|

市场调查报告书

商品编码

1766176

混合印刷系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Hybrid Printing System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

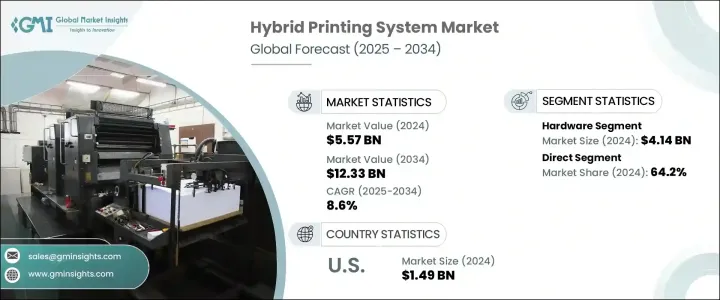

2024年,全球混合印刷系统市场规模达55.7亿美元,预计到2034年将以8.6%的复合年增长率成长,达到123.3亿美元。由于混合印刷能够提供个人化、短版印刷和高速印刷,同时保持成本效益,多个行业对混合印刷的需求正在增长。个人护理、包装商品和饮料等快节奏行业的企业正在转向混合印刷系统,以客製化标籤和包装来满足即时行销需求。透过将柔版印刷或凹版印刷等传统类比技术与现代数位喷墨或墨粉系统相结合,这些解决方案支援灵活、大量生产,并缩短週转时间。这种转变正在重新定义包装工作流程,并实现更快、更高品质的产出。

线上零售和智慧包装的日益普及也提升了混合系统的吸引力。电子商务需要可追溯的品牌包装,其中包含可扫描和安全元素——而混合印表机可以轻鬆处理这些功能。这些解决方案既能提升产品安全性,也能提升品牌知名度。除了包装之外,混合系统还广泛应用于时尚、标牌和广告领域,这些领域需要快速的设计变更和客製化印刷。随着这些应用的发展,混合印刷已成为高效率满足复杂印刷需求的重要工具。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 55.7亿美元 |

| 预测值 | 123.3亿美元 |

| 复合年增长率 | 8.6% |

硬体组件领域在2024年创造了41.4亿美元的产值,预计到2034年将以8.5%的复合年增长率成长。随着混合印刷市场的扩张,製造商正在大力投资强大且适应性强的硬体系统,这些系统能够将类比可靠性与数位精度相结合。印刷机架构、油墨管理和列印头方面的创新正在突破界限,从而提高品质和生产效率。这些升级对于满足纺织、包装和行销等行业不断变化的需求至关重要,因为这些行业对正常运行时间、速度和准确性的要求不容置疑。

2024年,直销通路占了64.2%的市场份额,预计2025年至2034年期间的复合年增长率将达到8.4%。这一成长归因于买家在购买混合印表机等复杂系统时,更重视个人化服务和深入的技术指导。直销模式能够提供客製化的入门指导和维护计划,并简化软体和硬体之间的整合。无需中介机构也简化了沟通,缩短了支援回应时间,并增强了买家关係。越来越多地使用数位平台进行产品教育和客户支持,也增强了直销模式在该领域的吸引力。

2024年,美国混合印刷系统市场规模达14.9亿美元,预计2034年将以8.7%的复合年增长率成长。美国凭藉其高度发展的製造业、对新技术的早期应用,以及医疗保健、消费品和商业印刷等各领域对高效、可定製印刷解决方案日益增长的需求,引领了这一区域市场。产业先锋的涌现和强大的研发实力巩固了这一领先地位。美国国内企业持续部署自动化工具、模组化印刷解决方案和人工智慧增强型工作流程,进一步巩固了其在混合印刷创新和应用领域的主导地位。

