|

市场调查报告书

商品编码

1755251

光学卫星市场机会、成长动力、产业趋势分析及2025-2034年预测Optical Satellite Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

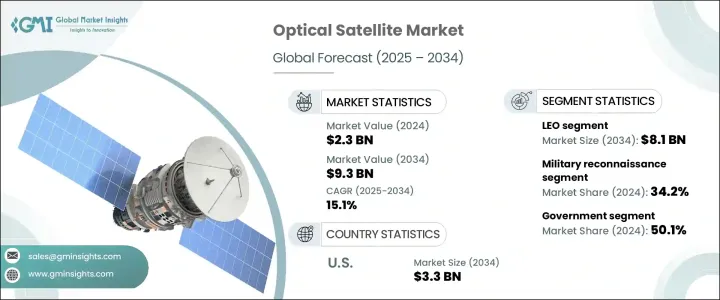

2024 年全球光学卫星市场规模为 23 亿美元,预计到 2034 年将以 15.1% 的复合年增长率增长,达到 93 亿美元,这得益于商业卫星服务需求的不断增长,尤其是对地球观测和监视应用的需求。随着光学卫星在轨道上越来越普遍,製造商面临与生产成本上升相关的新障碍。近期的关税政策给半导体、精密光学感测器和航空级材料等关键零件带来了成本压力,迫使许多製造商转向国内采购。这种转变导致资本支出增加和专案工期延长,给已经管理复杂卫星生产週期的公司带来了更大压力。此外,持续的供应链中断导致专案延误和预算超支,对持续产出构成挑战。

对高解析度地球观测 (EO) 影像日益增长的需求正在迅速改变卫星和航太工业的营运格局。如今,商业和公共部门都高度依赖高细节光学成像技术,用于环境监测、基础设施建设、灾害管理和农业分析等应用。精准农业尤其受益于这些能力,卫星透过多光谱成像提供有关土壤健康、作物生长和土地利用的可操作洞察。这些卫星能够实现近乎即时的资料传输,从而提高农业作业的准确性和效率,并进一步推动全球农业科技市场的采用。增强的成像能力加上可操作资料的快速週转时间,持续推动光学卫星部署的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 23亿美元 |

| 预测值 | 93亿美元 |

| 复合年增长率 | 15.1% |

到2034年,低地球轨道(LEO)市场规模预计将达到81亿美元。 LEO靠近地球,使其成为部署光学卫星的首选轨道,尤其适用于需要高解析度地面成像的任务。政府支持的措施与私营部门的能力相结合,以支持有针对性的卫星部署。这些合作收集了用于地形分析、气候建模和战略情报的详细图像,并增强了LEO市场对市场扩张的影响力。

随着精准农业诊断的重要性日益提升,预计2034年,作物监测应用的市场规模将达到23亿美元。光学卫星能够利用多光谱成像技术,在作物早期压力迹象的检测中发挥重要作用,从而防止产量损失。精准农业的发展,加上数位化农业的进步,持续推动对光电解决方案的需求,这些解决方案能够提供即时洞察,并帮助优化土地管理策略。

预计到2034年,英国光学卫星市场的复合年增长率将达到14.1%。英国政府持续投资地球观测技术,为卫星监测开闢了新的机会。英国对高品质成像解决方案的需求日益增长,这些解决方案可用于追踪环境变迁、增强监测系统,并为气候适应力和永续性相关政策提供资讯。

全球光学卫星市场的领导者包括洛克希德·马丁公司、空中巴士公司、泰雷兹·阿莱尼亚宇航公司和麦克萨科技公司。这些公司正在实施策略措施,以维持并扩大其市场地位。主要重点在于扩大卫星数量,并透过先进的光学技术提升影像解析度。他们投资与政府机构和私人航太公司的合作项目,以确保签订长期合约并共同开发下一代系统。大量的研发支出、零件的在地化采购以及精简製造流程的努力,正在帮助企业应对不断上涨的材料成本和生产挑战。此外,许多企业正在增强其软体平台,以支援更快的影像处理和分析集成,从而为最终用户创造更大的价值。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 价格波动

