|

市场调查报告书

商品编码

1750596

生物感测器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Biosensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

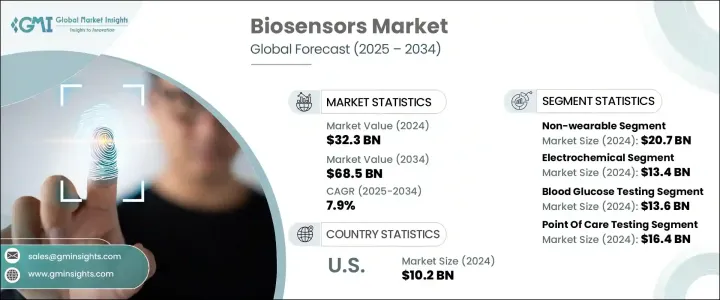

2024年,全球生物感测器市场规模达323亿美元,预计2034年将以7.9%的复合年增长率成长,达到685亿美元。这得益于生物感测器在多个领域(尤其是医疗保健领域)的应用日益增多,生物感测器在检测生物讯号方面发挥着至关重要的作用。这些设备灵敏度高、精准度高,能够快速检测生物标记,有助于早期诊断各种疾病。此外,生物感测器在药物研发和生物医药领域的应用日益广泛,也进一步支撑了市场的成长。便携式生物感测器的需求不断增长,尤其是在亚太和欧洲等地区,加上技术进步,是推动该产业发展的关键因素。

推动生物感测器市场成长的另一个关键因素是糖尿病和心血管疾病等慢性疾病的日益流行,这些疾病需要持续监测和管理,以避免严重的併发症。例如,如果不加以控制,糖尿病可能导致严重的健康问题,如肾衰竭、中风或下肢截肢。这导致对能够即时监测血糖水平的设备的需求日益增长,使患者能够在必要时立即采取行动。除了糖尿病之外,心血管疾病的发生率也在上升,因此对透过生物感测器等先进诊断工具进行早期发现和持续管理的需求日益增长。这些技术透过提供及时资料,帮助制定更精准的治疗方案,有助于改善患者的治疗效果。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 323亿美元 |

| 预测值 | 685亿美元 |

| 复合年增长率 | 7.9% |

2024年,非穿戴式生物感测器市场规模达207亿美元。这些感测器整合到用于即时诊断的诊断设备中,因其易用性、高精度以及无需用户持续互动即可提供即时结果的能力而备受青睐。随着医疗保健提供者寻求高效及时的诊断工具,预计对这些非穿戴式装置的需求将会成长。诸如灵敏度提升、微型化和数位连接等技术创新,增强了它们在临床环境中的有效性和可用性。

电化学生物感测器领域占据相当大的市场份额,占41.6%,2024年达到134亿美元。这些生物感测器广泛应用于医疗设备,例如糖尿病患者的血糖仪以及监测心臟生物标记和血液气体的系统。心血管疾病和糖尿病等慢性疾病的盛行率不断上升,推动了对电化学感测器作为重要诊断工具的需求。

受慢性病病例(尤其是糖尿病和心臟病)数量不断增长的推动,美国生物感测器市场在2024年达到了102亿美元的产值。儘管监管环境严格,美国仍然是包括生物感测器在内的创新医疗技术开发、批准和商业化的中心。 FDA等监管机构越来越重视加快新型生物感测器技术的审批流程,并认识到其在改善医疗保健结果方面的关键作用。

为了巩固市场地位,各公司正专注于创新和合作。许多公司在研发方面投入巨资,以开发灵敏度和精度更高的更先进的生物感测器技术。与医疗保健提供者和研究机构的合作有助于推动创新。此外,一些公司正在努力扩展其产品组合,以满足各种医疗需求,例如针对特定疾病的生物感测器和穿戴式健康监测设备。赛默飞世尔科技、Masimo 和丹纳赫等市场领导者正在采用这些策略来提升其市场占有率,并在这个快速成长的行业中保持竞争力。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 生物感测器在医疗领域的应用日益广泛

- 全球糖尿病盛行率上升

- 亚太地区和欧洲对便携式生物感测器的需求很高

- 不断进步的技术

- 产业陷阱与挑战

- 严格的监管情景

- 产品开发成本高

- 成长动力

- 成长潜力分析

- 监管格局

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 各国应对措施

- 对产业的影响

- 供应方影响(製造成本)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(消费者成本)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(製造成本)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 穿戴