业界顶尖企业包括富士软片、惠普(HP Indigo)、得世特(Durst)、博斯特(Bobst)、柯尼卡美能达、MPS Systems、多米诺印刷科学、纽博泰(Nilpeter)、佳能、赛康(Xeikon)、Screen Graphic Solutions、欧米特(Omet)、EFI、Bitam(海德堡)。为了保持竞争力,混合印刷系统市场的公司正专注于策略性产品创新和垂直整合。许多公司正在透过在更靠近需求中心的地方建立製造和服务设施来扩大其全球影响力。企业正在投资于用户友好的设计改进、先进的墨水技术和可扩展的列印模组。与软体供应商的合作有助于改善工作流程自动化和基于云端的列印管理。此外,企业正在加强技术培训和售后支援计划,以期为客户创造长期价值并建立品牌忠诚度。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 短期、客製化印刷和高速操作的需求不断增长

- 类比和数位技术的融合

- 电子商务和智慧包装的成长

- 扩大在各行业的应用

- 产业陷阱与挑战

- 技术复杂性和整合问题

- 维护和营运成本

- 机会

- 成长动力

- 成长潜力分析

- 未来市场趋势

- 科技与创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品

- 监管格局

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 贸易统计(HS 编码 - 8443)

- 主要进口国

- 主要出口国

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- Industry structure and concentration

- Competitive intensity assessment

- 公司市占率分析

- 竞争定位矩阵

- 产品定位

- 性价比定位

- 地理分布

- 创新能力

- 战略仪表板

- Competitive benchmarking

- Strategic initiatives assessment

- SWOT analysis of key players

- 未来竞争前景

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 传统印刷

- 非击打式印刷

第六章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 软体

- 服务

第七章:市场估计与预测:依自动化水平,2021 - 2034 年

- 主要趋势

- 手动混合印刷系统

- 半自动混合印刷系统

- 全自动混合印刷系统

第八章:市场估计与预测:依油墨类型,2021 - 2034 年

- 主要趋势

- UV油墨

- 溶剂型墨水

- 水性墨水

- 乳胶墨水

- 热昇华墨水

第九章:市场预估与预测:依基材类型,2021 - 2034

- 主要趋势

- 纸

- 塑胶薄膜

- 箔

- 纺织品/布料

- 玻璃

- 其他(金属板、瓦楞纸板/纸板)

第十章:市场估计与预测:依技术分类,2021 - 2034 年

- 主要趋势

- LED UV混合印刷

- 传统UV混合印刷

- 柔印喷墨混合

- 柔版印刷-墨粉混合

- 萤幕-DTG(直接成衣)混合

- 萤幕-DTF(直接製片)混合

- 胶印喷墨混合

- 胶印墨粉混合

- 加减混合

- 多材料混合系统

第 11 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 标籤

- 软包装

- 折迭纸盒

- 瓦楞包装

- 行销资料

- 书籍和出版物

- 时尚纺织品

- 家纺

- 其他(安全印刷、玻璃印刷)

第 12 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 快速消费品

- 製药

- 纺织服装

- 汽车

- 电子产品

- 其他(零售和电子商务)

第 13 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 直接的

- 间接

第 14 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 马来西亚

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 沙乌地阿拉伯

- 阿联酋

- 南非

第十五章:公司简介

- Bobst

- Canon

- Domino Printing Sciences

- Durst

- EFI

- Fujifilm

- Gallus (a Heidelberg company)

- HP (HP Indigo)

- Konica Minolta

- Mark Andy

- MPS Systems

- Nilpeter

- Omet

- Screen Graphic Solutions

- Xeikon

The Global Hybrid Printing System Market was valued at USD 5.57 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 12.33 billion by 2034. Demand for hybrid printing is rising across multiple sectors due to its ability to offer personalized, short-run, and high-speed printing, all while maintaining cost-effectiveness. Businesses in fast-paced industries like personal care, packaged goods, and beverages are turning to hybrid systems to meet real-time marketing demands with custom labeling and packaging. By merging traditional analog technologies such as flexographic or gravure printing with modern digital inkjet or toner systems, these solutions support flexible, high-volume production with reduced turnaround. This shift is redefining packaging workflows and enabling faster, higher-quality outputs.

