|

市场调查报告书

商品编码

1755307

燃料电池无人机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Fuel Cell UAV Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

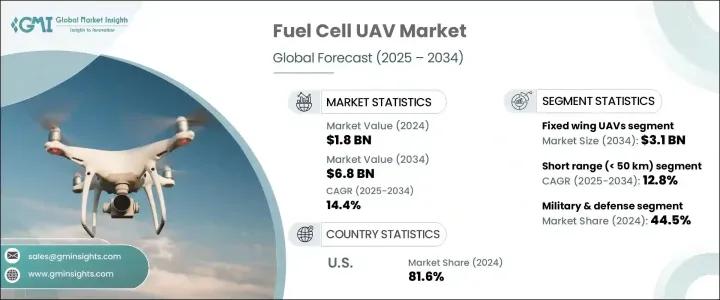

2024年,全球燃料电池无人机市场规模达18亿美元,预计2034年将以14.4%的复合年增长率成长,达到68亿美元。这得益于政府和机构对燃料电池技术的支持力度不断加大,以及对监视和侦察系统的需求不断增长。然而,美国政府的贸易政策(包括对中国进口产品加征关税)也给该市场带来了挑战,导致储氢系统、燃料电池堆和复合材料等关键零件的成本上升。这扰乱了全球供应链,影响了定价,并减缓了研发工作。

儘管如此,燃料电池无人机领域仍在持续显着成长,这得益于其众多优势。这些优势包括卓越的续航力、更低的噪音排放和更长的飞行时间,使其特别适合国防、环境监测和灾害应变等关键任务。燃料电池无人机能够长时间静音飞行且无需频繁加油,这正成为其区别于传统无人机的关键特征,使其成为监视、侦察和紧急行动的重要工具。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 18亿美元 |

| 预测值 | 68亿美元 |

| 复合年增长率 | 14.4% |

随着燃料电池无人机技术的进步,固定翼无人机预计将成为市场成长的主要贡献者,预计到2034年将达到31亿美元。这些无人机尤其适合执行长时间飞行任务,因为高气动效率和携带更大氢燃料电池系统的能力至关重要。它们能够在不影响燃油消耗的情况下保持较长的飞行时间,这使得它们在边境监视、环境监测和国防行动等需要覆盖广阔地理区域的应用中不可或缺。能够部署这些无人机执行更长的任务,将带来战略优势,尤其是在续航能力至关重要的行动中。

预计到2034年,短程燃料电池无人机市场的复合年增长率将达到12.8%。短程燃料电池无人机因其快速加油能力和比传统无人机更长的飞行时间而日益普及。这些无人机非常适合工业巡检、公共安全任务以及其他需要在狭窄作业区域内持续可靠运作的应用。随着技术的进步,这些无人机的用途更加广泛、效率更高,从而推动其在各行各业的应用。

预计到2034年,德国燃料电池无人机市场将以13.7%的复合年增长率成长,这得益于国家以脱碳和永续发展为重点的政策,以及欧盟支持的鼓励绿色技术创新的研究计画。德国致力于减少碳排放并推广永续航空解决方案,这推动了对氢动力无人机技术的投资。此外,国防承包商、航太公司和学术机构之间的合作,使德国成为绿色无人机技术的领导者,并使其成为先进无人机研发的中心。

全球燃料电池无人机产业的主要市场参与者包括 Hylium Industries、AeroVironment、FlightWave 航太、斗山创新、ISS Group、Aurora Flight Sciences、MMCUAV 和 Elbit Systems。为了巩固市场地位,燃料电池无人机领域的公司专注于开发尖端燃料电池技术,以提高无人机的效率和续航力。与政府和公私合作伙伴关係合作使他们能够获得资金和技术资源,从而降低开发成本。透过推动研发工作,这些公司正在推动创新并为氢动力无人机的普及做出贡献。他们也强调航太和国防领域的可持续解决方案,符合全球碳中和目标,确保其产品满足日益增长的环保技术需求。此外,与学术机构和国防承包商建立合作关係有助于他们始终站在绿色无人机革命的前沿。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 产业衝击力

- 成长动力

- 监视和侦察应用的需求不断增长

- 对清洁和永续推进技术的投资不断增加

- 在商业和工业应用的采用率不断提高

- 政府支持和军事现代化计划

- 政府和机构对燃料电池技术的支持不断增加

- 产业陷阱与挑战

- 燃料电池系统成本高

- 监管和空域限制

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- Pestel 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:依无人机类型,2021 - 2034 年

- 主要趋势

- 固定翼无人机

- 旋翼无人机

- 混合垂直起降无人机

第六章:市场估计与预测:依范围,2021 - 2034 年

- 主要趋势

- 短距离(<50公里)

- 中程(50-200公里)

- 长距离(>200公里)

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 军事与国防

- 商业和工业

- 配送和物流

- 空中监视和测绘

- 喷洒农药

- 环境监测

- 其他的

- 民事/政府

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- AeroVironment

- Aurora Flight Sciences

- Doosan Mobility Innovation

- Elbit Systems

- FlightWave Aerospace

- Hylium Industries

- ISS Group

- JOUAV

- MMCUAV

The Global Fuel Cell UAV Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 14.4% to reach USD 6.8 billion by 2034, driven by increasing government and institutional support for fuel cell technologies, as well as rising demand for surveillance and reconnaissance systems. However, the market faced challenges due to the U.S. administration's trade policies, including tariffs on Chinese imports, which led to higher costs for key components such as hydrogen storage systems, fuel cell stacks, and composite materials. This disrupted global supply chains, impacted pricing, and slowed research and development efforts.

