|

市场调查报告书

商品编码

1750597

肺癌市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Lung Cancer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

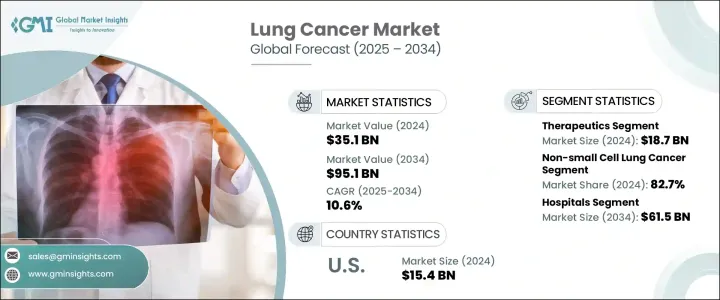

2024年,全球肺癌市场规模达351亿美元,预计2034年将以10.6%的复合年增长率成长,达到951亿美元。这主要得益于全球肺癌发生率的上升,以及各国政府为提高公众认知、促进早期发现和扩大治疗可及性而不断加大的力度。透过扩大援助计画和公共卫生计画来增加病患获得医疗服务的机会,也为市场扩张创造了更有利的环境。随着已开发国家老化人口的持续成长,高风险患者群体也不断扩大,尤其是在美国、德国和日本等国家。

公共机构和私人企业加大对肿瘤学的投入,引发了药物开发和诊断领域的创新浪潮,最终推动了市场的发展。持续的研究努力有助于发现治疗肺癌的先进方法,而生物标记驱动疗法的引入则促进了精准医疗的兴起。凭藉这些创新,医疗保健提供者可以提供更有效、更个人化的治疗方案,从而催生了对下一代诊断和治疗解决方案的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 351亿美元 |

| 预测值 | 951亿美元 |

| 复合年增长率 | 10.6% |

2024年,治疗领域收入达到187亿美元,因为患者和医护人员越来越青睐标靶治疗和免疫疗法,而非传统的化疗。这些新的治疗方案疗效较佳、副作用较少,并为患者带来更大的便利。此外,人们对联合疗法的兴趣也日益浓厚,即同时使用多种治疗策略,从而提高了治疗方案的有效性。先进的疗法如今常用于初始治疗阶段,这有助于重新定义各种肺癌类型的治疗标准。

预计医院癌症治疗市场将大幅成长,到2034年将达到615亿美元,这得益于支气管镜等先进诊断工具的广泛应用,这些工具已成为医院癌症检测的标准配置。随着这些工具越来越普及、效率越来越高,医院进行的诊断程序数量也将持续成长。医院对诊断设备和外科手术的支持性报销框架进一步鼓励患者到医院就诊,从而推动收入成长。

由于诊断技术的快速发展和监管机构的大力支持,美国肺癌市场在2024年的价值达到154亿美元。领先的生物製药公司和癌症研究机构的存在,加上联邦机构的大量资金投入,推动了临床开发和快速产品批准。这些因素为创新肺癌解决方案的采用创造了有利环境,进一步增强了北美市场的表现。

塑造全球肺癌市场格局的关键参与者包括默克、太阳製药、辉瑞、罗氏、百时美施贵宝、AdvaCare Pharma、克利夫兰诊所、威尔康奈尔医学院、罗格斯大学健康中心、Biodesix、纪念斯隆凯特琳癌症中心、梯瓦製药、CHEPLAPHARM 集团和匹兹堡大学医学中心。为了巩固市场地位,各公司优先投资精准肿瘤学研究、拓展全球分销网络,并与生技公司和学术机构建立策略合作。许多公司也正在加速临床试验管线的建设,以便更快推出创新疗法。此外,他们也正在收购拥有有前景的候选药物的小型公司,同时优化药物输送系统以改善患者治疗效果。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球肺癌发生率上升

