|

市场调查报告书

商品编码

1750608

木质地板市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Wooden Decking Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

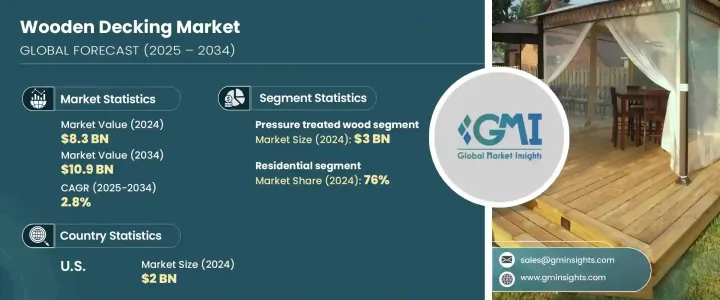

2024年,全球木质装饰市场价值达83亿美元,预计到2034年将以2.8%的复合年增长率成长,达到109亿美元。这得益于户外生活区需求的不断增长,以及已开发经济体和新兴经济体建筑活动的蓬勃发展。业主和开发商对提升房产价值和提升户外美观度表现出浓厚的兴趣,这推动了对高品质装饰解决方案的需求。市场也受到向可持续材料转变的日益增长的影响。注重环保的消费者寻求环保替代品,包括来自负责任管理的森林的木材以及由回收部件製成的高级复合装饰材料。这些替代品的维护需求较低,并且更能抵御恶劣天气条件。

对永续建筑实践的日益关注是推动该市场变革的重要催化剂。木材处理技术和复合材料製造领域的创新显着提高了露台地板解决方案的耐用性和使用寿命。现今的产品经过精心设计,能够抵御腐烂、虫害和环境磨损,是现代户外应用的理想选择。复合露台地板因其兼具木材的美观性和增强的弹性,并减少了维护需求而备受青睐。这种转变使复合材料成为追求长期性能和最小环境足迹的消费者的首选。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 83亿美元 |

| 预测值 | 109亿美元 |

| 复合年增长率 | 2.8% |

2024年,压力处理木材占据了最大的市场份额,贡献了30亿美元的市场规模,这得益于其价格实惠、易于获取以及优异的防潮、防腐和防虫性能。由于处理方法的不断改进,压力处理木材强度更高、使用寿命更长,因此仍然是露台专案的首选材料。儘管出现了更多现代化的替代品,但其实实用优势使其在商业和住宅应用中仍然广受欢迎。

住宅领域在2024年占据76%的市场份额,占据主导地位,预计到2034年将维持3%的复合年增长率。随着越来越多的房主注重居住环境中的健康和放鬆,户外空间变得至关重要。木质露台有助于实现这一转变,它提供了一种优雅、环保的解决方案,符合当代设计偏好。市场对经过认证的可持续木材和复合材料的采用率不断上升,尤其是那些经认证对环境影响较小的木材和复合材料,这进一步支持了绿色家居运动。

2024年,美国木质露台市场占了20%的市场。凭藉强大的房屋所有权文化和对户外休閒空间的重视,美国继续推动市场发展。越来越多的建筑商在新建住宅和翻新项目中采用木质露台,而红木和经过处理的木材等材料因其耐用性和与当地气候的兼容性而备受青睐。

James Latham、Fiberon、Kebony、AZEK Building Products、Trex Company、UPM、Alfresco Floors、Inovar Floors、West Fraser 和 DuraLife 等领先公司正在采用多种策略来提升其市场地位。他们大力投资研发,以打造更耐用、更环保的地板产品,并采用绿色认证标准来吸引註重永续发展的消费者。他们与大型零售商合作,并进行数位行销活动,以提升品牌知名度。一些公司将生产营运本地化,以降低成本并缩短交付时间。客製化服务和先进的表面技术是满足不断变化的客户偏好和竞争态势的关键差异化因素。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素。

- 利润率分析。

- 中断

- 未来展望

- 製成品

- 经销商

- 川普政府关税的影响

- 贸易影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(客户成本)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 贸易影响

- 供应商格局

- 重要新闻和倡议

- 监管格局

- 价格趋势分析

- 衝击力

- 成长动力

- 建筑业的成长

- 户外生活空间日益流行

- 转向可持续和可生物降解的建筑材料

- 住宅部门的成长

- 产业陷阱与挑战

- 替代品的可用性

- 与森林砍伐有关的担忧

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依木材类型,2021 - 2034 年

- 主要趋势

- 经过压力处理的木材

- 红木

- 雪松

- 热带硬木

- 木塑复合材料

- 其他(红木、柚木、虎木等)

第六章:市场估计与预测:按安装量,2021 - 2034 年

- 主要趋势

- 室内的

- 户外的

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 栏桿

- 地面

- 墙

- 其他的

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 住宅

- 新建筑

- 重塑

- 商业的

- 新建筑

- 重塑

第九章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 直销

- 间接销售

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第 11 章:公司简介

- Alfresco Floors

- AZEK Building Products

- DuraLife

- Fiberon

- Humboldt Redwood Company

- Inovar Floors

- James Latham

- Kebony

- Metsa Group

- Trex Company

- United Construction Products

- Universal Forest Products

- UPM

- West Fraser

- Weyerhaeuser Company

The Global Wooden Decking Market was valued at USD 8.3 billion in 2024 and is estimated to grow at a CAGR of 2.8% to reach USD 10.9 billion by 2034, fueled by increasing demand for outdoor living areas, combined with a rise in construction activity across both developed and emerging economies. Homeowners and developers are showing strong interest in enhancing property value and outdoor aesthetics, which is pushing demand for high-quality decking solutions. The market is also being shaped by a growing shift toward sustainable materials. Eco-conscious consumers look for environmentally friendly alternatives, including wood sourced from responsibly managed forests and advanced composite decking materials made from recycled components. These alternatives offer lower maintenance needs and better resistance to harsh weather conditions.

