|

市场调查报告书

商品编码

1755375

髋关节置换市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Hip Replacement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

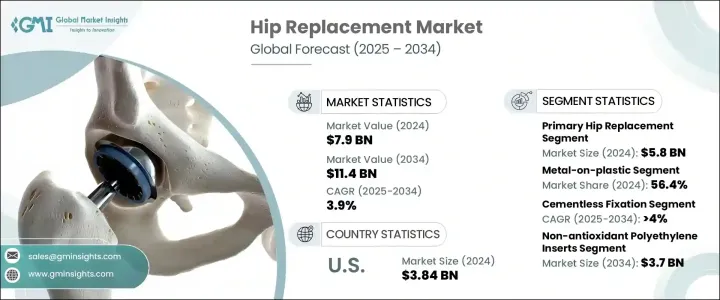

2024年,全球髋关节置换市场规模达79亿美元,预计到2034年将以3.9%的复合年增长率成长,达到114亿美元。技术创新、手术量增加以及关节相关疾病发病率上升等因素共同推动了市场的成长。老年人口不断增长,尤其是患有退化性关节疾病的老年人,仍然是接受髋关节置换手术的主要人群。此外,机器人技术与微创手术方法的结合显着改善了临床疗效。这些进步缩短了住院时间,缩短了復原期,提高了病患满意度,最终推动了全球髋关节置换手术的普及率。

在关节功能逐渐衰退的老年人中,植入手术越来越普遍。由于手术技术和材料的不断发展,这类手术如今取得了更高的成功率,并被广泛接受。此外,医疗基础设施的改善以及患者对治疗结果的教育也促进了市场扩张。创伤病例和骨科损伤数量的增加,以及医疗报销政策的优惠,也提高了髋关节置换手术的实施频率。植入物设计、相容性和耐用性的创新,进一步使骨科医生能够提供有效的、针对患者的具体解决方案。随着活跃老化人群对增强型活动解决方案和长期表现的需求不断增长,市场也在不断发展。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 79亿美元 |

| 预测值 | 114亿美元 |

| 复合年增长率 | 3.9% |

从产品细分来看,2024年,初级髋关节置换器材占据全球市场主导地位,市值达58亿美元。由于广泛应用于各种外科手术,这类器械仍是最常使用的植入物。其广泛应用归因于其与多种髋关节疾病的兼容性以及能够提供可靠的长期疗效。受骨折和老化相关关节磨损等因素驱动,髋关节植入手术数量的不断增加确保了该产品类别的持续成长。

按材料类型划分,金属对塑胶植入物在2024年占据56.4%的市场份额,占据市场主导地位。这种材料组合因其优异的耐磨性、经济性和机械稳定性,仍是首选。金属零件可有效吸收压力,而塑胶内衬可减少关节摩擦,从而提高活动能力并减少长期磨损。由于其有效性、外科医生熟悉度和较低的翻修率,这些植入物在世界各地广泛使用,使其成为医护人员和患者的首选。

以固定方式分析,非骨水泥固定係统在2024年成为领先类别,预计到2034年将以4%的复合年增长率成长。该领域因其提供的长期生物稳定性而备受青睐。与依赖合成黏合剂的骨水泥固定不同,非骨水泥植入物可促进植入物表面周围的自然骨生长。这种生物整合可延长植入物的使用寿命,并降低植入物随时间推移鬆动的可能性。由于其长期成功率较高,年轻患者尤其受益于这种固定方法。改进的表面设计和材料涂层进一步推动了对这种方法的需求,尤其是在微创和门诊手术领域。

植入物市场也呈现显着的趋势。非抗氧化聚乙烯植入物正日益受到关注,预计到2034年其市场规模将达37亿美元。这些植入物以减少氧化磨损而闻名,有助于延长植入物的使用寿命——这对于更活跃、更年轻的个体来说至关重要。其可靠的临床性能、更广泛的可用性和简化的製造流程使其使用量不断增长。医疗保健专业人士青睐这些植入物,因为它们在手术中取得了持续的成功,并且拥有强有力的历史资料,证明了其长期有效性。

在终端用途类别中,医院和诊所在2024年占据了主要收入份额,预计未来几年将大幅成长。这些机构配备了处理复杂骨科手术(包括髋关节置换术)的设备,并提供从术前咨询到术后復健的一体化护理。它们还受益于越来越多地使用先进的外科技术,包括机器人辅助和成像系统,从而提高了手术的准确性。在这些临床环境中进行的微创手术数量不断增加,进一步支持了市场的成长。

2024年,北美占据了全球50.6%的市场份额,这主要得益于其完善的医疗基础设施和日益增长的老龄人口。在北美地区,美国在2024年的市值达到38.4亿美元。骨质疏鬆症、关节炎和肥胖症的发生率上升,增加了髋关节置换手术的需求。公众意识宣传活动和手术选择机会的增加也促进了手术量的上升。

