|

市场调查报告书

商品编码

1755352

脊椎植入物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Spinal Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

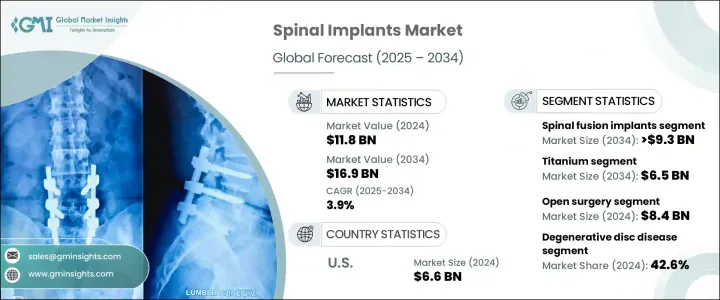

2024年,全球脊椎植入物市场规模达118亿美元,预计到2034年将以3.9%的复合年增长率成长,达到169亿美元。人口老化加剧、脊椎疾病发病率上升、微创手术的兴起以及植入材料和手术技术的进步,共同推动了市场需求的成长。随着椎管狭窄、退化性椎间盘疾病和椎间盘突出等脊椎疾病的发生率日益上升,尤其是在老年人群体中,对外科手术和脊椎稳定解决方案的需求也随之增长。

肥胖和久坐不动的生活方式进一步加剧了脊椎退化。因此,越来越多的患者选择手术矫正,尤其是在新的解决方案能够减轻疼痛、加速復原的情况下。机器人系统和导航工具在脊椎手术中的引入,不仅提高了手术精准度,还最大限度地降低了併发症发生率,从而鼓励了先进植入物的广泛应用。许多器械製造商正在积极应对这项挑战,设计出适用于微创技术的植入物,随着成本逐渐下降和可及性不断提高,这些植入物正在全球范围内被更广泛的临床应用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 118亿美元 |

| 预测值 | 169亿美元 |

| 复合年增长率 | 3.9% |

脊椎融合植入物市场预计将以4.3%的复合年增长率强劲成长,到2034年将达到93亿美元。这些器械的广泛应用源自于其在治疗因退化或创伤引起的脊椎不稳定方面的关键作用。随着脊椎滑脱和椎间盘疾病等退化性疾病的日益常见,脊椎融合手术的数量也持续增加。采用PEEK和钛等先进材料製成的新型融合植入物设计,因其与人体的兼容性、更高的强度以及与周围骨组织的更好结合,如今已得到更广泛的应用。这些特性能够改善患者的长期疗效,有助于巩固该领域在市场上的主导地位。

预计到2034年,钛基脊椎植入物市场将达到65亿美元的产值。钛因其高生物相容性、耐腐蚀性和结构耐久性,仍是脊椎外科手术的首选材料。它与人体无缝融合,最大限度地降低免疫排斥风险,同时在富含液体的环境中保持良好的弹性。钛植入物坚固而轻便,这对于患者在康復期间和康復后保持舒适度和良好的治疗效果至关重要。它们能够承受较大的机械负荷,使其成为颈椎和腰椎手术中椎间融合器、棒和板等应用的理想选择。其长期的安全记录进一步巩固了其在现代脊椎手术中的地位。

2024年,美国脊椎植入物市场规模达66亿美元,预计2025年至2034年期间的复合年增长率将达到3.5%。由于强生、史赛克、美敦力、捷迈邦美和NuVasive等主要製造商的鼎力支持,美国仍是脊椎植入物生产的全球领导者。这些公司走在创新的前沿,投资开发机器人技术和智慧植入物,以提高手术精准度和临床疗效。凭藉着遍布全国的广泛研发网路和製造设施,这些公司正在加速产品的部署和应用,增强美国在全球脊椎护理领域的影响力。

影响全球脊椎植入物市场的关键参与者包括 Spineart、Ulrich、Orthofix Holdings、B. Braun、CENTINEL SPINE、INTEGRA、Seaspine、RTI Surgical、Zimmer Biomet、Stryker、强生、Globus Medical、Alphatec Spine、美敦力和 NuVasive。为了扩大市场占有率,脊椎植入物产业的公司正专注于策略性研发投资,以增强植入物的功能及其与微创技术的兼容性。他们正积极透过合併、合作和收购进行全球扩张,以接触新的客户群并加强分销管道。将机器人技术和数位导航整合到他们的产品组合中,帮助他们提高手术准确性和患者满意度。该公司还与临床机构合作,以验证产品性能,获得更快的监管批准,并加强其在全球医疗保健提供者中的信誉。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 脊椎疾病盛行率上升

