|

市场调查报告书

商品编码

1755254

化学锚栓市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Chemical Anchors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

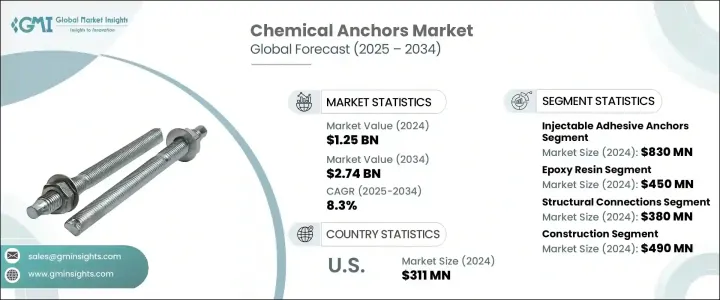

2024年,全球化学锚栓市场规模达12.5亿美元,预计到2034年将以8.3%的复合年增长率成长,达到27.4亿美元。这一增长主要源于全球建筑活动量的不断增长。随着城市人口的扩张和城市的快速发展,对先进建筑技术和现代化基础设施的需求持续增长。因此,化学锚栓正成为各种复杂程度和规模的建筑物中各种结构构件固定的必备组件。这些锚固解决方案在结构应用中提供强大且持久的黏结,并在住宅、商业和工业领域日益受到青睐。

随着都市化进程的加快,对能够在严苛环境下兼顾效能和安全性的锚固系统的需求日益增长。随着建筑结构日益复杂,以及对永续性的日益重视,工程师和承包商开始使用化学锚栓进行可靠的固定。它们能够有效地为混凝土和钢筋提供高强度的黏合力,因此在全球基础设施开发和改造专案中正日益被采用。化学锚栓能够承受动态和静态负荷,因此尤其适合现代建筑施工要求。目前,各公司正专注于生产符合严格安全标准的高效能锚定解决方案,以推动其在各种应用中的广泛应用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 12.5亿美元 |

| 预测值 | 27.4亿美元 |

| 复合年增长率 | 8.3% |

就产品类型而言,市场细分为注射式黏合剂锚固剂、胶囊黏合剂锚固剂和化学锚固固定件。注射式黏合剂锚固剂细分市场在2024年以8.3亿美元的估值引领市场,预计到2034年将以8.9%的复合年增长率成长。其主导地位归功于其易用性、在多种建筑应用中的多功能性以及在严苛工况下的卓越性能。这些锚固剂因其能够提供牢固、一致的黏合力而备受青睐,即使在需要精确承重性能和快速安装时间的区域也是如此。树脂配方技术的进步也促进了其日益普及,因为它可以实现更快的固化速度和更高的可靠性。

根据树脂类型,市场分为乙烯基酯树脂、环氧丙烯酸酯、环氧树脂、聚酯树脂和混合系统。环氧树脂细分市场在2024年的估值为4.5亿美元,预计在预测期内将以9%的复合年增长率扩张。环氧基化学锚栓因其高机械强度、优异的耐化学性以及在高负荷环境下的可靠黏合性,在重型建筑环境中广受青睐。这些树脂还具有快速固化能力,在极端环境条件下表现良好,使其成为结构完整性至关重要的专案的首选。

按应用分析,市场涵盖结构连接、钢筋连接、重型设备安装、外墙安装、扶手和安全护栏、抗震加固等。结构连结细分市场在2024年的价值达到3.8亿美元,预计2025年至2034年的复合年增长率为8.8%。该细分市场占据重要份额,因为它在确保各种建筑形式的稳定性和安全性方面发挥着至关重要的作用。随着高层建筑和现代基础设施系统的发展,对结构接头强力锚定解决方案的需求正在稳步增长。在这些应用中使用化学锚栓可以实现安全的负载传递,并将对周围材料的干扰降至最低。

建筑业在2024年成为最大的终端用途产业,价值4.9亿美元,预计复合年增长率为7.8%,市占率将达到39.5%。快速的城市发展趋势、商业房地产的扩张以及对安全和永续建筑实践的日益重视,都促进了该行业的突出地位。建筑商和开发商越来越依赖化学锚栓,因为它们具有适应性强、强度高且符合现代建筑要求的特性。随着设计复杂性和结构高度的不断提高,对可靠锚定解决方案的需求将持续高涨。

从区域表现来看,美国化学锚栓市场在2024年的估值为3.11亿美元,预计2034年将以8%的复合年增长率成长。基础设施升级的增加,加上抗震加强标准的日益普及,正在推动需求成长。此外,建筑法规的更新以及住宅和商业装修投资的增加也推动了市场成长。顶级製造商的技术改进和创新也扩大了化学锚栓的应用范围,为市场渗透提供了新的机会。

