|

市场调查报告书

商品编码

1766173

鸟氨酸转氨甲酰酶缺乏症治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Ornithine Transcarbamylase Deficiency Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

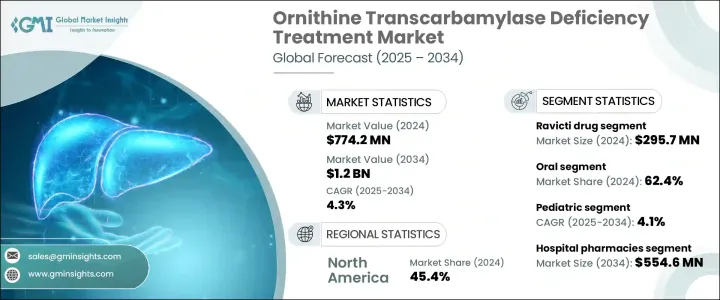

2024年,全球鸟氨酸转氨甲酰酶缺乏症治疗市场规模达7.742亿美元,预计到2034年将以4.3%的复合年增长率成长,达到12亿美元。尿素循环障碍(UCD)发病率的上升以及精准医疗和基因疗法的持续创新推动了市场扩张。医疗保健专业人员和患者意识的提高,以及更先进的诊断工具,有助于提高疾病的检出率并扩大治疗需求。晚髮型病例(尤其是女性)的增多,正在扩大患者群体并刺激需求。

包括基因编辑技术、酵素替代疗法和肝臟靶向小分子在内的新一代疗法的开发,正得到大量研究和临床试验投入的支持。包括孤儿药资格认定、财政诱因和加速审批流程在内的有利监管框架,正在进一步推动市场发展。医疗保健产业的这一领域专注于治疗一种罕见遗传性疾病,这种疾病会导致尿素循环受损,导致血氨水平升高,这种疾病通常危及生命,需要持续治疗。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 7.742亿美元 |

| 预测值 | 12亿美元 |

| 复合年增长率 | 4.3% |

Ravicti 部门在 2024 年的营收为 2.957 亿美元。该部门受益于其易用性和更高的耐受性,尤其受到儿童和老年人的青睐。其使用者友善的配方增强了治疗依从性,这是管理慢性终身疾病的关键因素。该疗法已在多个地区获得监管部门的批准,提高了其在各个医疗体系中的可及性和应用率。其儿科用药的核准显着扩大了适用人群,巩固了该部门的整体主导地位。

2024年,口服治疗领域占了62.4%的市场。口服给药的偏好源于其便捷性,以及能够减少对频繁就诊的依赖,这对于需要持续照护的疾病管理至关重要。缓释技术等药物製剂的进步提高了口服药物的疗效,使其与静脉注射药物相媲美。这项进步不仅提高了患者的依从性,也使得更个人化的给药策略成为可能,促进了口服非处方药的更广泛应用。

2024年,美国鸟氨酸转氨甲酰酶缺乏症治疗市场规模达3.156亿美元。美国高额的医疗保健支出确保了患有非处方药(OTC)缺乏症等罕见疾病的患者能够获得更多治疗选择。製药开发商、研究机构和生物技术公司之间的合作正在加速该领域的创新。此外,《孤儿药法案》等支持性措施正在鼓励罕见疾病疗法的开发和更快的批准。政府资助和激励计画在推动研究和提供救命疗法方面继续发挥关键作用。

影响全球鸟氨酸转氨甲酰酶缺乏症治疗市场的关键参与者包括 Ultragenyx Pharmaceutical、雅培实验室、博士伦斯医疗集团、Arcturus Therapeutics、纽迪希亚(达能集团)、美赞臣(利洁时)、Acer Therapeutics、OrphanPacific、雀巢和安进。为巩固市场地位,鸟氨酸转氨甲酰酶缺乏症治疗市场的公司正专注于多项策略性措施。这些倡议包括加速创新基因疗法和酵素替代解决方案的临床开发、投资合作伙伴关係和许可交易以扩大全球可及性、以及透过孤儿药资格认定确保监管优势。许多公司也正在加强患者支持计画以提高治疗依从性,并建立製造能力以确保稳定的供应链。此外,他们还透过瞄准新兴市场并与区域卫生机构合作以改善诊断和早期干预策略来扩大地域覆盖范围。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 提高对早期发现OTC缺陷的认识

- 危及生命的疾病尚未满足的医疗需求很高

- 公共和私人保险公司提供强有力的保险和报销

- 产业陷阱与挑战

- 核准疗法的可用性有限

- 治疗费用高昂

- 产业陷阱与挑战

- 新生儿筛检扩大,诊断率提高

- 专科药房和罕见疾病基础设施日益普及

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 未来市场趋势

- 管道分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 重点发展

- 併购

- 伙伴关係和合作

- 新产品发布

第五章:市场估计与预测:按产品,2021 年至 2034 年

- 主要趋势

- 丁苯

- 拉维奇蒂

- 阿蒙努尔

- 膳食补充剂

- 其他产品

第六章:市场估计与预测:依管理路线,2021 年至 2034 年

- 主要趋势

- 口服

- 静脉

第七章:市场估计与预测:依年龄组,2021 年至 2034 年

- 主要趋势

- 儿科

- 成年人

第八章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 网路药局

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Abbott Laboratories

- Acer Therapeutics

- Amgen

- Arcturus Therapeutics

- Bausch Health Companies

- Nutricia (Danone Group)

- Mead Johnson (Reckitt Benckiser)

- Nestle

- OrphanPacific

- Ultragenyx Pharmaceutical

The Global Ornithine Transcarbamylase Deficiency Treatment Market was valued at USD 774.2 million in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 1.2 billion by 2034. Market expansion is being driven by the rising incidence of urea cycle disorders (UCDs) and continued innovation in precision medicine and gene therapies. Increased awareness among healthcare professionals and patients, along with more advanced diagnostic tools, are contributing to higher detection rates and broader treatment needs. A growing number of late-onset cases, particularly in females, is expanding the patient base and fueling demand.