产业参与者持续投资新一代植入物和数位技术,不断增强其产品线。策略合作和技术创新(包括3D列印植入物和机器人手术系统)正在帮助製造商保持竞争力,并更好地满足不断变化的患者需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 创伤病例数上升

- 髋关节炎和骨质疏鬆症的盛行率不断上升

- 最近的技术进步

- 个性化髋关节植入物的需求不断增长

- 产业陷阱与挑战

- 植入物和手术费用高昂

- 严格的监管准则

- 成长动力

- 成长潜力分析

- 监管格局

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 报销场景

- 报销政策对市场成长的影响

- 专利格局

- 管道分析

- 消费者行为分析

- 主要国家髋关节置换手术数量

- 髋关节置换治疗案例

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 主要髋关节置换装置

- 部分髋关节置换装置

- 髋关节置换翻修装置

- 髋关节置换装置

第六章:市场估计与预测:按材料,2021 - 2034 年

- 主要趋势

- 金属与塑料

- 陶瓷-金属

- 陶瓷-塑料

- 陶瓷对陶瓷

第七章:市场估计与预测:按固定材料,2021 - 2034 年

- 主要趋势

- 非骨水泥固定

- 混合固定

- 骨水泥固定

第 8 章:市场估计与预测:按插入件,2021 年至 2034 年

- 主要趋势

- 非抗氧化聚乙烯插入件

- 交联聚乙烯插入件

- 抗氧化聚乙烯内衬

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院和诊所

- 门诊手术中心

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- B Braun

- CONFIRMIS

- Corin

- DePuy Synthes (Johnson & Johnson)

- enovis

- ExaTech Inc

- KyOCERA

- Link

- Medacta International

- MicroPort Orthopedics

- ORTHO DEVELOPMENT

- Smith+Nephew

- stryker

- ZIMMER BIOMET

The Global Hip Replacement Market was valued at USD 7.9 billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 11.4 billion by 2034. The market is experiencing growth due to a combination of technological innovation, increased surgical volume, and rising incidences of joint-related disorders. A growing elderly population, particularly those affected by degenerative joint diseases, continues to be a primary demographic undergoing hip replacement procedures. Moreover, the integration of robotics and minimally invasive surgical methods has significantly enhanced clinical outcomes. These advancements have led to shorter hospital stays, reduced recovery periods, and improved patient satisfaction, ultimately contributing to a higher adoption rate of hip replacement procedures globally.

Implant surgeries are increasingly common among older adults experiencing progressive joint deterioration. These procedures are more successful and widely accepted today, thanks to ongoing developments in surgical techniques and materials. In addition, improved healthcare infrastructure and better patient education regarding treatment outcomes have supported market expansion. The rising number of trauma cases and orthopedic injuries, along with favorable healthcare reimbursement, has also boosted the frequency of hip replacement surgeries. Innovations in implant design, compatibility, and durability further enable orthopedic surgeons to deliver effective, patient-specific solutions. The market continues to evolve with the increasing demand for enhanced mobility solutions and long-term performance among active aging populations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.9 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 3.9% |

In terms of product segmentation, primary hip replacement devices dominated the global market in 2024, with a recorded value of USD 5.8 billion. These devices remain the most commonly used implants due to their broad application across various surgical procedures. Their widespread use is attributed to their compatibility with multiple hip disorders and their ability to provide reliable, long-term results. An increasing number of hip implant procedures-driven by factors such as bone fractures and aging-related joint wear-has ensured continued growth for this product category.

Based on material type, metal-on-plastic implants led the market with a 56.4% share in 2024. This material combination remains a preferred choice due to its excellent wear resistance, affordability, and mechanical stability. The metal component effectively absorbs pressure, while the plastic liner reduces joint friction, leading to improved mobility and reduced wear over time. These implants are commonly used worldwide due to their effectiveness, surgeon familiarity, and lower revision rates, making them a go-to choice for both healthcare professionals and patients.

When analyzed by fixation method, cementless fixation systems emerged as the leading category in 2024 and are forecasted to grow at a CAGR of 4% through 2034. This segment has gained traction due to the long-term biological stability it offers. Unlike cemented fixation, which relies on synthetic adhesives, cementless implants promote natural bone growth around the implant surface. This biological integration offers increased longevity and reduces the chances of implant loosening over time. Younger patients, in particular, benefit from this fixation method due to its higher success rate over extended periods. Improved surface designs and material coatings have further driven demand for this approach, especially in minimally invasive and outpatient surgical settings.

The inserts segment of the market is also experiencing notable trends. Non-antioxidant polyethylene inserts are gaining attention and are projected to reach USD 3.7 billion by 2034. These inserts are known to reduce oxidative wear, which helps enhance implant longevity-a vital consideration for more active and younger individuals. Their growing usage is supported by their reliable clinical performance, broader availability, and simplified manufacturing processes. Healthcare professionals favor these inserts due to consistent procedural success and strong historical data supporting their long-term effectiveness.