- 供应链重组

- 生产成本影响

- 需求面影响

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 成长动力

- 对高解析度地球观测资料的需求不断增长

- 增加对国家安全和监控的投资

- 商业卫星快速成长

- 影像和资料处理技术的进步

- 气候变迁监测和环境保护措施日益增多

- 产业陷阱与挑战

- 资本和营运成本高

- 资料过载和处理复杂性

- 对贸易的影响

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:依轨道类型,2021-2034

- 主要趋势

- 低地球轨道

- 中欧

- 地理

- 其他的

第六章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 军事侦察

- 作物监测

- 都市计画

- 灾害管理

- 矿物测绘

- 环境监测

- 其他的

第七章:市场估计与预测:依最终用途,2021-2034

- 主要趋势

- 政府

- 商业的

- 学术的

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- Airbus

- China Aerospace Science and Technology Corp.

- Elbit Systems

- Hanwha Group

- Israeli Aerospace Industry

- ISRO

- Lockheed Martin Corporation

- Maxar Technologies

- Mitsubishi Electric Corporation

- OHB SE

- Satellogic

- Surrey Satellite Technology Ltd

- Thales Alenia Space

- Turksat

The Global Optical Satellite Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 15.1% to reach USD 9.3 billion by 2034, driven by increasing demand for commercial satellite services, particularly for Earth observation and surveillance applications. As optical satellites become more prevalent in orbit, manufacturers are facing new hurdles tied to escalating production costs. Recent tariff policies have created cost pressures on critical components such as semiconductors, precision optical sensors, and aerospace-grade materials, forcing many manufacturers to pivot toward domestic sourcing. This shift has resulted in rising capital expenditure and extended project timelines, adding strain to companies already managing complex satellite production cycles. Additionally, persistent supply chain disruptions are causing delays and budget overruns, presenting a challenge for consistent output.

Heightened demand for high-resolution Earth Observation (EO) imagery is rapidly transforming the operational landscape of the satellite and space industry. Both commercial and public sectors now rely heavily on high-detail optical imaging for applications like environmental monitoring, infrastructure development, disaster management, and agricultural analysis. Precision farming has especially benefited from these capabilities, with satellites offering actionable insights on soil health, crop growth, and land use through multispectral imaging. These satellites allow for nearly real-time data delivery, improving the accuracy and efficiency of agricultural operations and further fueling adoption across global agritech markets. Enhanced imaging capabilities combined with quick turnaround times for actionable data continue to push the demand for optical satellite deployment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 15.1% |

The Low Earth Orbit (LEO) segment is poised to reach USD 8.1 billion by 2034. Its proximity to Earth makes LEO a preferred orbit for deploying optical satellites, especially for missions requiring high-resolution surface imaging. Government-backed initiatives integrated with private sector capabilities to support targeted satellite deployments. These collaborations gather detailed imagery for terrain analysis, climate modeling, and strategic intelligence, reinforcing the LEO segment's influence on market expansion.

The crop monitoring application is expected to hit USD 2.3 billion by 2034, backed by the rising importance of accurate agricultural diagnostics. Optical satellites are instrumental in detecting early signs of crop stress using multispectral imaging to prevent yield loss. The growth in precision agriculture, combined with advancements in digital farming, continues to boost demand for EO-enabled solutions that deliver real-time insights and help optimize land management strategies.

UK Optical Satellite Market is anticipated to grow at a CAGR of 14.1% through 2034. Ongoing investment in Earth observation technologies by the UK government has opened new opportunities for satellite-based monitoring. There's increasing national demand for high-quality imaging solutions used for tracking environmental changes, enhancing surveillance systems, and informing policies around climate resilience and sustainability.