The increasing focus on sustainable building practices is a major catalyst for change in this market. Innovations in wood treatment technology and composite material manufacturing have significantly improved the durability and lifespan of decking solutions. Products today are engineered to resist decay, pests, and environmental wear, making them ideal for modern outdoor applications. Composite decking has gained traction for combining wood aesthetics with enhanced resilience, reducing the need for upkeep. This shift has positioned composite materials as a preferred choice among consumers aiming for long-term performance with a minimal environmental footprint.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $10.9 Billion |

| CAGR | 2.8% |

In 2024, pressure-treated wood held the largest market share, contributing USD 3 billion due to its affordability, accessibility, and high resistance to moisture, rot, and insects. Pressure-treated wood remains a preferred option in decking projects thanks to its improved strength and extended lifespan, enabled by continuous technological improvements in treatment methods. Despite the emergence of more modern alternatives, its practical advantages have helped it retain popularity in commercial and residential applications.

The residential sector dominated the market with a 76% share in 2024 and is projected to maintain steady growth at a 3% CAGR through 2034. As more homeowners focus on wellness and relaxation within their living environments, outdoor spaces have become essential. Wooden decking helps in this transformation by offering an elegant, eco-conscious solution that aligns with contemporary design preferences. The market has seen increased adoption of certified sustainable wood and composites, particularly those verified for low environmental impact, further supporting the green home movement.

United States Wooden Decking Market held a 20% share in 2024. With a strong culture of homeownership and appreciation for outdoor recreational space, the U.S. continues to drive market momentum. Builders are increasingly incorporating wooden decks in new housing and renovation projects, with materials like redwood and treated lumber being favored for their durability and compatibility with regional climates.

Leading companies such as James Latham, Fiberon, Kebony, AZEK Building Products, Trex Company, UPM, Alfresco Floors, Inovar Floors, West Fraser, and DuraLife are using several strategies to enhance their market standing. They are heavily investing in R&D to create longer-lasting, eco-friendly decking options and adopting green certification standards to appeal to sustainability-driven consumers. Partnerships with large retailers and digital marketing campaigns are employed to expand brand visibility. Some firms localize manufacturing operations to reduce costs and improve delivery timelines. Customization offerings and advanced surface technologies are key differentiators to meet evolving customer preferences and competitive dynamics.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Trade impact

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (cost to customers)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook & future considerations

- 3.2.1 Trade impact

- 3.3 Supplier landscape

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Pricing trend analysis

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increase in the construction industry

- 3.7.1.2 Growing trend of outdoor living spaces

- 3.7.1.3 Shift towards sustainable and biodegradable building materials

- 3.7.1.4 Increase in the residential sector

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Availability of substitutes

- 3.7.2.2 Concerns related to deforestation

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Wood Type, 2021 - 2034 (USD Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Pressure treated wood

- 5.3 Redwood

- 5.4 Cedar

- 5.5 Tropical hardwood

- 5.6 Wood-plastic composites

- 5.7 Others (Mahagony, teak, tigerwood, etc.)

Chapter 6 Market Estimates & Forecast, By Installation, 2021 - 2034 (USD Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Indoor

- 6.3 Outdoor

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Railing

- 7.3 Floor

- 7.4 Wall

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.2.1 New construction

- 8.2.2 Remodeling

- 8.3 Commercial

- 8.3.1 New construction

- 8.3.2 Remodeling

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Alfresco Floors

- 11.2 AZEK Building Products

- 11.3 DuraLife

- 11.4 Fiberon

- 11.5 Humboldt Redwood Company

- 11.6 Inovar Floors

- 11.7 James Latham

- 11.8 Kebony

- 11.9 Metsa Group

- 11.10 Trex Company

- 11.11 United Construction Products

- 11.12 Universal Forest Products

- 11.13 UPM

- 11.14 West Fraser

- 11.15 Weyerhaeuser Company

2026年全球木质甲板市场报告

2026年全球木质甲板市场报告 木质甲板市场 - 全球产业规模、份额、趋势、机会及预测(按类型、施工类型、应用、最终用户产业、地区和竞争格局划分,2021-2031年)

木质甲板市场 - 全球产业规模、份额、趋势、机会及预测(按类型、施工类型、应用、最终用户产业、地区和竞争格局划分,2021-2031年) 木质甲板市场按类型、应用、最终用户和地区划分

木质甲板市场按类型、应用、最终用户和地区划分 木质甲板市场规模、份额和成长分析(按类型、应用、施工类型、最终用途和地区划分)—2026-2033年产业预测

木质甲板市场规模、份额和成长分析(按类型、应用、施工类型、最终用途和地区划分)—2026-2033年产业预测 全球木地板市场预测(2025-2030 年),按木材类型、结构、处理、应用、最终用户和分销管道划分

全球木地板市场预测(2025-2030 年),按木材类型、结构、处理、应用、最终用户和分销管道划分 2026 年至 2032 年木质装饰市场(按类型、应用、最终用户和地区划分)

2026 年至 2032 年木质装饰市场(按类型、应用、最终用户和地区划分) 木地板:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

木地板:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 木甲板市场报告:2030 年趋势、预测与竞争分析

木甲板市场报告:2030 年趋势、预测与竞争分析