- 微创手术的需求不断增加

- 技术进步

- 已开发国家优惠的报销政策

- 产业陷阱与挑战

- 脊椎植入物和手术费用高昂

- 已开发国家的严格监管环境

- 市场机会

- 人工智慧和机器人技术在脊椎手术中的整合

- 日益关注门诊与流动医疗环境

- 成长动力

- 成长潜力分析

- 监管格局

- 我们

- 欧洲

- 技术格局

- 报销场景

- 波特的分析

- PESTEL分析

- 定价分析

- 差距分析

- 价值链分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 按地区

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 年至 2034 年

- 主要趋势

- 脊椎融合植入物

- 椎弓根螺钉

- 椎间融合装置(IBFD)

- 桿

- 盘子

- 笼子

- 其他脊椎融合植入物

- 动态稳定装置

- 人工椎间盘

- 子宫颈

- 腰椎

- 其他产品类型

第六章:市场估计与预测:按材料,2021 年至 2034 年

- 主要趋势

- 钛

- 钴铬合金

- 不銹钢

- 聚醚醚酮(PEEK)

- 其他材料

第七章:市场估计与预测:依手术类型,2021 年至 2034 年

- 主要趋势

- 开放性手术

- 微创手术

第 8 章:市场估计与预测:按适应症,2021 年至 2034 年

- 主要趋势

- 椎间盘退化性疾病

- 脊椎畸形

- 脊椎创伤

- 骨折

- 其他适应症

第九章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院

- 门诊手术中心

- 其他最终用途

第十章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Alphatec Spine

- B. Braun

- CENTINEL SPINE

- Globus Medical

- INTEGRA

- Johnson & Johnson

- Medtronic

- NuVasive

- Orthofix Holdings

- RTI Surgical

- Seaspine

- Spineart

- Stryker

- Ulrich

- Zimmer Biomet

The Global Spinal Implants Market was valued at USD 11.8 billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 16.9 billion by 2034. The growing demand is fueled by a rising aging population, an increase in spinal disorders, a shift toward minimally invasive procedures, and technological advancements in implant materials and surgical techniques. As spinal conditions like spinal stenosis, degenerative disc disease, and herniated discs become more prevalent, especially among older individuals, the need for surgical intervention and spinal stabilization solutions continues to climb.

Obesity and sedentary lifestyles further contribute to spinal degeneration. As a result, more patients are opting for surgical correction, especially with new solutions offering reduced pain and faster recovery. The introduction of robotic systems and navigation tools in spinal surgeries has not only enhanced procedural precision but also minimized complication rates, encouraging greater use of advanced implants. Many device manufacturers are responding by designing implants tailored for minimally invasive techniques, driving broader clinical adoption globally as costs gradually decline and accessibility improves.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.8 Billion |

| Forecast Value | $16.9 Billion |

| CAGR | 3.9% |

The spinal fusion implants segment is projected to witness strong growth at a CAGR of 4.3%, reaching USD 9.3 billion by 2034. The widespread use of these devices stems from their critical role in treating spinal instability caused by degeneration or trauma. As degenerative conditions such as spondylolisthesis and disc disorders become more common, the volume of spinal fusion procedures continues to grow. New fusion implant designs made from advanced materials such as PEEK and titanium are now more commonly used due to their compatibility with the human body, enhanced strength, and better integration with surrounding bone tissue. These properties increase long-term patient outcomes, helping to solidify the segment's dominance in the market.

Titanium-based spinal implants segment is expected to generate USD 6.5 billion by 2034. Titanium remains the preferred material in spinal surgeries due to its high biocompatibility, corrosion resistance, and structural durability. It integrates seamlessly with the body, minimizing the risk of immune rejection while maintaining resilience in fluid-rich environments. Titanium implants are strong yet lightweight, which is essential for patient comfort and performance during and after the recovery phase. They withstand significant mechanical loads, making them ideal for applications such as interbody cages, rods, and plates in both cervical and lumbar spine procedures. Their long-term safety record further reinforces their position in modern spinal procedures.

U.S. Spinal Implants Market was valued at USD 6.6 billion in 2024 and is expected to grow at a CAGR of 3.5% between 2025 and 2034. The U.S. remains a global leader in spinal implant production, supported by the presence of major manufacturers including Johnson & Johnson, Stryker, Medtronic, Zimmer Biomet, and NuVasive. These companies are at the forefront of innovation, investing in the development of robotics and smart implants that enhance surgical precision and clinical outcomes. With extensive R&D networks and manufacturing facilities across the country, these firms accelerate product deployment and adoption, strengthening the country's influence in the global spinal care landscape.

