|

市场调查报告书

商品编码

1750493

PVT 收集器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测PVT Collectors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

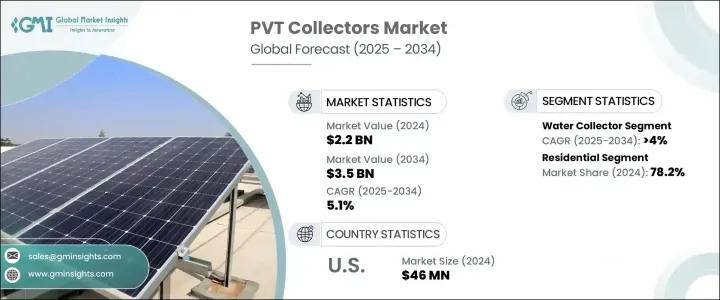

2024年,全球光电集热器市场规模达22亿美元,预计2034年将以5.1%的复合年增长率成长,达到35亿美元。偏远地区和离网地区对混合太阳能係统的需求日益增长,这加速了光电集热器在全球的普及。这些系统将光伏和热能技术整合到一块面板中,同时提供电力和热能。透过高效利用太阳能,光伏集热器有助于减少对传统燃料来源的依赖,提供经济高效且永续的能源解决方案。服务欠缺地区日益增多的电气化计画预计将进一步推动这一需求,尤其是在能源基础设施有限的地区。

除了农村电气化之外,人们对混合再生能源系统在建筑能源管理中日益增长的兴趣也推动了光伏集热器的广泛应用。这些系统可以节省空间,实现双能源输出,同时最大限度地降低土地使用和安装成本。随着城市地区交通日益拥堵,人们越来越关注能够以最小面积实现最大发电量的技术。光电集热器恰好满足了这项需求,为人口密集地区提供了切实可行的解决方案。随着更严格的法规鼓励节能低排放的建筑实践,政府也在推动向光伏系统等综合再生能源技术转变方面发挥关键作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 22亿美元 |

| 预测值 | 35亿美元 |

| 复合年增长率 | 5.1% |

PVT集热器与热泵等其他绿色技术的日益融合,进一步刺激了市场成长。这种组合能够提高生活热水系统和空间加热解决方案的能源效率。 PVT集热器与热泵之间的协同作用显着节约能源,使其成为寻求性能优化和成本降低的住宅和商业能源消费者的可行选择。随着越来越多的公司和机构开发此类整合解决方案,市场渗透率预计将加速成长。

影响市场动态的另一个重要趋势是住宅和商业建筑对高效低温供热的需求日益增长。光电系统 (PVT) 可以满足这一需求,同时也能提供发电的额外优势,所有这些都只需一个屋顶单元即可完成。随着分散式能源系统在全球的普及,像光伏集热器这样的双发电装置因其高投资回报率而越来越受到青睐。这些系统可以提高建筑的整体能源性能,尤其是在屋顶空间有限的城市住宅区。这种高效率正推动建筑一体化太阳能解决方案日益普及,尤其是在业主和开发商寻求在不影响能源产出的情况下实现永续发展目标的情况下。

儘管前景乐观,但一些监管和政策相关的挑战正在影响该行业。太阳能电池和热电联产机组等光电模组的高额进口关税推高了系统价格,并减缓了其普及速度,尤其是在严重依赖进口技术的市场。这一成本壁垒限制了先进且高效系统的普及,并延长了大型专案的部署时间,这可能会减缓某些地区的成长。

就产品细分而言,PVT集热器市场分为水集热器、空气集热器和聚光系统。其中,水集热器市场预计到2034年将以超过4%的复合年增长率扩张。这些系统因其能够在各种气候条件下提供可靠的热输出而日益普及,支持其在已开发市场和发展中市场的广泛应用。它们与节能计划的兼容性使其成为致力于长期脱碳的机构和企业的首选。

按应用领域划分,光电市场分为住宅和商业领域。 2024年,住宅领域占据全球市场78.2%的主导地位。这一强劲增长源于日益加重的公共事业费用负担以及房主对能源自给自足的日益偏好。紧凑的设计和双能源输出使光伏系统成为住宅建筑的理想选择,尤其是在空间有限的城市地区。政府支持的太阳能技术应用激励措施和返利计划进一步鼓励了家庭层面的安装,从而增强了该领域的成长。