行业领导者透过持续创新、品牌建立和广泛的国际分销管道保持竞争优势。这些公司专注于生产先进的配方,提供卓越的承载能力、更快的固化时间以及在不同环境条件下的可靠性能。主要製造商注重永续性和符合全球安全标准,并根据不断变化的监管要求调整其产品线。此外,透过合作、合併和策略性收购进行扩张,使他们能够增强在新兴市场和成熟市场的影响力。专业的技术支援、先进的培训项目以及针对不同建筑需求的整合解决方案也塑造着该行业的发展。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)

(註:仅提供重点国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 注射式黏合剂锚

- 胶囊黏合剂锚

- 化学锚栓固定件

第六章:市场估计与预测:按树脂类型,2021 - 2034

- 主要趋势

- 环氧树脂

- 环氧丙烯酸酯

- 聚酯树脂

- 乙烯基酯树脂

- 混合系统

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 结构连接

- 钢筋连接

- 重型设备安装

- 外墙安装

- 扶手和安全护栏

- 抗震加固

- 其他的

第八章:市场估计与预测:按最终用途产业,2021 - 2034 年

- 主要趋势

- 建造

- 住宅

- 商业的

- 工业的

- 基础设施

- 公路和桥樑

- 水坝和隧道

- 铁路

- 其他的

- 製造业

- 海洋和近海

- 石油和天然气

- 矿业

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Hilti Corporation

- Sika AG

- Simpson Strong-Tie Company, Inc.

- Illinois Tool Works Inc. (ITW)

- BASF SE

- 3M Company

- Henkel AG & Co. KGaA

- Fischer Group

- Powers Fasteners (Stanley Black & Decker)

- MKT Fastening LLC

- DEWALT (Stanley Black & Decker)

- Mapei SpA

- Rawlplug

- EJOT Holding GmbH & Co. KG

- CELO Fixings

- Chemfix Products Ltd

- FIXDEX Fastening Technology

- Evonik Industries AG

- Good Use Hardware Co., Ltd.

- Ripple Construction Products Pvt Ltd.

The Global Chemical Anchors Market was valued at USD 1.25 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 2.74 billion by 2034. This growth is largely driven by the increasing volume of construction activity worldwide. As urban populations expand and cities develop rapidly, the demand for advanced construction techniques and modern infrastructure continues to rise. In response, chemical anchors are becoming essential components for securing various structural elements in buildings of varying complexity and size. These anchoring solutions provide strong, long-lasting bonds in structural applications and are gaining traction across residential, commercial, and industrial sectors.

As urbanization intensifies, there is a growing need for anchoring systems that ensure both performance and safety in demanding environments. With more complex structures being built and an increased focus on sustainability, engineers and contractors are turning to chemical anchors for reliable fastening. They are particularly effective in delivering high-strength adhesion to concrete and reinforcement bars, which is why they are being increasingly adopted in infrastructure development and renovation projects globally. Their ability to handle dynamic and static loads makes them especially suitable for modern-day construction requirements. Companies are now concentrating on manufacturing high-performance anchoring solutions that meet stringent safety standards, driving adoption across diverse applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.25 billion |

| Forecast Value | $2.74 billion |

| CAGR | 8.3% |

In terms of product types, the market is segmented into injectable adhesive anchors, capsule adhesive anchors, and chemical anchor fixings. The injectable adhesive anchors segment led the market in 2024 with a valuation of USD 830 million and is expected to grow at a CAGR of 8.9% through 2034. Its dominance is attributed to its ease of use, versatility across multiple construction applications, and superior performance in demanding scenarios. These anchors are favored for their ability to provide strong, consistent bonding, even in areas that require precise load-bearing performance and fast installation times. Technological advancements in resin formulations have also contributed to their rising popularity by enabling faster curing and improved reliability.

Based on resin types, the market is categorized into vinyl ester resin, epoxy acrylate, epoxy resin, polyester resin, and hybrid systems. The epoxy resin segment was valued at USD 450 million in 2024 and is anticipated to expand at a CAGR of 9% during the forecast period. Epoxy-based chemical anchors are widely preferred in heavy construction environments due to their high mechanical strength, excellent resistance to chemicals, and dependable bonding in high-load settings. These resins also offer rapid curing capabilities and perform well under extreme environmental conditions, making them the go-to option in projects where structural integrity is critical.

When analyzed by application, the market includes structural connections, rebar connections, heavy equipment mounting, facade installations, handrails and safety barriers, seismic retrofitting, and others. The structural connections segment recorded a value of USD 380 million in 2024 and is projected to grow at a CAGR of 8.8% from 2025 to 2034. This segment holds a significant share as it fulfills a crucial role in ensuring stability and safety across a broad range of construction formats. With the evolution of high-rise buildings and modern infrastructure systems, the demand for strong anchoring solutions in structural joints is growing steadily. The use of chemical anchors in these applications allows for secure load transfer and minimal disruption to surrounding materials.

The construction segment emerged as the largest end-use industry in 2024, valued at USD 490 million, and is forecasted to grow at a CAGR of 7.8%, capturing a market share of 39.5%. The growing trend of rapid urban development, expansion in commercial real estate, and increased focus on safe and sustainable construction practices have all contributed to the segment's prominence. Builders and developers increasingly rely on chemical anchors for their adaptability, strength, and compatibility with modern construction requirements. As design complexity and structural heights continue to rise, the need for reliable anchoring solutions will remain high.

