

- 8.2.2 Space applications

- 8.2.3 Defense equipment

- 8.3 Automotive

- 8.3.1 Structural components

- 8.3.2 Interior components

- 8.3.3 Powertrain components

- 8.3.4 Electric vehicle applications

- 8.4 Wind energy

- 8.4.1 Blades

- 8.4.2 Nacelles

- 8.4.3 Other components

- 8.5 Sports & leisure

- 8.5.1 Bicycles

- 8.5.2 Tennis rackets

- 8.5.3 Golf clubs

- 8.5.4 Others

- 8.6 Construction

- 8.6.1 Reinforcement materials

- 8.6.2 Structural components

- 8.6.3 Others

- 8.7 Marine

- 8.7.1 Hull structures

- 8.7.2 Deck components

- 8.7.3 Others

- 8.8 Medical

- 8.8.1 Prosthetics

- 8.8.2 Imaging equipment

- 8.8.3 Others

- 8.9 Industrial equipment

- 8.10 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Carbon Fiber Composite Design

- 10.2 Composite Horizons LLC

- 10.3 Cytec Industries Inc.

- 10.4 DowAksa

- 10.5 Formosa Plastics Corporation

- 10.6 Hexcel Corporation

- 10.7 Hyosung Advanced Materials

- 10.8 Kureha Corporation

- 10.9 Mitsubishi Chemical Holdings Corporation

- 10.10 Nippon Carbon Co., Ltd.

- 10.11 Plasan Carbon Composites

- 10.12 SABIC

- 10.13 SGL Carbon

- 10.14 Sigmatex

- 10.15 Solvay S.A.

- 10.16 Teijin Limited

- 10.17 Toho Tenax Co., Ltd.

- 10.18 Toray Industries, Inc.

- 10.19 Zhongfu Shenying Carbon Fiber Co., Ltd.

- 10.20 Zoltek Companies, Inc.

全球碳纤维结构修復市场

全球碳纤维结构修復市场 全球碳纤维建筑修復市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球碳纤维建筑修復市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 碳纤维和碳纤维增强塑胶市场-全球产业规模、份额、趋势、机会和预测,按原料类型(聚丙烯腈、沥青和人造丝)、製造流程、最终用户、地区和竞争细分,2020 年至 2030 年全球碳纤维复合材料市场

碳纤维和碳纤维增强塑胶市场-全球产业规模、份额、趋势、机会和预测,按原料类型(聚丙烯腈、沥青和人造丝)、製造流程、最终用户、地区和竞争细分,2020 年至 2030 年全球碳纤维复合材料市场 CF 和 CFRP 市场(按树脂类型、前体类型、产地、製造流程、最终用途产业和地区划分)- 预测至 2030 年

CF 和 CFRP 市场(按树脂类型、前体类型、产地、製造流程、最终用途产业和地区划分)- 预测至 2030 年 2034年碳纤维全球市场机会与策略全球大丝束碳纤维市场全球碳纤维市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

2034年碳纤维全球市场机会与策略全球大丝束碳纤维市场全球碳纤维市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 碳纤维的全球市场:各原料,各纤维束尺寸,各用途,各终端用户业界,各地区,机会,预测,2018年~2032年全球碳纤维树脂市场-依树脂类型、应用、地区、预测的市场规模

碳纤维的全球市场:各原料,各纤维束尺寸,各用途,各终端用户业界,各地区,机会,预测,2018年~2032年全球碳纤维树脂市场-依树脂类型、应用、地区、预测的市场规模