Key players shaping the Global Spinal Implants Market include Spineart, Ulrich, Orthofix Holdings, B. Braun, CENTINEL SPINE, INTEGRA, Seaspine, RTI Surgical, Zimmer Biomet, Stryker, Johnson & Johnson, Globus Medical, Alphatec Spine, Medtronic, and NuVasive. To expand their market footprint, companies within the spinal implants industry are focusing on strategic R&D investments to enhance implant functionality and compatibility with minimally invasive techniques. They are actively pursuing global expansion through mergers, partnerships, and acquisitions to reach new customer bases and reinforce distribution channels. Integration of robotics and digital navigation into their product portfolios is helping them improve surgical accuracy and patient satisfaction. Firms are also collaborating with clinical institutions to validate product performance, obtain faster regulatory approvals, and strengthen their credibility among healthcare providers worldwide.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Material trends

- 2.2.4 Surgery type trends

- 2.2.5 Indication trends

- 2.2.6 End use trends

- 2.3 CXO Perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of spinal diseases

- 3.2.1.2 Increasing demand for minimally invasive procedures

- 3.2.1.3 Technological advancements

- 3.2.1.4 Favorable reimbursement policies in developed countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of spinal implants and surgeries

- 3.2.2.2 Stringent regulatory scenario in developed countries

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and robotics in spine surgery

- 3.2.3.2 Growing focus on outpatient and ambulatory settings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis

- 3.10 GAP analysis

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1 By region

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Spinal fusion implants

- 5.2.1 Pedicle screws

- 5.2.2 Intervertebral body fusion device (IBFD)

- 5.2.3 Rods

- 5.2.4 Plates

- 5.2.5 Cages

- 5.2.6 Other spinal fusion implants

- 5.3 Dynamic stabilization devices

- 5.4 Artificial discs

- 5.4.1 Cervical

- 5.4.2 Lumbar

- 5.5 Other product types

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium

- 6.3 Cobalt chrome

- 6.4 Stainless steel

- 6.5 Polyetheretherketone (PEEK)

- 6.6 Other materials

Chapter 7 Market Estimates and Forecast, By Surgery Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Open surgery

- 7.3 Minimally invasive surgery

Chapter 8 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Degenerative disc disease

- 8.3 Spinal deformities

- 8.4 Spinal trauma

- 8.5 Fractures

- 8.6 Other indications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Alphatec Spine

- 11.2 B. Braun

- 11.3 CENTINEL SPINE

- 11.4 Globus Medical

- 11.5 INTEGRA

- 11.6 Johnson & Johnson

- 11.7 Medtronic

- 11.8 NuVasive

- 11.9 Orthofix Holdings

- 11.10 RTI Surgical

- 11.11 Seaspine

- 11.12 Spineart

- 11.13 Stryker

- 11.14 Ulrich

- 11.15 Zimmer Biomet

脊椎移植和器械市场规模、份额和成长分析(按产品类型、技术、手术类型、操作类型、最终用户和地区划分)—产业预测(2026-2033 年)

脊椎移植和器械市场规模、份额和成长分析(按产品类型、技术、手术类型、操作类型、最终用户和地区划分)—产业预测(2026-2033 年) 脊椎移植市场规模、份额和成长分析(按产品类型、手术类型、操作类型和地区划分)—产业预测(2026-2033 年)

脊椎移植市场规模、份额和成长分析(按产品类型、手术类型、操作类型和地区划分)—产业预测(2026-2033 年) 微创骶髂关节融合术:全球市场份额和排名、总收入和需求预测(2025-2031年)

微创骶髂关节融合术:全球市场份额和排名、总收入和需求预测(2025-2031年) 脊椎移植和外科器械市场(按产品类型、手术类型、手术入路、年龄层、应用和最终用户划分)-2025-2032年全球预测脊髓神经刺激植入市场:按产品类型、技术、应用和最终用户 - 2025 年至 2032 年全球预测骶髂关节融合市场按产品类型、手术类型、最终用户、手术入路、固定机制和分销管道划分-2025-2032年全球预测

脊椎移植和外科器械市场(按产品类型、手术类型、手术入路、年龄层、应用和最终用户划分)-2025-2032年全球预测脊髓神经刺激植入市场:按产品类型、技术、应用和最终用户 - 2025 年至 2032 年全球预测骶髂关节融合市场按产品类型、手术类型、最终用户、手术入路、固定机制和分销管道划分-2025-2032年全球预测 脊椎植入物市场

脊椎植入物市场 2025年全球脊椎移植市场报告2025年全球防滑盘市场报告2025年骶髂关节融合手术全球市场报告

2025年全球脊椎移植市场报告2025年全球防滑盘市场报告2025年骶髂关节融合手术全球市场报告