In terms of regional performance, the United States chemical anchors market was valued at USD 311 million in 2024 and is anticipated to grow at a CAGR of 8% through 2034. The rise in infrastructure upgrades, coupled with the increasing adoption of seismic retrofitting standards, is fueling demand. Additionally, market growth is supported by updates in construction regulations and rising investments in residential and commercial renovations. Technological enhancements and innovations from top manufacturers are also expanding the application scope of chemical anchors, offering new opportunities for market penetration.

Leading industry players maintain a competitive edge through continuous innovation, brand development, and broad international distribution channels. These companies focus on producing advanced formulations that offer superior load-bearing capabilities, faster curing times, and reliable performance under varying environmental conditions. With an emphasis on sustainability and compliance with global safety standards, major manufacturers are aligning their product lines with evolving regulatory requirements. Moreover, expansion efforts through partnerships, mergers, and strategic acquisitions are enabling them to strengthen their presence across emerging and mature markets. The industry is also shaped by specialized technical support, advanced training programs, and integrated solutions tailored to diverse construction needs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Resin type

- 2.2.4 Application

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Injectable adhesive anchors

- 5.3 Capsule adhesive anchors

- 5.4 Chemical anchor fixings

Chapter 6 Market Estimates & Forecast, By Resin Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Epoxy resin

- 6.3 Epoxy acrylate

- 6.4 Polyester resin

- 6.5 Vinyl ester resin

- 6.6 Hybrid systems

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Structural connections

- 7.3 Rebar connections

- 7.4 Heavy equipment mounting

- 7.5 Facade installations

- 7.6 Handrails and safety barriers

- 7.7 Seismic retrofitting

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Construction

- 8.2.1 Residential

- 8.2.2 Commercial

- 8.2.3 Industrial

- 8.3 Infrastructure

- 8.3.1 Highways and bridges

- 8.3.2 Dams and tunnels

- 8.3.3 Railways

- 8.3.4 Others

- 8.4 Manufacturing

- 8.5 Marine and offshore

- 8.6 Oil & gas

- 8.7 Mining

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Hilti Corporation

- 10.2 Sika AG

- 10.3 Simpson Strong-Tie Company, Inc.

- 10.4 Illinois Tool Works Inc. (ITW)

- 10.5 BASF SE

- 10.6 3M Company

- 10.7 Henkel AG & Co. KGaA

- 10.8 Fischer Group

- 10.9 Powers Fasteners (Stanley Black & Decker)

- 10.10 MKT Fastening LLC

- 10.11 DEWALT (Stanley Black & Decker)

- 10.12 Mapei S.p.A.

- 10.13 Rawlplug

- 10.14 EJOT Holding GmbH & Co. KG

- 10.15 CELO Fixings

- 10.16 Chemfix Products Ltd

- 10.17 FIXDEX Fastening Technology

- 10.18 Evonik Industries AG

- 10.19 Good Use Hardware Co., Ltd.

- 10.20 Ripple Construction Products Pvt Ltd.

全球铁路锚固件市场(按产品类型、材料、安装类型、应用、最终用户和分销管道划分)预测(2026-2032年)黏结锚固市场按应用、树脂类型、最终用途产业、产品形式和分销管道划分,全球预测,2026-2032年

全球铁路锚固件市场(按产品类型、材料、安装类型、应用、最终用户和分销管道划分)预测(2026-2032年)黏结锚固市场按应用、树脂类型、最终用途产业、产品形式和分销管道划分,全球预测,2026-2032年 机械锚栓市场规模、份额和趋势分析报告:按材料、应用、地区和细分市场预测(2025-2033 年)

机械锚栓市场规模、份额和趋势分析报告:按材料、应用、地区和细分市场预测(2025-2033 年) 全球化学锚固市场概览及成长机会(2024-2031年)

全球化学锚固市场概览及成长机会(2024-2031年) 化学黏合剂锚栓:全球市场份额和排名、总收入和需求预测(2025-2031年)锚固设备市场按锚固类型、应用、最终用户、分销管道和材料类型-2025-2032年全球预测

化学黏合剂锚栓:全球市场份额和排名、总收入和需求预测(2025-2031年)锚固设备市场按锚固类型、应用、最终用户、分销管道和材料类型-2025-2032年全球预测 2025年锚定和固定件全球市场报告

2025年锚定和固定件全球市场报告 全球机械锚栓市场

全球机械锚栓市场 建筑锚固市场-全球产业规模、份额、趋势、机会和预测,按产品类型、材料、最终用途产业、地区和竞争细分,2020-2030 年预测全球建筑锚栓市场

建筑锚固市场-全球产业规模、份额、趋势、机会和预测,按产品类型、材料、最终用途产业、地区和竞争细分,2020-2030 年预测全球建筑锚栓市场