|

市场调查报告书

商品编码

1755208

焊接耗材市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Welding Consumables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

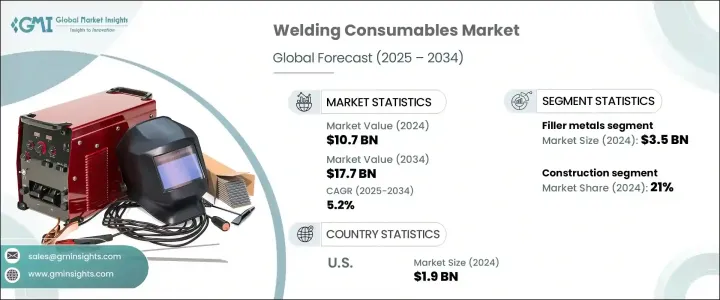

2024年,全球焊接耗材市场规模达107亿美元,预计到2034年将以5.2%的复合年增长率成长,达到177亿美元。这一增长主要源于基础设施和建筑项目对焊接耗材的需求不断增长,以及工业应用中自动化和机器人技术的日益普及。此外,新兴市场对环保焊接材料的日益青睐以及汽车产业的扩张也进一步促进了市场成长。在发展中国家,城镇化和可支配收入的提高预计将带来基础设施的大量投资,进而刺激对焊接耗材的需求。

随着这些地区工业的持续繁荣,焊接需求也将持续成长,为市场创造新的机会。焊接技术的进步,例如更坚固耐用材料的开发,也正在支撑市场的成长。随着製造商对客製化产品的需求不断增加,汽车产业(尤其是在已开发经济体和新兴经济体)对焊接製程的应用正在不断增加。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 107亿美元 |

| 预测值 | 177亿美元 |

| 复合年增长率 | 5.2% |

2024年,填充金属占据了最大的市场份额,产值达35亿美元,预计2025年至2034年期间的复合年增长率将达到5.6%。随着製造商不断推出创新产品以满足管道安装、重型机械生产和海上製造等行业不断变化的需求,对填充金属的需求也在不断增长。这些行业越来越多地转向使用强度更高的材料来提高产品的耐用性和性能。

建筑业在2024年占21%的份额,预计2025年至2034年的复合年增长率将达到5.9%。焊接是建筑业必不可少的工艺,尤其是在结构金属框架的製造中。随着大型建筑项目的推进和金属用量的增加,焊接在确保建筑物和基础设施的结构完整性方面发挥着至关重要的作用。该行业对焊接材料的需求与整个建筑行业的发展密切相关,焊接在预製和现场组装工作中都发挥着重要作用。

美国焊接耗材市场占77%的市场份额,2024年价值达19亿美元。基础设施建设的蓬勃发展,加上机器人技术和自动化在製造业的广泛应用,正在推动该市场的成长。除了机器人技术外,协作焊接机器人(cobot)也越来越多地应用于製造工厂,以协助人工焊工,从而提高焊接过程的效率和精度。环保耗材的需求以及汽车产业在新兴地区的扩张也促进了美国市场的成长。

全球焊接耗材市场的主要参与者包括林肯电气、松下、伊萨、D&H Secheron、米勒电气、神户製钢、现代焊接、Ador Welding、霍巴特焊接产品、Berkenhoff、EWM、Welding Alloys、Diffusion Engineers、Hilco Welding 和 Nouveaux。为了巩固其在焊接耗材市场的地位,各公司正专注于其产品的技术进步,例如开发具有增强机械和化学性能的新型填充金属。他们也强调环保解决方案,以满足製造业对永续实践日益增长的需求。此外,製造商正在大力投资研发,以开发满足日益增长的客製化解决方案需求的产品,尤其是在汽车和建筑行业。扩大在新兴市场的影响力并专注于自动化和机器人技术也是关键策略,使公司能够提高生产效率并降低劳动力成本。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素。