- 不可穿戴

第六章:市场估计与预测:按技术,2021 年至 2034 年

- 主要趋势

- 电化学

- 光学的

- 热的

- 压电

- 其他技术

第七章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 血糖检测

- 胆固醇检测

- 血气分析

- 妊娠测试

- 药物研发

- 传染病检测

- 其他应用

第八章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 即时检验

- 家庭医疗保健诊断

- 研究实验室

- 其他最终用户

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 瑞士

- 亚太地区

- 中国

- 日本

- 印度

- 拉丁美洲

- 巴西

- 墨西哥

- 中东和非洲

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Abbott Laboratories

- ARKRAY

- Bio-Rad Laboratories

- Biosensors International Group

- Dexcom

- Danaher

- F. Hoffmann-La Roche

- Masimo

- Nova Biomedical

- Platinum Equity Advisors

- PHC Holdings

- Pinnacle Technology

- Siemens Healthineers

- Thermo Fisher Scientific

- Trividia Health

目录

第 11 章:方法论与范围

第 12 章:执行摘要

第 13 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 生物感测器在医疗领域的应用日益广泛

- 全球糖尿病盛行率上升

- 亚太地区和欧洲对便携式生物感测器的需求很高

- 不断进步的技术

- 产业陷阱与挑战

- 严格的监管情景

- 产品开发成本高

- 成长动力

- 成长潜力分析

- 监管格局

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 各国应对措施

- 对产业的影响

- 供应方影响(製造成本)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(消费者成本)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(製造成本)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第 14 章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 15 章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 穿戴

- 不可穿戴

第 16 章:市场估计与预测:按技术,2021 年至 2034 年

- 主要趋势

- 电化学

- 光学的

- 热的

- 压电

- 其他技术

第 17 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 血糖检测

- 胆固醇检测

- 血气分析

- 妊娠测试

- 药物研发

- 传染病检测

- 其他应用

第 18 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 即时检验

- 家庭医疗保健诊断

- 研究实验室

- 其他最终用户

第 19 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 瑞士

- 亚太地区

- 中国

- 日本

- 印度

- 拉丁美洲

- 巴西

- 墨西哥

- 中东和非洲

- 南非

- 沙乌地阿拉伯

第二十章:公司简介

- Abbott Laboratories

- ARKRAY

- Bio-Rad Laboratories

- Biosensors International Group

- Dexcom

- Danaher

- F. Hoffmann-La Roche

- Masimo

- Nova Biomedical

- Platinum Equity Advisors

- PHC Holdings

- Pinnacle Technology

- Siemens Healthineers

- Thermo Fisher Scientific

- Trividia Health

The Global Biosensors Market was valued at USD 32.3 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 68.5 billion by 2034, driven by increasing applications of biosensors across several sectors, particularly healthcare, where they play a crucial role in detecting biological signals. These devices offer high sensitivity and precision, allowing for the quick detection of biomarkers that aid in the early diagnosis of various diseases. Additionally, the expanding use of biosensors in drug discovery and biomedicine further supports the market's growth. The growing demand for portable biosensors, especially in regions like Asia Pacific and Europe, alongside technological advancements, is key factor propelling the industry.

Another key factor driving the growth of the biosensors market is the increasing prevalence of chronic conditions, such as diabetes and cardiovascular diseases, which require continuous monitoring and management to avoid serious complications. For example, diabetes, if left unmanaged, can lead to severe health issues like kidney failure, stroke, or lower limb amputations. This has led to a growing demand for devices that can offer real-time monitoring of blood glucose levels, allowing patients to take immediate action when necessary. In addition to diabetes, cardiovascular diseases are also on the rise, creating an increasing need for early detection and ongoing management through advanced diagnostic tools like biosensors. These technologies are helping improve patient outcomes by providing timely data that allows for more precise treatment plans.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $32.3 Billion |

| Forecast Value | $68.5 Billion |

| CAGR | 7.9% |

The non-wearable biosensor segment accounted for USD 20.7 billion in 2024. These sensors, integrated into diagnostic devices used for point-of-care testing, are valued for their ease of use, high accuracy, and ability to provide immediate results without continuous user interaction. As healthcare providers seek efficient and timely diagnostic tools, the demand for these non-wearable devices is expected to rise. Technological innovations such as improved sensitivity, miniaturization, and digital connectivity enhance their effectiveness and usability in clinical settings.

The electrochemical biosensor segment holds a substantial share of the market, representing 41.6% share, which was USD 13.4 billion in 2024. These biosensors are widely used in medical devices such as glucose meters for diabetic patients and in systems that monitor cardiac biomarkers and blood gases. The increasing prevalence of chronic conditions, including cardiovascular diseases and diabetes, drives the demand for electrochemical sensors as essential diagnostic tools.

United States Biosensors Market generated USD 10.2 billion in 2024, driven by the rising number of chronic disease cases, especially diabetes and heart-related conditions. Despite a strict regulatory environment, the U.S. remains a hub for the development, approval, and commercialization of innovative medical technologies, including biosensors. Regulatory bodies like the FDA are increasingly focused on accelerating the approval process for new biosensor technologies, recognizing their critical role in improving healthcare outcomes.