Among end-use categories, hospitals and clinics held the dominant revenue share in 2024 and are anticipated to witness substantial growth over the coming years. These facilities are equipped to handle complex orthopedic surgeries, including hip replacements, and offer integrated care that spans pre-surgical consultation through post-surgical rehabilitation. They also benefit from increased access to advanced surgical technologies, including robotic assistance and imaging systems, which enhance procedural accuracy. The rising number of minimally invasive surgeries performed in these clinical environments further supports market growth.

North America accounted for 50.6% of the global market share in 2024, largely due to the presence of well-established healthcare infrastructure and a growing elderly population. Within the region, the United States registered a market value of USD 3.84 billion in 2024. Higher rates of osteoporosis, arthritis, and obesity are increasing the demand for hip replacement procedures. Public awareness campaigns and improved access to surgical options have also contributed to rising procedure volumes.

Industry players continue to enhance their product lines by investing in next-generation implants and digital technologies. Strategic collaborations and technological innovations, including 3D-printed implants and robotic surgical systems, are helping manufacturers stay competitive and better serve evolving patient needs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Forecast model

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Fixation material

- 2.2.5 Inserts

- 2.2.6 End use

- 2.3 CXO Perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in number of trauma cases

- 3.2.1.2 Increasing prevalence of hip arthritis and osteoporosis

- 3.2.1.3 Recent technological advancements

- 3.2.1.4 Growing demand for personalized hip implants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with implants and surgery

- 3.2.2.2 Stringent regulatory guidelines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.8.1 Impact of reimbursement policies on market growth

- 3.9 Patent landscape

- 3.10 Pipeline analysis

- 3.11 Consumer behaviour analysis

- 3.12 Number of hip replacement procedures for key countries

- 3.13 Hip replacement treatment scenario

- 3.14 Porter's analysis

- 3.15 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Primary hip replacement devices

- 5.3 Partial hip replacement devices

- 5.4 Revision hip replacement devices

- 5.5 Hip resurfacing devices

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn and Units)

- 6.1 Key trends

- 6.2 Metal-on-plastic

- 6.3 Ceramic-on-metal

- 6.4 Ceramic-on-plastic

- 6.5 Ceramic-on-ceramic

Chapter 7 Market Estimates and Forecast, By Fixation Material, 2021 - 2034 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Cementless fixation

- 7.3 Hybrid fixation

- 7.4 Cemented fixation

Chapter 8 Market Estimates and Forecast, By Inserts, 2021 - 2034 ($ Mn and Units)

- 8.1 Key trends

- 8.2 Non-antioxidant polyethylene inserts

- 8.3 Cross-linked polyethylene inserts

- 8.4 Antioxidant polyethylene inserts

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Ambulatory surgical centers

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 B Braun

- 11.2 CONFIRMIS

- 11.3 Corin

- 11.4 DePuy Synthes (Johnson & Johnson)

- 11.5 enovis

- 11.6 ExaTech Inc

- 11.7 KyOCERA

- 11.8 Link

- 11.9 Medacta International

- 11.10 MicroPort Orthopedics

- 11.11 ORTHO DEVELOPMENT

- 11.12 Smith+Nephew

- 11.13 stryker

- 11.14 ZIMMER BIOMET

女性用骨盆腔植入市场:2026-2032年全球市场预测(依产品类型、材料、应用、最终用户及通路划分)

女性用骨盆腔植入市场:2026-2032年全球市场预测(依产品类型、材料、应用、最终用户及通路划分) 2026年全球髋关节置换植入术市场报告

2026年全球髋关节置换植入术市场报告 全球髋关节置换市场规模、份额、趋势和成长分析报告(2026-2034年)

全球髋关节置换市场规模、份额、趋势和成长分析报告(2026-2034年) 髋关节植入物市场2025年全球髋关节置换术市场报告

髋关节植入物市场2025年全球髋关节置换术市场报告 全髋关节置换术市场(按产品类型、零件、最终用户和地区划分)髋关节置换植入术市场(按产品、应用、最终用户和地区):未来预测(2026-2032 年)

全髋关节置换术市场(按产品类型、零件、最终用户和地区划分)髋关节置换植入术市场(按产品、应用、最终用户和地区):未来预测(2026-2032 年) 人工髋置换术市场规模、份额、成长分析,按手术方法、材料、最终用户、地区划分 - 按行业预测,2024-2031

人工髋置换术市场规模、份额、成长分析,按手术方法、材料、最终用户、地区划分 - 按行业预测,2024-2031 髋关节置换植入术市场报告:2030 年趋势、预测与竞争分析

髋关节置换植入术市场报告:2030 年趋势、预测与竞争分析 髋关节置换植入术市场规模、份额、趋势分析报告:按产品类型、材料、最终用途、地区和细分市场预测,2024-2030 年

髋关节置换植入术市场规模、份额、趋势分析报告:按产品类型、材料、最终用途、地区和细分市场预测,2024-2030 年