The increasing popularity of online retail and smart packaging has also boosted the appeal of hybrid systems. E-commerce requires traceable, branded packaging that includes scannable and secure elements-functions that hybrid printers can handle with ease. These solutions enhance both product security and brand visibility. Beyond packaging, hybrid systems are being widely used in fashion, signage, and advertising, where rapid design changes and custom prints are routine. As these applications evolve, hybrid printing becomes a vital tool to meet complex printing requirements efficiently.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.57 Billion |

| Forecast Value | $12.33 Billion |

| CAGR | 8.6% |

The hardware component segment generated USD 4.14 billion in 2024 and is anticipated to grow at a CAGR of 8.5% through 2034. As the market for hybrid printing expands, manufacturers are investing heavily in robust and adaptable hardware systems capable of merging analog reliability with digital precision. Innovations in press architecture, ink management, and print heads are pushing boundaries to deliver enhanced quality and production efficiency. These upgrades are critical to meeting the evolving needs of sectors like textiles, packaging, and marketing, where uptime, speed, and accuracy are non-negotiable.

The direct sales channel segment accounted for 64.2% share in 2024 and is forecasted to grow at a CAGR of 8.4% between 2025 and 2034. This growth is attributed to the value buyers place on personalized service and deep technical guidance when purchasing complex systems like hybrid printers. Selling directly allows for tailored onboarding, maintenance plans, and easier integration between the software and hardware. The absence of intermediaries also streamlines communication, enhances support response time, and strengthens buyer relationships. Increasing use of digital platforms for product education and customer support is also reinforcing the appeal of direct-to-customer sales in this space.

United States Hybrid Printing System Market was valued at USD 1.49 billion in 2024 and is estimated to grow at a CAGR of 8.7% through 2034. The U.S. leads this regional segment due to its highly developed manufacturing sector, early adoption of new technologies, and increasing demand for efficient, customizable print solutions across varied fields like healthcare, consumer goods, and commercial printing. The presence of industry pioneers and strong R&D backing contributes to this leadership. Domestic businesses continue to implement automation tools, modular printing solutions, and AI-enhanced workflows, further supporting the country's dominance in hybrid printing innovation and implementation.

Top industry players include Fujifilm, HP (HP Indigo), Durst, Bobst, Konica Minolta, MPS Systems, Domino Printing Sciences, Nilpeter, Canon, Xeikon, Screen Graphic Solutions, Omet, EFI, Gallus (a Heidelberg company), Mark Andy. To stay competitive, companies in the hybrid printing system market are focusing on strategic product innovation and vertical integration. Many are expanding their global footprints by launching manufacturing and service facilities closer to demand centers. Firms are investing in user-friendly design improvements, advanced ink technologies, and scalable print modules. Partnerships with software vendors help improve workflow automation and cloud-based print management. Additionally, players are ramping up technical training and after-sales support programs to create long-term value for customers and build brand loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for short-run, customizable printing and high-speed operation

- 3.2.1.2 Integration of analog and digital technologies

- 3.2.1.3 Growth in e-commerce and smart packaging

- 3.2.1.4 Expanding use in various industries

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Technical complexity and integration issues

- 3.2.2.2 Maintenance and operational costs

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code - 8443)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.1.1 Industry structure and concentration

- 4.1.2 Competitive intensity assessment

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.3.1 Product positioning

- 4.3.2 Price-performance positioning

- 4.3.3 Geographic presence

- 4.3.4 Innovation capabilities

- 4.4 Strategic dashboard

- 4.4.1 Competitive benchmarking

- 4.4.1.1 Manufacturing capabilities

- 4.4.1.2 Product portfolio strength

- 4.4.1.3 Distribution network

- 4.4.1.4 R&D investments

- 4.4.2 Strategic initiatives assessment

- 4.4.3 SWOT analysis of key players

- 4.4.1 Competitive benchmarking

- 4.5 Future competitive outlook

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Conventional printing

- 5.3 Non-Impact printing

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Hardware

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates & Forecast, By Automation Level, 2021 - 2034, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Manual hybrid printing systems

