|

市场调查报告书

商品编码

1766182

水痘疫苗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Varicella Vaccine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

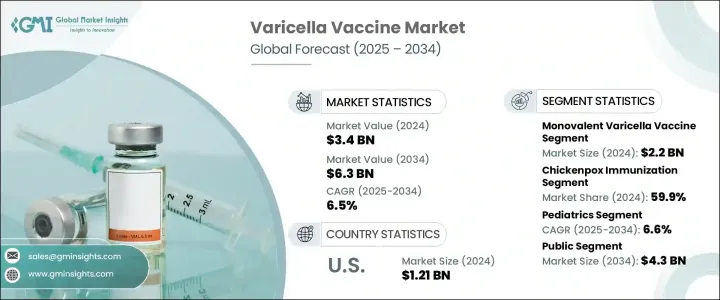

2024年,全球水痘疫苗市场规模达34亿美元,预计2034年将以6.5%的复合年增长率成长至63亿美元。全球水痘(又称水痘)负担的不断加重,持续成为该市场的主要驱动力。高传播率和反覆爆发的疫情(尤其是在人口稠密的地区)加剧了对有效免疫解决方案的需求。早期疫苗接种意识的不断提升,加上政府主导的强大免疫接种运动和资金支持,正在加速全球水痘疫苗的普及。技术进步也在塑造市场发展势头,尤其是联合疫苗的研发,这种疫苗可以减少所需剂量并提高患者的依从性。

国家免疫规划中日益倾向于采用综合免疫接种程序,这有助于提高疫苗覆盖率。此外,随着医疗保健系统强调预防措施和常规免疫接种,疫苗需求持续成长。一些地区老龄人口的不断增长也促使人们对疫苗接种保持持续兴趣,因为老年人更容易感染水痘-带状疱疹病毒。随着医疗保健服务覆盖范围的扩大,以及旨在提高疫苗覆盖率和可负担性的公私合作的持续推进,预计未来几年水痘疫苗市场将持续稳定成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 34亿美元 |

| 预测值 | 63亿美元 |

| 复合年增长率 | 6.5% |

单价水痘疫苗市场在2024年以22亿美元的估值领先市场。其在常规免疫计划中的广泛应用,尤其是在资源匮乏的国家,进一步巩固了其市场主导地位。与多价疫苗相比,单价疫苗通常价格更实惠、更易于储存且物流更便捷,使其成为大规模公共卫生活动的理想选择。长期以来,单价疫苗的持续使用赢得了卫生当局和临床医生的充分信任,并使其广受欢迎。单价疫苗凭藉其可靠的有效性和长期的安全性记录,成为全球儿童免疫接种计画的首选。凭藉其可靠性和成本效益,单价疫苗在已开发国家和发展中国家都持续受到青睐。

2024年,水痘免疫接种占比最高,达59.9%。这一领先地位归功于儿童对水痘预防的广泛需求。拥有先进医疗体系的国家已将水痘疫苗纳入其全民免疫政策,实现了高接种率。即使在新兴市场,更完善的医疗服务、日益提升的家长意识以及推广水痘疫苗接种的国家计画也正在推动这一趋势。由于水痘病毒传染性极强,各国继续将疫苗的取得和接种放在首位。持续的教育和推广工作正在提高儿童的依从性,并使水痘免疫接种成为全球儿童医疗保健的标准组成部分。

2024年,北美水痘疫苗市场占据39.1%的市占率。这一增长得益于完善的医疗体系和积极的监管环境。该地区的公共卫生机构致力于确保水痘疫苗的广泛普及和保险报销,从而最大限度地降低个人的直接成本。疫苗的早期普及、高额的保险覆盖率以及强有力的公共卫生宣传推动了疫苗的广泛应用。因此,该地区将继续保持强劲的需求,预计在整个预测期内仍将是全球水痘疫苗市场的主要贡献者。

全球水痘疫苗市场的领先公司包括 SK Bioscience、赛诺菲、GC Pharma(绿十字控股)、葛兰素史克、武田药品工业株式会社、Seqirus、田边三菱製药株式会社、诺和医疗、默克、科兴生物、BPL、Bio-Med 和长春长生生命科学有限公司。水痘疫苗市场的主要参与者正在利用一系列策略性措施来加强其市场地位。主要重点是扩大生产能力和改善冷链物流,以确保全球供应的一致性。各公司也正在研发方面投入资金,以研发将水痘保护整合到更广泛的免疫计画中的联合疫苗,从而提高便利性和依从性。与政府和全球卫生机构的策略合作正在促进更广泛的分发,特别是在中低收入国家。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 水痘盛行率不断上升

- 政府不断扩大免疫计划

- 疫苗研发技术进步

- 产业陷阱与挑战

- 严格的监管要求

- 疫苗储存和运输成本高

- 市场机会

- 扩大国家免疫计划

- 成人和青少年疫苗接种需求不断增长

- 联合疫苗的成长

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 当前的技术趋势

- 新兴技术

- 未来市场趋势

- 管道分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按疫苗类型,2021 年至 2034 年

- 主要趋势

- 单价水痘疫苗

- 水痘联合疫苗

第六章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 水痘免疫

- 腮腺炎、麻疹、德国麻疹和水痘 (MMRV) 免疫接种

第七章:市场估计与预测:依年龄组,2021 年至 2034 年

- 主要趋势

- 儿科

- 青少年和成年人

第 8 章:市场估计与预测:按采购,2021 年至 2034 年

- 主要趋势

- 民众

- 私人的

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Bio-Med

- Changchun Changsheng Life Sciences Limited

- GC Pharma (Green Cross Holdings)