在美国,PVT 集热器市场呈现稳定成长,到 2024 年将达到 4,600 万美元,高于 2023 年的 4,300 万美元和 2022 年的 4,100 万美元。北美目前占全球市场的 2.3%,预计到 2034 年这一数字将稳定上升。美国几个州的高电价促使消费者探索 PVT 系统等替代能源,以降低公用事业成本并减少对电网的依赖。

该产业的领导企业合计占全球约39.5%的市场。这些公司透过垂直整合保持竞争优势,涵盖从研发、製造到安装和服务的各个环节。他们与建筑和暖通空调公司的合作进一步巩固了其市场地位,确保了无缝的系统相容性和优化的性能。在研发方面的大量投入促成了新一代PVT面板的推出,这些面板具有卓越的能量输出,并配备了先进的监控技术。这些发展不仅提高了系统效率,也符合全球对永续净零能耗建筑日益增长的承诺。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率

- 战略仪表板

- 策略倡议

- 竞争基准测试

- 创新与永续发展格局

第五章:市场规模及预测:依类型,2021 - 2034

- 主要趋势

- 集水器

- 覆盖

- 裸露

- 真空管

- 空气收集器

- 集中器

第六章:市场规模及预测:依应用,2021 - 2034

- 主要趋势

- 住宅

- 商业的

第七章:市场规模及预测:依地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 义大利

- 希腊

- 波兰

- 法国

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 中东和北非

- 以色列

- 约旦

- 黎巴嫩

- 摩洛哥

- 世界其他地区

第八章:公司简介

- Abora Solar

- Balkansolar

- Dualsun

- Naked Energy

- NIBE Energy

- PowerPanel

- SolarPower

- Solimpeks

- SunEarth

- Sunmaxx

The Global Photovoltaic Thermal Collectors Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 3.5 billion by 2034. Increasing demand for hybrid solar energy systems in remote and off-grid locations is accelerating the adoption of PVT collectors worldwide. These systems combine photovoltaic and thermal technologies into a single panel, offering both electricity and heat. By efficiently utilizing solar energy, PVT collectors help reduce reliance on conventional fuel sources, offering cost-effective and sustainable energy solutions. Growing electrification initiatives in underserved areas are expected to further drive this demand, particularly in regions with limited energy infrastructure.

In addition to rural electrification, growing interest in hybrid renewable systems in building energy management is encouraging the broader use of PVT collectors. These systems allow for space-efficient installations that deliver dual energy outputs while minimizing land use and installation costs. As urban areas become more congested, there is an increasing focus on technologies that enable maximum energy generation from minimal surface area. PVT collectors fit this requirement well, offering a practical solution for densely populated areas. With stricter regulations encouraging energy-efficient and low-emission building practices, governments are also playing a key role in driving the shift toward integrated renewable technologies like PVT systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.5 Billion |

| CAGR | 5.1% |

Market growth is being further stimulated by the increasing integration of PVT collectors with other green technologies, such as heat pumps. The combination enables greater energy efficiency in both domestic hot water systems and space heating solutions. The synergy between PVT panels and heat pumps contributes to notable energy savings, making it a viable option for both residential and commercial energy consumers seeking performance optimization and cost reduction. As more companies and institutions develop these integrated solutions, market penetration is expected to accelerate.

Another important trend shaping market dynamics is the rising need for efficient low-temperature heat in residential and commercial buildings. PVT systems can meet this demand while offering the added benefit of electricity generation, all from a single rooftop unit. As decentralized energy systems gain traction globally, dual-generation units like PVT collectors are increasingly preferred for their high return on investment. These systems enhance overall building energy performance, especially in urban residential spaces where rooftop space is limited. This efficiency is contributing to the growing popularity of building-integrated solar solutions, especially as property owners and developers seek ways to meet sustainability targets without compromising on energy output.

Despite the positive outlook, some regulatory and policy-related challenges are impacting the industry. High import duties on PVT components such as solar cells and thermal units have increased system prices and slowed adoption, especially in markets heavily dependent on imported technology. This cost barrier limits access to advanced, high-efficiency systems and extends the deployment timeline for larger projects, potentially slowing growth in some regions.