- 利润率分析。

- 中断

- 未来展望

- 製成品

- 经销商

- 供应商格局

- 重要新闻和倡议

- 监管格局

- 价格趋势分析

- 衝击力

- 成长动力

- 基础设施和建筑项目激增

- 汽车和製造业的成长

- 产业陷阱与挑战

- 原物料价格波动

- 地缘政治与贸易壁垒

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 电极

- 焊条电弧焊

- 气体保护金属电弧焊电极

- 其他的

- 助焊剂

- 埋弧焊剂

- 氧气燃料焊剂

- 其他(焊焊剂等)

- 气体

- 保护气体

- 支持气体

- 其他的

- 填充金属

- 实心线

- 药芯焊丝

- 金属芯线

- 焊条

- 其他(特种填充金属等)

- 其他的

第六章:市场估计与预测:按材料类型,2021 - 2034 年

- 主要趋势

- 低碳钢

- 不銹钢

- 铝

- 镍合金

- 铜合金

- 其他(钴合金等)

第七章:市场估计与预测:按最终用途产业,2021 - 2034 年

- 主要趋势

- 建造

- 汽车

- 活力

- 造船

- 航太

- 重型工程

- 其他(国防等)

第八章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 直销

- 间接销售

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第十章:公司简介

- Ador Welding

- Berkenhoff

- D&H Secheron

- Diffusion Engineers

- ESAB

- EWM

- Hilco Welding

- Hobart Welding Products

- Hyundai Welding

- Kobe Steel

- Lincoln Electric

- Miller Electric

- Nouveaux

- Panasonic

- Welding Alloys

The Global Welding Consumables Market was valued at USD 10.7 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 17.7 billion by 2034. This growth is driven by the increasing demand for welding consumables in infrastructure and construction projects with the rising adoption of automation and robotics in industrial applications. Additionally, the growing preference for eco-friendly welding materials and the expansion of the automotive sector in emerging markets are further contributing to market growth. In developing nations, urbanization and rising disposable incomes are expected to lead to significant investments in infrastructure, which in turn will fuel the demand for welding consumables.

As the industrial sector in these regions continues to thrive, the need for welding will grow, creating new opportunities in the market. Advances in welding technology, such as the development of stronger, more durable materials, are also supporting market growth. The automotive sector, particularly in both developed and emerging economies, is seeing a rise in the application of welding processes as manufacturers demand more custom-made products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.7 Billion |

| Forecast Value | $17.7 Billion |

| CAGR | 5.2% |

Filler metals held the largest market share in 2024, generating USD 3.5 billion, and is expected to grow at a CAGR of 5.6% between 2025 and 2034. The demand for filler metals is rising as manufacturers introduce innovative products to meet the evolving needs of industries like pipeline installation, heavy machinery production, and offshore fabrication. These industries are increasingly turning to higher-strength materials to improve the durability and performance of their products.

The construction segment held a 21% share in 2024 and is expected to grow at a CAGR of 5.9% from 2025 to 2034. Welding is an essential process in construction, especially in the fabrication of structural metal frameworks. With large-scale construction projects and increasing metal usage, welding plays a critical role in ensuring the structural integrity of buildings and infrastructure. The demand for welding consumables in this sector is closely tied to the growth of the overall construction industry, with welding playing a significant role in both prefabricated and on-site assembly work.

United States Welding Consumables Market held a 77% share and was valued at USD 1.9 billion in 2024. The surge in infrastructure development, coupled with the adoption of robotics and automation in manufacturing, is propelling the growth of this market. In addition to robotics, collaborative welding robots (cobots) are increasingly being used in manufacturing facilities to assist human welders, making welding processes more efficient and precise. The demand for eco-friendly consumables and the automotive sector's expansion in emerging regions are also contributing to market growth in the U.S.

Key players operating in the Global Welding Consumables Market include Lincoln Electric, Panasonic, ESAB, D&H Secheron, Miller Electric, Kobe Steel, Hyundai Welding, Ador Welding, Hobart Welding Products, Berkenhoff, EWM, Welding Alloys, Diffusion Engineers, Hilco Welding, and Nouveaux. To strengthen their position in the welding consumables market, companies are focusing on technological advancements in their product offerings, such as the development of new filler metals with enhanced mechanical and chemical properties. They are also emphasizing eco-friendly solutions to cater to the growing demand for sustainable practices in manufacturing. Additionally, manufacturers are investing heavily in R&D to develop products that meet the increasing need for customized solutions, especially in the automotive and construction sectors. Expanding their presence in emerging markets and focusing on automation and robotics are also key strategies, enabling companies to improve production efficiency while reducing labor costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Pricing trend analysis

