|

市场调查报告书

商品编码

1755219

单模光纤市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Single-Mode Optical Fiber Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

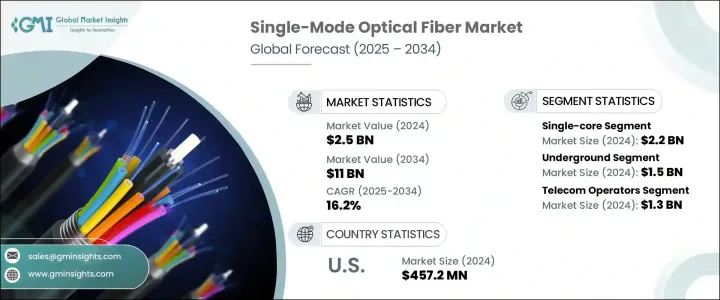

2024年,全球单模光纤市场规模达25亿美元,预计2034年将以16.2%的复合年增长率成长,达到110亿美元。 5G网路的全球部署以及云端运算和物联网扩张带来的资料流量激增,推动了这一急剧成长。随着网路基础设施对更快速度和更广覆盖范围的需求,电信业者纷纷转向单模光纤,因其能够在远距离传输资料的同时最大程度地降低讯号损耗。向下一代数位连接的转变正在推动各行各业的采用,其中,智慧城市、自治系统和超大规模资料中心等频宽密集型应用依赖可靠的高容量光纤网路。

过去,为了提升国内製造商的竞争力,推出了一系列贸易限制措施,例如对某些进口产品征收关税,但效果好坏参半。这些措施虽然支持了本土生产,但也扰乱了国际供应链,推高了光纤的进口成本。这导致光纤网路部署的延迟和不确定性。儘管如此,5G网路的快速部署仍然是全球单模光纤需求的主要驱动力,它能够实现基地台和资料中心之间更高速度和更低延迟的连接。该技术适用于长距离、大容量资料传输,使其成为扩展全球行动和固定宽频基础设施的关键。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 25亿美元 |

| 预测值 | 110亿美元 |

| 复合年增长率 | 16.2% |

单芯光纤市场在2024年创造了22亿美元的市场规模,成为主导类别。这一增长主要得益于其与全球现有电信基础设施的广泛兼容性。单芯单模光纤(SMF)凭藉其低色散和低衰减的特性,被广泛整合到长途和城域网路中。随着电信营运商不断推进升级,这些光纤无需更换原有系统即可实现高效能扩展。 FTTH的快速部署和5G连接的不断发展,进一步强化了单芯设计在跨区域向最终用户快速可靠地提供服务方面的作用。

2024年,地下部署市场规模达15亿美元。在人口密集的城市环境中,对隐蔽且受保护的基础设施的需求持续推动地下安装的趋势。城市发展和智慧城市计画正在鼓励电信业者采用地下电缆系统,以保持美观并防止外部损坏。这些部署也符合各国的国家宽频策略,要求建造具有高弹性、高容量且能抵御环境因素影响的基础设施。地下网路对于城域和城际资料传输日益重要,它为资料中心、企业园区和存取环网提供了可靠的效能。

美国单模光纤市场在2024年创收4.572亿美元,预计2034年将持续成长。全国范围内的5G部署需要更大的光纤回程容量,以支援低延迟和高速资料传输。联邦政府的资助计画为宽频扩张创造了强劲势头,推动了对先进长距离光纤网路的需求。超大规模资料中心基础设施的成长持续增加对连接各种设施的高频宽光纤连接的需求,从而进一步推动单模光纤在国内部署中的采用。

全球单模光纤市场的主要参与者包括康宁、康普、普睿司曼、LS Cable and System、长飞光纤光缆、住友电工、Humanetics、HTGD、Nike森、藤仓、Birla Furukawa 和古河马达。为了巩固更强大的市场地位,单模光纤公司将创新、成本效益和地理扩张放在首位。许多公司正在大力投资研发具有更低衰减和更高传输容量的光纤,使其成为 5G、FTTH 和超大规模资料网路等不断发展的应用的理想选择。与电信营运商和基础设施供应商的策略合作伙伴关係正在加快产品在各地区的采用速度。製造商也在优化生产流程并扩大新兴市场的设施覆盖范围,以缩短交货时间和降低物流成本。此外,材料采购多元化和增强供应链弹性已成为关键策略。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响