- 诊断和筛检技术的进步

- 标靶疗法和免疫疗法的应用日益增多

- 微创手术需求不断成长

- 产业陷阱与挑战

- 治疗费用高昂

- 缺乏技术精湛、训练有素的肿瘤科医生和放射科医生

- 成长动力

- 成长潜力分析

- 监管格局

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 未来市场趋势

- 肺癌流行病学

- 报销场景

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按诊断和治疗,2021 年至 2034 年

- 主要趋势

- 诊断

- 支气管镜检查

- 分子检测

- 影像学

- 其他诊断

- 疗法

- 非侵入性治疗

- 按类型

- 化疗

- 标靶治疗

- 免疫疗法

- 其他非侵入性疗法

- 依给药途径

- 口服

- 肠外

- 按类型

- 微创治疗

- 射频消融

- 微波消融

- 热/冷冻消融

- 其他微创疗法

- 非侵入性治疗

第六章:市场估计与预测:按适应症,2021 年至 2034 年

- 主要趋势

- 非小细胞肺癌

- 小细胞肺癌

第七章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院

- 诊断实验室

- 专科诊所

- 其他最终用途

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- AdvaCare Pharma

- Biodesix

- Bristol-Myers Squibb Company

- CHEPLAPHARM Group

- Cleveland Clinic

- F. Hoffmann La Roche

- Memorial Sloan Kettering Cancer Center

- Merck & Co.

- Pfizer

- Rutgers Health Sun Pharmaceutical

- Sun Pharmaceuticals

- Teva Pharmaceuticals

- UPMC

- Weill Cornell Medicine

The Global Lung Cancer Market was valued at USD 35.1 billion in 2024 and is estimated to grow at a CAGR of 10.6% to reach USD 95.1 billion by 2034, driven by the rising incidence of lung cancer worldwide, as well as growing government efforts to improve awareness, promote early detection, and enhance access to treatment. Increasing patient access to care through expanding assistance programs and public health initiatives has also contributed to a more favorable environment for market expansion. As aging populations in developed countries continue to rise, so does the at-risk patient pool, particularly in nations like the United States, Germany, and Japan.

Greater investment in oncology by public institutions and private players has triggered a wave of innovation in drug development and diagnostics, ultimately pushing the market forward. Continuous research efforts are helping to uncover advanced methods of treating lung cancer, and the introduction of biomarker-driven therapies has supported the emergence of precision medicine. With these innovations, healthcare providers can offer more effective, customized treatment regimens, creating demand for next-generation diagnostic and therapeutic solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $35.1 Billion |

| Forecast Value | $95.1 Billion |

| CAGR | 10.6% |

The therapeutics segment generated USD 18.7 billion in 2024, as patients and healthcare professionals increasingly prefer targeted therapies and immunotherapies over conventional chemotherapy. These new treatment options offer better outcomes, fewer side effects, and greater patient convenience. There is also growing interest in combination approaches-using multiple therapeutic strategies simultaneously, which has enhanced the effectiveness of treatment protocols. Advanced therapies are now often used in initial treatment stages, which is helping to redefine standards of care across various lung cancer types.

The hospital segment is projected to grow significantly, reaching an estimated USD 61.5 billion by 2034, fueled by the widespread adoption of advanced diagnostic tools such as bronchoscopy and other cutting-edge technologies, which have become standard in hospital settings for cancer detection. As these tools become more accessible and efficient, the number of diagnostic procedures performed in hospitals continues to rise. Supportive reimbursement frameworks for diagnostic equipment and surgical treatments in hospitals further encourage patients to seek care in these facilities, driving revenue growth.

United States Lung Cancer Market was valued at USD 15.4 billion in 2024, supported by rapid advancements in diagnostic technologies and strong support from regulatory authorities. The presence of leading biopharmaceutical companies and cancer research institutions, coupled with extensive funding from federal agencies, has fueled clinical development and fast-tracked product approvals. These elements have created a favorable landscape for the adoption of innovative lung cancer solutions, further strengthening market performance across North America.

Key players shaping the Global Lung Cancer Market landscape include Merck, Sun Pharmaceuticals, Pfizer, F. Hoffmann-La Roche, Bristol-Myers Squibb Company, AdvaCare Pharma, Cleveland Clinic, Weill Cornell Medicine, Rutgers Health, Biodesix, Memorial Sloan Kettering Cancer Center, Teva Pharmaceuticals, CHEPLAPHARM Group, and UPMC. To strengthen their market presence, companies prioritize investing in precision oncology research, expanding global distribution networks, and forming strategic collaborations with biotech firms and academic institutions. Many are also accelerating their clinical trial pipelines to introduce innovative therapies faster. Additionally, they are acquiring smaller firms with promising drug candidates, while optimizing drug delivery systems to improve patient outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of lung cancer globally

- 3.2.1.2 Technology advancements in diagnostics and screening

- 3.2.1.3 Increasing adoption of targeted and immune therapies

- 3.2.1.4 Rising demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Dearth of well-skilled and trained oncologists and radiologists

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Future market trends

- 3.7 Lung cancer epidemiology

- 3.8 Reimbursement scenario

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Diagnostics and Therapeutics, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostics