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Surge in infrastructure and construction projects

- 3.6.1.2 Growth in automotive and manufacturing sectors

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Fluctuating raw material prices

- 3.6.2.2 Geopolitical and trade barriers

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Billion, Million Units)

- 5.1 Key trends

- 5.2 Electrodes

- 5.2.1 Shielded metal arc welding electrodes

- 5.2.2 Gas metal arc welding electrodes

- 5.2.3 Others

- 5.3 Fluxes

- 5.3.1 Submerged arc welding flux

- 5.3.2 Oxy-fuel welding flux

- 5.3.3 Others (brazing flux etc.)

- 5.4 Gases

- 5.4.1 Shielding Gases

- 5.4.2 Backing Gases

- 5.4.3 Others

- 5.5 Filler metals

- 5.5.1 Solid wire

- 5.5.2 flux-cored wire

- 5.5.3 Metal cored wire

- 5.5.4 Welding rods

- 5.5.5 Others (specialty filler metals etc.)

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Material Type, 2021 - 2034 ($Billion, Million Units)

- 6.1 Key trends

- 6.2 Mild steel

- 6.3 Stainless steel

- 6.4 Aluminum

- 6.5 Nickel alloys

- 6.6 Copper alloys

- 6.7 Others (cobalt alloys etc.)

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Billion, Million Units)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Automobile

- 7.4 Energy

- 7.5 Shipbuilding

- 7.6 Aerospace

- 7.7 Heavy engineering

- 7.8 Others (defense etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Million Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Ador Welding

- 10.2 Berkenhoff

- 10.3 D&H Secheron

- 10.4 Diffusion Engineers

- 10.5 ESAB

- 10.6 EWM

- 10.7 Hilco Welding

- 10.8 Hobart Welding Products

- 10.9 Hyundai Welding

- 10.10 Kobe Steel

- 10.11 Lincoln Electric

- 10.12 Miller Electric

- 10.13 Nouveaux

- 10.14 Panasonic

- 10.15 Welding Alloys

2026年全球汽车数位焊接设备市场报告2026年全球焊接耗材市场报告2026年全球耐磨件市场报告

2026年全球汽车数位焊接设备市场报告2026年全球焊接耗材市场报告2026年全球耐磨件市场报告 焊接材料市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034)

焊接材料市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034) 新能源汽车焊接合金市场:按合金类型、焊接工艺、母材类型、形状、应用和最终用户划分,全球预测(2026-2032年)

新能源汽车焊接合金市场:按合金类型、焊接工艺、母材类型、形状、应用和最终用户划分,全球预测(2026-2032年) 日本焊接耗材市场规模、份额、趋势及预测(依产品类型、焊接技术、终端用户产业及地区划分,2026-2034年)

日本焊接耗材市场规模、份额、趋势及预测(依产品类型、焊接技术、终端用户产业及地区划分,2026-2034年) 镍合金焊接耗材市场规模、份额及成长分析(依产品类型、基体合金类型、焊接製程、最终用途产业及地区划分)-2026-2033年产业预测

镍合金焊接耗材市场规模、份额及成长分析(依产品类型、基体合金类型、焊接製程、最终用途产业及地区划分)-2026-2033年产业预测 焊接耗材市场规模、份额及成长分析(按类型、焊接技术、基材、应用及地区划分)-2026-2033年产业预测

焊接耗材市场规模、份额及成长分析(按类型、焊接技术、基材、应用及地区划分)-2026-2033年产业预测 焊接耗材:全球市占率及排名、总收入及需求预测(2025-2031年)焊接耗材市场按产品类型、焊接工艺、最终用户产业、材料类型、耗材形式和应用划分 - 全球预测 2025-2032

焊接耗材:全球市占率及排名、总收入及需求预测(2025-2031年)焊接耗材市场按产品类型、焊接工艺、最终用户产业、材料类型、耗材形式和应用划分 - 全球预测 2025-2032