- 关键零件价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 产业衝击力

- 成长动力

- 来自云端服务和物联网的资料流量不断增加

- 5G网路全球部署

- FTTH(光纤到府)需求不断成长

- 智慧城市和基础设施项目

- 向工业自动化和工业4.0转变

- 产业陷阱与挑战

- 城市环境中的复杂安装

- 激烈的市场竞争与价格压力

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:依核心,2021 年至 2034 年

- 主要趋势

- 单核

- 双核心

- 多核心

第六章:市场估计与预测:依部署,2021 年至 2034 年

- 主要趋势

- 地下

- 水下

- 电线桿

第七章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 政府/国防

- 电信营运商

- 云端提供者

- 石油和天然气

- 工业自动化

- 其他的

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- AFL

- Birla Furukawa

- CommScope

- Corning Incorporated

- Exail

- Fujikura

- Furukawa

- HTGD

- Humanetics

- LS Cable & System

- Nexans

- Optical Cable Corporation

- Prysmian Group

- Sr. Indus Electro Systems Pvt. Ltd

- STL Tech

- Sumitomo Electric Industries, Ltd.

- Yangtze Optical Fiber & Cable

- ZTT

The Global Single-Mode Optical Fiber Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 16.2% to reach USD 11 billion by 2034. This sharp increase is being fueled by the global implementation of 5G networks and the explosion of data traffic driven by cloud computing and IoT expansion. As network infrastructure demands faster speeds and broader coverage, telecom providers are turning to single-mode fibers for their ability to transmit data over extended distances with minimal signal loss. The shift toward next-gen digital connectivity is propelling adoption across industries, where bandwidth-intensive applications like smart cities, autonomous systems, and hyperscale data centers rely on reliable high-capacity fiber networks.

Past trade restrictions, such as tariffs on certain imports, were introduced to improve competitiveness for domestic manufacturers but had mixed results. While they supported local production, they also disrupted international supply chains and pushed up the cost of importing optical fibers. This led to delays and uncertainty in fiber network deployments. Despite this, the rapid rollout of 5G networks remains the key driver of global demand for single-mode optical fiber, enabling higher speed and lower latency connectivity between base stations and data centers. The technology's suitability for long-distance, high-volume data transmission makes it essential for expanding mobile and fixed broadband infrastructure worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $11 Billion |

| CAGR | 16.2% |

The single-core segment generated USD 2.2 billion in 2024, making it the dominant category. This growth is primarily supported by its broad compatibility with existing global telecom infrastructure. Single-core SMFs are widely integrated into long-distance and metro networks because of their low dispersion and attenuation characteristics. As telecom providers push forward with upgrades, these fibers enable high-performance expansion without the need for replacing legacy systems. The fast pace of FTTH deployment and growing 5G connectivity further reinforce the role of single-core designs in enabling rapid and reliable service delivery to end users across regions.

The underground deployment segment generated USD 1.5 billion in 2024. The need for concealed and protected infrastructure in dense urban landscapes continues to drive the trend toward underground installation. Urban development and smart city initiatives are encouraging telecom operators to adopt underground cable systems to maintain aesthetics and safeguard against external damage. These deployments also align with national broadband strategies in various countries, calling for resilient and high-capacity infrastructure capable of withstanding environmental factors. Underground networks are increasingly essential for metro and intercity data transport, offering reliable performance for data centers, enterprise parks, and access rings.

U.S. Single-Mode Optical Fiber Market generated USD 457.2 million in 2024 and is projected to grow through 2034. National 5G deployments are demanding greater fiber backhaul capacity to support low latency and high-speed data transfers. Federal funding initiatives have created strong momentum in broadband expansion, driving demand for advanced long-distance optical fiber networks. Growth in hyperscale data center infrastructure continues to increase demand for high-bandwidth fiber connections linking various facilities, further boosting single-mode fiber adoption in domestic deployments.