- 5.2.1 Bronchoscopy

- 5.2.2 Molecular testing

- 5.2.3 Imaging

- 5.2.4 Other diagnostics

- 5.3 Therapeutics

- 5.3.1 Non-invasive therapy

- 5.3.1.1 By type

- 5.3.1.1.1 Chemotherapy

- 5.3.1.1.2 Targeted therapy

- 5.3.1.1.3 Immunotherapy

- 5.3.1.1.4 Other non-invasive therapies

- 5.3.1.2 By route of administration

- 5.3.1.2.1 Oral

- 5.3.1.2.2 Parenteral

- 5.3.1.1 By type

- 5.3.2 Minimally invasive therapy

- 5.3.2.1 Radiofrequency ablation

- 5.3.2.2 Microwave ablation

- 5.3.2.3 Thermal/cryoablation

- 5.3.2.4 Other minimally invasive therapies

- 5.3.1 Non-invasive therapy

Chapter 6 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Non-small cell lung cancer

- 6.3 Small cell lung cancer

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Diagnostic laboratories

- 7.4 Specialty clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AdvaCare Pharma

- 9.2 Biodesix

- 9.3 Bristol-Myers Squibb Company

- 9.4 CHEPLAPHARM Group

- 9.5 Cleveland Clinic

- 9.6 F. Hoffmann La Roche

- 9.7 Memorial Sloan Kettering Cancer Center

- 9.8 Merck & Co.

- 9.9 Pfizer

- 9.10 Rutgers Health Sun Pharmaceutical

- 9.11 Sun Pharmaceuticals

- 9.12 Teva Pharmaceuticals

- 9.13 UPMC

- 9.14 Weill Cornell Medicine

肺癌免疫疗法查核点抑制剂市场:2026-2032年全球市场预测(按癌症类型、通路、治疗方法、作用机制、治疗阶段和最终用户划分)

肺癌免疫疗法查核点抑制剂市场:2026-2032年全球市场预测(按癌症类型、通路、治疗方法、作用机制、治疗阶段和最终用户划分) 肺癌治疗:全球市场肺癌基因组检测市场:依技术、检测类型、应用和最终用户划分-2026-2032年全球市场预测

肺癌治疗:全球市场肺癌基因组检测市场:依技术、检测类型、应用和最终用户划分-2026-2032年全球市场预测 表皮生长因子受体非小细胞肺癌市场-全球产业规模、份额、趋势、机会、预测:按药物类型、通路、地区和竞争格局划分,2021-2031年肺癌基因组检测市场-全球产业规模、份额、趋势、机会和预测,按组件、技术、检测板类型、样本类型、最终用户、地区和竞争格局划分,2021-2031年预测

表皮生长因子受体非小细胞肺癌市场-全球产业规模、份额、趋势、机会、预测:按药物类型、通路、地区和竞争格局划分,2021-2031年肺癌基因组检测市场-全球产业规模、份额、趋势、机会和预测,按组件、技术、检测板类型、样本类型、最终用户、地区和竞争格局划分,2021-2031年预测 肺癌药物市场规模、份额和成长分析(治疗方法、癌症类型、分子类型、通路和地区划分)—2026-2033年产业预测肺癌基因组检测药物市场-全球产业规模、份额、趋势、机会和预测,按技术、样本类型、检测组类型、最终用户、地区和竞争格局划分,2020-2030年预测

肺癌药物市场规模、份额和成长分析(治疗方法、癌症类型、分子类型、通路和地区划分)—2026-2033年产业预测肺癌基因组检测药物市场-全球产业规模、份额、趋势、机会和预测,按技术、样本类型、检测组类型、最终用户、地区和竞争格局划分,2020-2030年预测 肺癌抗体药物复合体的全球市场:市场机会,专利,价格,临床试验相关洞察(2030年)

肺癌抗体药物复合体的全球市场:市场机会,专利,价格,临床试验相关洞察(2030年) 肺癌市场按类型、药物类别、分子类型、给药途径、疾病分期、年龄层、性别、分销管道、最终用户和地区划分肺癌治疗市场-全球产业规模、份额、趋势、机会和预测,按癌细胞类型(非小细胞肺癌、小细胞肺癌)、按治疗方法、按地区和竞争细分,2020 年至 2030 年

肺癌市场按类型、药物类别、分子类型、给药途径、疾病分期、年龄层、性别、分销管道、最终用户和地区划分肺癌治疗市场-全球产业规模、份额、趋势、机会和预测,按癌细胞类型(非小细胞肺癌、小细胞肺癌)、按治疗方法、按地区和竞争细分,2020 年至 2030 年