The development of next-generation therapies, including gene editing technologies, enzyme replacement treatments, and liver-targeted small molecules, is being supported by significant investments in research and clinical trials. A favorable regulatory framework, including orphan drug designations, financial incentives, and accelerated approval processes, is further propelling the market forward. This segment of the healthcare industry focuses on therapies that address a rare genetic disorder where the urea cycle is impaired, leading to elevated ammonia levels in the bloodstream, an often life-threatening condition requiring ongoing management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $774.2 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 4.3% |

The Ravicti segment generated USD 295.7 million in 2024. This segment benefits from strong patient preference due to its ease of use and improved tolerability, especially for children and the elderly. Its user-friendly formulation enhances treatment adherence, a crucial factor in managing chronic, lifelong conditions. The therapy has gained regulatory approval across several regions, increasing its accessibility and uptake across various healthcare systems. Its approval for pediatric use has notably expanded the eligible population, contributing to the segment's overall dominance.

The oral treatments segment held a 62.4% share in 2024. The preference for oral administration stems from its convenience and ability to reduce dependency on frequent hospital visits, which is essential for managing a condition that requires continuous care. Advancements in pharmaceutical formulations, such as extended-release technologies, have improved the therapeutic effectiveness of oral medications, making them comparable to intravenous options. This progress not only enhances patient compliance but also allows for more personalized dosing strategies, contributing to the broader adoption of oral OTC treatments.

United States Ornithine Transcarbamylase Deficiency Treatment Market was valued at USD 315.6 million in 2024. High healthcare spending in the country ensures greater access to treatment options for patients dealing with rare conditions like OTC deficiency. Collaborative efforts among pharmaceutical developers, research institutes, and biotechnology firms are accelerating innovation in this space. Additionally, supportive initiatives such as the Orphan Drug Act are encouraging the development and faster approval of therapies targeting rare diseases. Government funding and incentive programs continue to play a critical role in advancing research and the availability of life-saving treatments.

Key players shaping the Global Ornithine Transcarbamylase Deficiency Treatment Market include Ultragenyx Pharmaceutical, Abbott Laboratories, Bausch Health Companies, Arcturus Therapeutics, Nutricia (Danone Group), Mead Johnson (Reckitt Benckiser), Acer Therapeutics, OrphanPacific, Nestle, and Amgen. To strengthen their market positions, companies in the ornithine transcarbamylase deficiency treatment market are focusing on several strategic initiatives. These include accelerating clinical development of innovative gene therapies and enzyme replacement solutions, investing in partnerships and licensing deals to expand global access, and securing regulatory advantages through orphan drug designations. Many firms are also enhancing patient support programs to increase treatment adherence and building manufacturing capabilities to ensure steady supply chains. Additionally, they are broadening their geographic footprint by targeting emerging markets and aligning with regional health agencies to improve diagnosis and early intervention strategies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.1.1 Key market trends

- 2.1.2 Regional

- 2.1.3 Product

- 2.1.4 Route of administration

- 2.1.5 Age group

- 2.1.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased awareness for earlier detection of OTC deficiency

- 3.2.1.2 High unmet medical need for life-threatening condition

- 3.2.1.3 Strong insurance and reimbursement by public and private insurers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited availability of approved therapies

- 3.2.2.2 High cost of treatment

- 3.2.3 Industry pitfalls and challenges

- 3.2.3.1 Increasing diagnosis rates due to expanded newborn screening

- 3.2.3.2 Growing availability of specialty pharmacies and rare disease infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Pipeline analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key development

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New Product Launches

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Buphenyl

- 5.3 Ravicti

- 5.4 Ammonul

- 5.5 Dietary supplements

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Intravenous

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatrics

- 7.3 Adults

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Acer Therapeutics

- 10.3 Amgen

- 10.4 Arcturus Therapeutics

- 10.5 Bausch Health Companies

- 10.6 Nutricia (Danone Group)

- 10.7 Mead Johnson (Reckitt Benckiser)

- 10.8 Nestle

- 10.9 OrphanPacific

- 10.10 Ultragenyx Pharmaceutical

鸟胺酸氨甲酰基转移酶缺乏症治疗市场报告:趋势、预测和竞争分析(至2031年)

鸟胺酸氨甲酰基转移酶缺乏症治疗市场报告:趋势、预测和竞争分析(至2031年) 全球鸟氨酸转氨甲酰酶缺乏症治疗市场:成长、展望与竞争分析(2025-2033)

全球鸟氨酸转氨甲酰酶缺乏症治疗市场:成长、展望与竞争分析(2025-2033) 全球鸟胺酸氨甲酰基转移酶缺乏症市场规模:依产品类型、最终用户、区域范围和预测

全球鸟胺酸氨甲酰基转移酶缺乏症市场规模:依产品类型、最终用户、区域范围和预测