To strengthen their position in the market, companies are focusing on innovation and partnerships. Many firms invest heavily in R&D to develop more advanced biosensor technologies with greater sensitivity and precision. Collaborations with healthcare providers and research institutions help in driving innovation. Furthermore, some companies are working to expand their product portfolios to cater to various medical needs, such as disease-specific biosensors and wearable health monitoring devices. Market leaders, such as Thermo Fisher Scientific, Masimo, and Danaher, are adopting these strategies to enhance their market presence and remain competitive in this rapidly growing industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing application of biosensors in medical field

- 3.2.1.2 Rising prevalence of diabetes globally

- 3.2.1.3 High demand for portable biosensors in Asia Pacific and Europe

- 3.2.1.4 Increasing technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 High cost of product development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Wearable

- 5.3 Non-wearable

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Electrochemical

- 6.3 Optical

- 6.4 Thermal

- 6.5 Piezoelectric

- 6.6 Other technologies

Chapter 7 Market Estimates and Forecast, By Applications, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Blood glucose testing

- 7.3 Cholesterol testing

- 7.4 Blood gas analysis

- 7.5 Pregnancy testing

- 7.6 Drug discovery

- 7.7 Infectious disease testing

- 7.8 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Point of care testing

- 8.3 Home healthcare diagnostics

- 8.4 Research laboratories

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Switzerland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 ARKRAY

- 10.3 Bio-Rad Laboratories

- 10.4 Biosensors International Group

- 10.5 Dexcom

- 10.6 Danaher

- 10.7 F. Hoffmann-La Roche

- 10.8 Masimo

- 10.9 Nova Biomedical

- 10.10 Platinum Equity Advisors

- 10.11 PHC Holdings

- 10.12 Pinnacle Technology

- 10.13 Siemens Healthineers

- 10.14 Thermo Fisher Scientific

- 10.15 Trividia Health

Table of Contents

Chapter 11 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 12 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 13 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing application of biosensors in medical field

- 3.2.1.2 Rising prevalence of diabetes globally

- 3.2.1.3 High demand for portable biosensors in Asia Pacific and Europe

- 3.2.1.4 Increasing technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 High cost of product development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 14 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 15 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Wearable

- 5.3 Non-wearable

Chapter 16 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Electrochemical

- 6.3 Optical

- 6.4 Thermal

- 6.5 Piezoelectric

- 6.6 Other technologies

Chapter 17 Market Estimates and Forecast, By Applications, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Blood glucose testing

- 7.3 Cholesterol testing

- 7.4 Blood gas analysis

- 7.5 Pregnancy testing

- 7.6 Drug discovery

- 7.7 Infectious disease testing

- 7.8 Other applications

Chapter 18 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Point of care testing

- 8.3 Home healthcare diagnostics

- 8.4 Research laboratories

- 8.5 Other end users

Chapter 19 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Switzerland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

Chapter 20 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 ARKRAY

- 10.3 Bio-Rad Laboratories

- 10.4 Biosensors International Group

- 10.5 Dexcom

- 10.6 Danaher

- 10.7 F. Hoffmann-La Roche

- 10.8 Masimo

- 10.9 Nova Biomedical

- 10.10 Platinum Equity Advisors

- 10.11 PHC Holdings

- 10.12 Pinnacle Technology

- 10.13 Siemens Healthineers

- 10.14 Thermo Fisher Scientific

- 10.15 Trividia Health

SPR分子交互作用分析仪市场:依产品类型、技术、应用和最终用户划分-2026-2032年全球预测检测器市场:按技术、产品类型、部署模式和最终用户划分-2026-2032年全球预测艾灸设备市场依产品类型、技术、操作方式、应用、最终用户和销售管道,全球预测(2026-2032年)分子交互作用分析仪器市场:按技术、最终用户和应用划分,全球预测(2026-2032)

SPR分子交互作用分析仪市场:依产品类型、技术、应用和最终用户划分-2026-2032年全球预测检测器市场:按技术、产品类型、部署模式和最终用户划分-2026-2032年全球预测艾灸设备市场依产品类型、技术、操作方式、应用、最终用户和销售管道,全球预测(2026-2032年)分子交互作用分析仪器市场:按技术、最终用户和应用划分,全球预测(2026-2032) 2026年全球检测器及配件市场报告

2026年全球检测器及配件市场报告 智慧生物膜感测器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、材质、最终用户和功能划分生物感测器市场分析及预测(至2035年):按类型、产品类型、技术、组件、应用、材料类型、最终用户、功能、安装类型和模式划分2026年全球生物感测器市场报告

智慧生物膜感测器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、材质、最终用户和功能划分生物感测器市场分析及预测(至2035年):按类型、产品类型、技术、组件、应用、材料类型、最终用户、功能、安装类型和模式划分2026年全球生物感测器市场报告 即时检测生物感测器市场-全球产业规模、份额、趋势、机会、预测:按产品、平台、最终用户、地区和竞争对手划分,2021-2031年检测器及配件市场-全球产业规模、份额、趋势、机会及预测:按产品、应用、最终用途、地区及竞争对手划分,2021-2031年

即时检测生物感测器市场-全球产业规模、份额、趋势、机会、预测:按产品、平台、最终用户、地区和竞争对手划分,2021-2031年检测器及配件市场-全球产业规模、份额、趋势、机会及预测:按产品、应用、最终用途、地区及竞争对手划分,2021-2031年