Key industry players in the Global Single-Mode Optical Fiber Market include Corning, CommScope, Prysmian, LS Cable and System, Yangtze Optical Fiber and Cable, Sumitomo Electric, Humanetics, HTGD, Nexans, Fujikura, Birla Furukawa, and Furukawa. To secure a stronger market position, single-mode optical fiber companies are prioritizing innovation, cost efficiency, and geographic expansion. Many are heavily investing in R&D to develop fibers with lower attenuation and higher transmission capacity, making them ideal for evolving applications like 5G, FTTH, and hyperscale data networks. Strategic partnerships with telecom operators and infrastructure providers are enabling faster product adoption across regions. Manufacturers are also optimizing production processes and expanding facility footprints in emerging markets to reduce lead times and logistics costs. In addition, diversification of material sourcing and strengthening supply chain resilience have become crucial strategies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing data traffic from cloud services & IoT

- 3.3.1.2 Global rollout of 5G network

- 3.3.1.3 Growing demand for FTTH (fiber to the home)

- 3.3.1.4 Smart city and infrastructure projects

- 3.3.1.5 Shift towards industrial automation and industry 4.0

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Complex installation in urban environments

- 3.3.2.2 Intense market competition and price pressure

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Core, 2021 – 2034 (USD Million & Megameter)

- 5.1 Key trends

- 5.2 Single-core

- 5.3 Dual-core

- 5.4 Multi-core

Chapter 6 Market Estimates and Forecast, By Deployment, 2021 – 2034 (USD Million & Megameter)

- 6.1 Key trends

- 6.2 Underground

- 6.3 Underwater

- 6.4 Utility poles

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Million & Megameter)

- 7.1 Key trends

- 7.2 Government/defense

- 7.3 Telecom operators

- 7.4 Cloud providers

- 7.5 Oil & gas

- 7.6 Industrial automation

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Megameter)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AFL

- 9.2 Birla Furukawa

- 9.3 CommScope

- 9.4 Corning Incorporated

- 9.5 Exail

- 9.6 Fujikura

- 9.7 Furukawa

- 9.8 HTGD

- 9.9 Humanetics

- 9.10 LS Cable & System

- 9.11 Nexans

- 9.12 Optical Cable Corporation

- 9.13 Prysmian Group

- 9.14 Sr. Indus Electro Systems Pvt. Ltd

- 9.15 STL Tech

- 9.16 Sumitomo Electric Industries, Ltd.

- 9.17 Yangtze Optical Fiber & Cable

- 9.18 ZTT

光纤测试市场:按产品类型、光纤类型、应用、最终用户和测试方法 - 2025 年至 2032 年全球预测

光纤测试市场:按产品类型、光纤类型、应用、最终用户和测试方法 - 2025 年至 2032 年全球预测 2025年全球军用光纤感测器市场报告

2025年全球军用光纤感测器市场报告 光纤市场预测(至 2032 年):按光纤类型、电缆类型、传输模式、应用、最终用户和地区进行的全球分析光纤检测设备市场(按设备类型、光纤模式、形式、最终用户和分销管道)—2025-2030 年全球预测

光纤市场预测(至 2032 年):按光纤类型、电缆类型、传输模式、应用、最终用户和地区进行的全球分析光纤检测设备市场(按设备类型、光纤模式、形式、最终用户和分销管道)—2025-2030 年全球预测 全球中空芯光纤市场全球轻纤维市场航太与军用光纤市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、材料类型、设备、部署、最终用户

全球中空芯光纤市场全球轻纤维市场航太与军用光纤市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、材料类型、设备、部署、最终用户 2025年全球多芯光纤(MCF)市场全球光纤监控市场全球内视镜光纤市场

2025年全球多芯光纤(MCF)市场全球光纤监控市场全球内视镜光纤市场