Leading players in the Global Optical Satellite Market include Lockheed Martin Corporation, Airbus, Thales Alenia Space, and Maxar Technologies. These companies are implementing strategic measures to maintain and grow their market presence. A major focus lies in expanding satellite fleets and enhancing image resolution capabilities through advanced optics. They invest in collaborative programs with government agencies and private space firms to secure long-term contracts and co-develop next-generation systems. Significant R&D spending, localized sourcing of components, and efforts to streamline manufacturing are helping address rising material costs and production challenges. In addition, many players are enhancing their software platforms to support faster image processing and analytics integration delivering greater value to end-users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.3 Trump administration tariffs analysis

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.1.3 Impact on the industry

- 3.3.1.3.1 Supply-side impact (raw material)

- 3.3.1.3.1.1 Price volatility

- 3.3.1.3.1.2 Supply chain restructuring

- 3.3.1.3.1.3 Production cost implications

- 3.3.1.3.2 Demand-side impact

- 3.3.1.3.2.1 Price transmission to end markets

- 3.3.1.3.2.2 Market share dynamics

- 3.3.1.3.2.3 Consumer response patterns

- 3.3.1.3.1 Supply-side impact (raw material)

- 3.3.1.4 Key companies impacted

- 3.3.1.5 Strategic industry responses

- 3.3.1.5.1 Supply chain reconfiguration

- 3.3.1.5.2 Pricing and product strategies

- 3.3.1.5.3 Policy engagement

- 3.3.1.5.4 Outlook and future considerations

- 3.3.2 Growth drivers

- 3.3.2.1 Rising demand for high-resolution earth observation data

- 3.3.2.2 Increased investments in national security and surveillance

- 3.3.2.3 Rapid growth of commercial satellite

- 3.3.2.4 Technological advancements in imaging and data processing

- 3.3.2.5 Growing climate change monitoring and environmental protection initiatives

- 3.3.3 Industry pitfalls and challenges

- 3.3.3.1 High capital and operational costs

- 3.3.3.2 Data overload and processing complexity

- 3.3.1 Impact on trade

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Orbit Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 LEO

- 5.3 MEO

- 5.4 GEO

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Military reconnaissance

- 6.3 Crop monitoring

- 6.4 Urban planning

- 6.5 Disaster management

- 6.6 Mineral mapping

- 6.7 Environmental monitoring

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Government

- 7.3 Commercial

- 7.4 Academic

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Airbus

- 9.2 China Aerospace Science and Technology Corp.

- 9.3 Elbit Systems

- 9.4 Hanwha Group

- 9.5 Israeli Aerospace Industry

- 9.6 ISRO

- 9.7 Lockheed Martin Corporation

- 9.8 Maxar Technologies

- 9.9 Mitsubishi Electric Corporation

- 9.10 OHB SE

- 9.11 Satellogic

- 9.12 Surrey Satellite Technology Ltd

- 9.13 Thales Alenia Space

- 9.14 Turksat

2026年全球光卫星通讯市场报告

2026年全球光卫星通讯市场报告 光卫星通讯市场:依组件、平台、应用和最终用途划分-全球预测至2036年

光卫星通讯市场:依组件、平台、应用和最终用途划分-全球预测至2036年 全球光卫星通讯市场规模、份额、趋势和成长分析报告(2026-2034年)

全球光卫星通讯市场规模、份额、趋势和成长分析报告(2026-2034年) 全球光(雷射)卫星通讯市场(至2030年)以雷射类型(半导体二极体、光纤、固体)、资料速率(<2.5 Gbps、2.5-10 Gbps、>10 Gbps)、平台、应用、组件和地区划分

全球光(雷射)卫星通讯市场(至2030年)以雷射类型(半导体二极体、光纤、固体)、资料速率(<2.5 Gbps、2.5-10 Gbps、>10 Gbps)、平台、应用、组件和地区划分 光卫星通讯市场规模、份额和成长分析(按雷射类型、组件、传输介质、销售管道、应用和地区划分)-2026-2033年产业预测

光卫星通讯市场规模、份额和成长分析(按雷射类型、组件、传输介质、销售管道、应用和地区划分)-2026-2033年产业预测 全球光学卫星通讯市场

全球光学卫星通讯市场 光卫星通讯:终端厂商的策略

光卫星通讯:终端厂商的策略 光学卫星影像的全球市场:市场规模和占有率分析 - 趋势、驱动因素、竞争格局和预测(2024-2030 年)

光学卫星影像的全球市场:市场规模和占有率分析 - 趋势、驱动因素、竞争格局和预测(2024-2030 年)