- GlaxoSmithKline

- Merck

- Mitsubishi Tanabe Pharma Corporation

- Novo Medi Sciences

- Sanofi

- Seqirus

- Sinovac Biotech

- SK Bioscience

- Takeda Pharmaceutical Company Limited

The Global Varicella Vaccine Market was valued at USD 3.4 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 6.3 billion by 2034. The increasing global burden of varicella, or chickenpox, continues to be a major driver of this market. High transmission rates and recurring outbreaks, especially in densely populated regions, are raising the demand for effective immunization solutions. The rising awareness of early vaccination, combined with strong government-led immunization campaigns and funding support, is accelerating the uptake of varicella vaccines globally. Technological advancements are also shaping the market's momentum, particularly the development of combination vaccines that reduce the number of required doses and enhance patient compliance.

The growing shift toward integrated immunization schedules in national programs is helping increase coverage. Additionally, as healthcare systems emphasize preventive measures and routine immunization, demand continues to grow. The increasing elderly population in several regions has also contributed to sustained interest in vaccination due to susceptibility to varicella-zoster reactivation. With expanded access to healthcare and ongoing public-private partnerships aimed at improving vaccine reach and affordability, the market for varicella vaccines is anticipated to experience consistent and steady growth in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 6.5% |

The monovalent varicella vaccine segment led the market with a valuation of USD 2.2 billion in 2024. Its widespread use in routine immunization programs, especially in countries with limited resources, supports this dominance. These vaccines are often more affordable, easier to store, and logistically simpler than multivalent alternatives, making them ideal for large-scale public health campaigns. Their consistent usage over time has built strong trust among health authorities and clinicians, helping maintain their popularity. Proven efficacy and long-standing safety records have made monovalent vaccines the preferred choice for childhood immunization schedules globally. They continue to gain traction in both developed and developing countries due to their reliability and cost-efficiency.

In 2024, the chickenpox immunization segment accounted for the largest share at 59.9%. This leadership is attributed to the widespread demand for childhood varicella protection. Countries with advanced healthcare systems have integrated varicella vaccination into their universal immunization policies, resulting in high uptake. Even in emerging markets, stronger healthcare access, growing parental awareness, and national programs promoting varicella vaccination are helping drive this trend. With the virus being highly contagious, countries continue to prioritize vaccine access and delivery. Continuous education and outreach efforts are increasing compliance and making immunization against chickenpox a standard part of pediatric healthcare globally.

North America Varicella Vaccine Market held a 39.1% share in 2024. This growth is supported by well-established healthcare systems and proactive regulatory environments. Public health agencies in the region have helped ensure that varicella vaccines are widely available and reimbursed under insurance plans, minimizing direct costs for individuals. The early availability of the vaccine, high insurance coverage, and strong public health messaging have driven significant adoption. As a result, the region continues to show strong demand and is expected to remain a dominant contributor to the global varicella vaccine market throughout the forecast period.

Leading companies in the Global Varicella Vaccine Market include SK Bioscience, Sanofi, GC Pharma (Green Cross Holdings), GlaxoSmithKline, Takeda Pharmaceutical Company Limited, Seqirus, Mitsubishi Tanabe Pharma Corporation, Novo Medi Sciences, Merck, Sinovac Biotech, BPL, Bio-Med, and Changchun Changsheng Life Sciences Limited. Key players in the varicella vaccine market are leveraging a range of strategic initiatives to strengthen their market presence. A major focus is on expanding production capacity and improving cold-chain logistics to ensure consistent global supply. Companies are also investing in research and development to create combination vaccines that integrate varicella protection into broader immunization schedules, enhancing convenience and compliance. Strategic collaborations with governments and global health agencies are facilitating broader distribution, especially in low- and middle-income countries.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vaccine type

- 2.2.3 Application

- 2.2.4 Age group

- 2.2.5 Procurement

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chickenpox

- 3.2.1.2 Growing immunization programs by the government

- 3.2.1.3 Technological advancements in vaccine development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory requirements

- 3.2.2.2 High cost of storage and transportation of vaccine

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of National Immunization Programs

- 3.2.3.2 Rising demand for adult and adolescent vaccination

- 3.2.3.3 Growth in combination vaccines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pipeline analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Vaccine Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Monovalent varicella vaccine

- 5.3 Combination varicella vaccine

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chickenpox immunization

- 6.3 Mumps, measles, rubella, and varicella (MMRV) immunization

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatrics

- 7.3 Adolescents and adults

Chapter 8 Market Estimates and Forecast, By Procurement, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Public

- 8.3 Private

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bio-Med

- 10.2 Changchun Changsheng Life Sciences Limited

- 10.3 GC Pharma (Green Cross Holdings)

- 10.4 GlaxoSmithKline

- 10.5 Merck

- 10.6 Mitsubishi Tanabe Pharma Corporation

- 10.7 Novo Medi Sciences

- 10.8 Sanofi

- 10.9 Seqirus

- 10.10 Sinovac Biotech

- 10.11 SK Bioscience

- 10.12 Takeda Pharmaceutical Company Limited