Despite this, the fuel cell UAV sector continues to experience significant growth, driven by the numerous advantages these UAVs offer. These include superior endurance, reduced noise emissions, and extended flight durations, making them particularly suitable for critical operations, including defense, environmental monitoring, and disaster response. Their ability to operate silently for longer periods without needing frequent refueling is becoming a key feature that differentiates fuel cell UAVs from their traditional counterparts, positioning them as essential tools for surveillance, reconnaissance, and emergency operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 14.4% |

As fuel cell UAV technology advances, fixed-wing UAVs are anticipated to become a major contributor to market growth, projected to reach USD 3.1 billion by 2034. These UAVs are particularly favored for long-duration missions, where high aerodynamic efficiency and the capacity to carry larger hydrogen fuel cell systems are crucial. Their ability to maintain extended flight times without compromising on fuel consumption is making them indispensable in applications like border surveillance, environmental monitoring, and defense operations, where coverage over vast geographic areas is necessary. The ability to deploy these UAVs for longer missions provides strategic advantages, particularly in operations where endurance is critical.

The short-range fuel cell UAV segment is projected to grow at a CAGR of 12.8% through 2034, short-range fuel cell UAVs are gaining popularity due to their quick refueling capability and longer flight times compared to their traditional counterparts. These UAVs are ideal for industrial inspections, public safety tasks, and other applications that require sustained, reliable performance in confined operational areas. As technology improves, these UAVs become more versatile and efficient, driving their adoption in various industries.

Germany Fuel Cell UAV Market is expected to grow at a CAGR of 13.7% through 2034 fueled by national policies focused on decarbonization and sustainability, along with EU-backed research programs that encourage innovation in green technologies. Germany's commitment to reducing carbon emissions and promoting sustainable aviation solutions drives investments in hydrogen-powered UAV technologies. Furthermore, collaborations between defense contractors, aerospace companies, and academic institutions are positioning the country as a leader in green UAV technologies, making it a hub for advanced UAV research and development.

Key market players in the Global Fuel Cell UAV Industry include Hylium Industries, AeroVironment, FlightWave Aerospace, Doosan Mobility Innovation, ISS Group, Aurora Flight Sciences, MMCUAV, and Elbit Systems. To strengthen their market position, companies in the fuel cell UAV sector focus on developing cutting-edge fuel cell technology that enhances the efficiency and endurance of UAVs. Collaborating with governments and public-private partnerships allows them to access funding and technical resources, reducing development costs. By advancing R&D efforts, these companies are driving innovation and contributing to the adoption of hydrogen-powered UAVs. They also emphasize sustainable solutions in aerospace and defense, in line with global carbon neutrality goals, ensuring that their products meet the growing demand for eco-friendly technologies. Additionally, forging collaborations with academic institutions and defense contractors helps them remain at the forefront of the green UAV revolution.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growing demand for surveillance and reconnaissance applications

- 3.3.1.2 Rising investments in clean and sustainable propulsion technologies

- 3.3.1.3 Increasing adoption in commercial and industrial applications

- 3.3.1.4 Government support and military modernization programs

- 3.3.1.5 Rising government and institutional support for fuel cell technology

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost of fuel cell systems

- 3.3.2.2 Regulatory and airspace restrictions

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 Pestel analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By UAV Type, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Fixed wing UAVs

- 5.3 Rotary wing UAVs

- 5.4 Hybrid VTOL UAVs

Chapter 6 Market Estimates & Forecast, By Range, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Short range (< 50 km)

- 6.3 Medium range (50-200 km)

- 6.4 Long range (>200 km)

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Military & defense

- 7.3 Commercial & industrial

- 7.3.1 Delivery and logistics

- 7.3.2 Aerial surveillance and mapping

- 7.3.3 Pesticide spraying

- 7.3.4 Environmental monitoring

- 7.3.5 Others

- 7.4 Civil/government

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AeroVironment

- 9.2 Aurora Flight Sciences

- 9.3 Doosan Mobility Innovation

- 9.4 Elbit Systems

- 9.5 FlightWave Aerospace

- 9.6 Hylium Industries

- 9.7 ISS Group

- 9.8 JOUAV

- 9.9 MMCUAV

2026年全球氢能无人机集群动力市场报告

2026年全球氢能无人机集群动力市场报告 燃料电池无人机市场-全球产业规模、份额、趋势、机会、预测:按类型、最终用户、地区和竞争格局划分,2021-2031年

燃料电池无人机市场-全球产业规模、份额、趋势、机会、预测:按类型、最终用户、地区和竞争格局划分,2021-2031年 军用无人机燃料电池(2025-2029)

军用无人机燃料电池(2025-2029) 氢燃料电池无人机的全球市场:2030年为止的预测

氢燃料电池无人机的全球市场:2030年为止的预测