In terms of product segmentation, the PVT collectors market is categorized into water collectors, air collectors, and concentrator systems. Among these, the water collectors segment is projected to expand at a CAGR exceeding 4% through 2034. These systems are gaining popularity for their ability to deliver reliable thermal output in a wide range of climatic conditions, supporting broader adoption in both developed and developing markets. Their compatibility with energy-saving initiatives makes them a preferred option for institutions and enterprises targeting long-term decarbonization.

By application, the market is split between residential and commercial sectors. The residential segment accounted for a dominant 78.2% share of global revenue in 2024. This strong presence is due to the increasing burden of utility bills and a rising preference among homeowners for energy self-sufficiency. The compact design and dual-energy output make PVT systems ideal for residential buildings, especially in urban areas where space is limited. Government-backed incentives and rebate programs for solar technology adoption further encourage household-level installations, reinforcing the growth of this segment.

In the United States, the PVT collectors market has shown steady growth, reaching USD 46 million in 2024, up from USD 43 million in 2023 and USD 41 million in 2022. North America currently holds a 2.3% share of the global market, a figure expected to rise steadily through 2034. High electricity prices in several US states are driving consumers to explore alternative energy sources like PVT systems to cut down on utility costs and reduce grid dependency.

Leading players in the industry collectively account for around 39.5% of the global market share. These companies maintain competitive advantages through vertical integration, managing everything from R&D and manufacturing to installation and service. Their partnerships with construction and HVAC firms further enhance their market position, ensuring seamless system compatibility and optimized performance. Heavy investment in R&D has led to the rollout of new-generation PVT panels that offer superior energy output and are equipped with advanced monitoring technologies. These developments not only improve system efficiency but also align with growing global commitments to sustainable, net-zero energy buildings.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Type, 2021 - 2034 (USD Million, m2 & MW)

- 5.1 Key trends

- 5.2 Water collectors

- 5.2.1 Covered

- 5.2.2 Uncovered

- 5.2.3 Evacuated tube

- 5.3 Air collectors

- 5.4 Concentrators

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million, m2 & MW)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, m2 & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Greece

- 7.3.4 Poland

- 7.3.5 France

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.5 Middle East & North Africa

- 7.5.1 Israel

- 7.5.2 Jordan

- 7.5.3 Lebanon

- 7.5.4 Morocco

- 7.6 Rest of World

Chapter 8 Company Profiles

- 8.1 Abora Solar

- 8.2 Balkansolar

- 8.3 Dualsun

- 8.4 Naked Energy

- 8.5 NIBE Energy

- 8.6 PowerPanel

- 8.7 SolarPower

- 8.8 Solimpeks

- 8.9 SunEarth

- 8.10 Sunmaxx

2026-2030年全球聚光太阳能集热器市场

2026-2030年全球聚光太阳能集热器市场 太阳能集热器市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测

太阳能集热器市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测 太阳能集热器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

太阳能集热器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 太阳能集热器市场-2025年至2030年预测

太阳能集热器市场-2025年至2030年预测 PVT(光伏-热能)集热器市场,按材料类型、集热器类型、安装类型、技术、应用、国家/地区划分 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测非聚光太阳能集热器市场,按吸收板、按应用、按国家和地区划分-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

PVT(光伏-热能)集热器市场,按材料类型、集热器类型、安装类型、技术、应用、国家/地区划分 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测非聚光太阳能集热器市场,按吸收板、按应用、按国家和地区划分-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测 聚光太阳能集热器市场-全球产业规模、份额、趋势、机会和预测(按类型、按技术、按最终用途行业、按地区和按竞争细分,2020-2030 年)

聚光太阳能集热器市场-全球产业规模、份额、趋势、机会和预测(按类型、按技术、按最终用途行业、按地区和按竞争细分,2020-2030 年) 全球太阳能集热管市场

全球太阳能集热管市场 2032 年非聚光太阳能集热器市场预测:按类型、吸收板、最终用户和地区进行的全球分析太阳能集热管市场 - 全球产业规模、份额、趋势、机会和预测,细分,按类型、按最终用户、按系统类型、按地区、按竞争,2020-2030F

2032 年非聚光太阳能集热器市场预测:按类型、吸收板、最终用户和地区进行的全球分析太阳能集热管市场 - 全球产业规模、份额、趋势、机会和预测,细分,按类型、按最终用户、按系统类型、按地区、按竞争,2020-2030F