- 7.3 Semi-automated hybrid printing systems

- 7.4 Fully automated hybrid printing systems

Chapter 8 Market Estimates & Forecast, By Ink Type, 2021 - 2034, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 UV-based ink

- 8.3 Solvent-based ink

- 8.4 Aqueous ink

- 8.5 Latex ink

- 8.6 Dye sublimation ink

Chapter 9 Market Estimates & Forecast, By Substrate Type, 2021 - 2034, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Paper

- 9.3 Plastic films

- 9.4 Foils

- 9.5 Textiles/Fabrics

- 9.6 Glass

- 9.7 Others (Metal sheets, Corrugated boards/Cardboard)

Chapter 10 Market Estimates & Forecast, By Technology, 2021 - 2034, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 LED UV hybrid printing

- 10.3 Conventional UV hybrid printing

- 10.4 Flexo-inkjet hybrid

- 10.5 Flexo-toner hybrid

- 10.6 Screen-DTG (Direct to Garment) hybrid

- 10.7 Screen-DTF (Direct to Film) hybrid

- 10.8 Offset-inkjet hybrid

- 10.9 Offset-toner hybrid

- 10.10 Additive-subtractive hybrid

- 10.11 Multi-material hybrid systems

Chapter 11 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 Labels

- 11.3 Flexible packaging

- 11.4 Folding cartons

- 11.5 Corrugated packaging

- 11.6 Marketing materials

- 11.7 Books and publications

- 11.8 Fashion textiles

- 11.9 Home textiles

- 11.10 Other (Security printing, Glass printing)

Chapter 12 Market Estimates & Forecast, By End Use, 2021 - 2034, (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 FMCG

- 12.3 Pharmaceutical

- 12.4 Textile and apparel

- 12.5 Automotive

- 12.6 Electronics

- 12.7 Other (Retail and E-commerce)

Chapter 13 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Million Units)

- 13.1 Key trends

- 13.2 Direct

- 13.3 Indirect

Chapter 14 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Million Units)

- 14.1 Key trends

- 14.2 North America

- 14.2.1 U.S.

- 14.2.2 Canada

- 14.3 Europe

- 14.3.1 Germany

- 14.3.2 UK

- 14.3.3 France

- 14.3.4 Italy

- 14.3.5 Spain

- 14.4 Asia Pacific

- 14.4.1 China

- 14.4.2 India

- 14.4.3 Japan

- 14.4.4 South Korea

- 14.4.5 Australia

- 14.4.6 Indonesia

- 14.4.7 Malaysia

- 14.5 Latin America

- 14.5.1 Brazil

- 14.5.2 Mexico

- 14.6 MEA

- 14.6.1 Saudi Arabia

- 14.6.2 UAE

- 14.6.3 South Africa

Chapter 15 Company Profiles

- 15.1 Bobst

- 15.2 Canon

- 15.3 Domino Printing Sciences

- 15.4 Durst

- 15.5 EFI

- 15.6 Fujifilm

- 15.7 Gallus (a Heidelberg company)

- 15.8 HP (HP Indigo)

- 15.9 Konica Minolta

- 15.10 Mark Andy

- 15.11 MPS Systems

- 15.12 Nilpeter

- 15.13 Omet

- 15.14 Screen Graphic Solutions

- 15.15 Xeikon

全球混合印刷市场

全球混合印刷市场 混合印刷技术市场规模、份额、趋势分析报告:按组件、按基板、按应用、按地区、细分市场预测,2024-2030

混合印刷技术市场规模、份额、趋势分析报告:按组件、按基板、按应用、按地区、细分市场预测,2024-2030 混合印刷市场 - 全球市场规模、份额、趋势分析、机会、预测报告,2019-2030

混合印刷市场 - 全球市场规模、份额、趋势分析、机会、预测报告,2019-2030