|

市场调查报告书

商品编码

1766207

高脂(>85%)奶油市场机会、成长动力、产业趋势分析及2025-2034年预测High Fat (>85%) Butter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

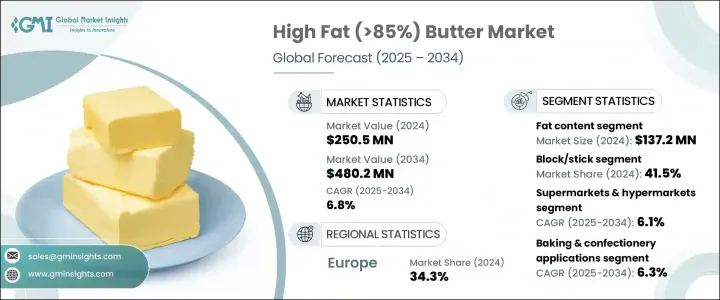

2024年,全球高脂(>85%)奶油市场规模达2.505亿美元,预计到2034年将以6.8%的复合年增长率成长,达到4.802亿美元。这项稳定成长的动力源自于消费者对更浓郁、更天然、更手工的乳製品日益增长的偏好。高脂奶油曾经一度仅限于美食烘焙和高级餐饮等小众领域,如今随着低碳水化合物和生酮饮食等潮流的兴起,在註重健康的消费者群体中也逐渐受到青睐。此外,一个新兴的高端细分市场也正在兴起,专注于采用传统搅拌方式生产的清洁标籤、有机认证和原产地认证黄油。

儘管供应和价格波动,但人们对美味乳製品的需求仍然强劲。产品创新、人们对脂肪功能益处的认识不断提高,以及全球人口日益增长对品质和真实性的高标准,都推动了市场的扩张。此外,零售策略的不断演变、新兴市场准入的不断扩大以及特色食品店和电商平台的兴起,都支持着市场的持续成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 2.505亿美元 |

| 预测值 | 4.802亿美元 |

| 复合年增长率 | 6.8% |

烘焙和糖果市场预计将以更快的速度成长,复合年增长率为 6.3%。在高脂(>85%)奶油市场中,由于对优质糕点、饼干和巧克力的卓越质地、浓郁风味和稳定品质的需求日益增长,烘焙和糖果占据了主导地位。烹饪用途也在不断增长,越来越多的厨师选择高脂黄油用于煎炒、製作酱汁和提升风味。追求浓郁顺滑涂抹酱和食材的消费者进一步推动了这项需求,而生酮饮食和高脂饮食等营养趋势也正在扩大奶油在饮食应用中的作用。

到2024年,块状和条状食品的市场份额将达到41.5%,预计复合年增长率将达到6.4%,从而吸引更广泛的消费者群体。这些食品形式将继续占据主导地位,尤其是在西部地区,因为它们在烹饪和烘焙过程中方便、熟悉且易于计量。注重健康的城市消费者尤其青睐这些柔软易涂抹的食品形式,因为它们可以直接涂抹在麵包和饼干上,既方便又不影响口感。

2024年,欧洲高脂(>85%)奶油市场占34.3%的份额。这一主导地位源自于该地区根深蒂固的烹饪传统,而奶油在传统食谱和美食烹饪中扮演着至关重要的角色。欧洲消费者对高品质乳製品有着成熟的鑑赏力,注重产品的真实性、浓郁的风味和手工生产工艺。此外,消费者对优质和清洁标籤产品的广泛认知,也推动了零售和餐饮服务业对高脂黄油的稳定需求。成熟的乳製品生产商和强大的分销网络进一步巩固了欧洲作为该市场关键参与者的地位,确保了其能够持续供应满足消费者挑剔口味的特色黄油产品。

推动高脂(>85%)奶油市场创新和分销的关键参与者包括Ornua合作社有限公司(Kerrygold)、Arla Foods amba(Lurpak)、Lactalis集团(President)、恆天然合作社集团(Anchor)和古吉拉特邦合作牛奶营销联合会有限公司(Amul)。达能公司、雀巢公司、JM Smucker公司(Eagle Brand)、Arla Foods和Friesland Campina NV在炼乳和淡奶领域发挥重要作用。

为了巩固市场地位,高脂黄油行业的公司正优先考虑产品创新,专注于清洁标籤和有机认证,以满足消费者日益增长的透明度和品质需求。他们不断扩展风味组合,推出添加了香草、香料和益生菌的黄油,以占领利基烹饪和健康细分市场。行销工作强调产品的真实性和手工性,以吸引寻求优质天然乳製品的消费者。与专业零售商和线上平台建立策略伙伴关係,提升了产品的可近性和消费者覆盖率。此外,对永续采购和生产实践的投资正在提升品牌声誉,同时也符合环保理念。这些综合策略使公司能够建立忠诚度,并进入不断扩张的全球市场。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 按脂肪含量

- 脂肪含量85-90%

- 脂肪含量90-95%

- 脂肪含量 95%+(无水乳脂/奶油)

- 按风味特征

- 咸味

- 无盐

- 培养/发酵

- 调味和注入

第六章:市场估计与预测:依形式,2021 - 2034 年

- 主要趋势

- 阻挡/黏住

- 可涂抹

- 澄清/酥油

- 其他的

第七章:市场估计与预测:按来源,2021 - 2034 年

- 主要趋势

- 传统的

- 有机的

- 草饲

- 特种动物来源

- 水牛

- 山羊

- 羊

- 其他的

第八章:市场估计与预测:按包装类型,2021 - 2034 年

- 主要趋势

- 积木/木棍

- 桶子和容器

- 散装包装

- 特色及礼品包装

- 其他的

第九章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 超市和大卖场

- 特色商店和美食商店

- 网路零售

- 电子商务平台

- 直接面向消费者的网站

- 订阅服务

- 餐饮业

- 其他的

第 10 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 烹饪应用

- 烹饪与煎炒

- 酱汁和乳剂

- 其他烹饪用途

- 烘焙和糖果

- 糕点和迭层麵团

- 蛋糕和饼干

- 糖果产品

- 涂抹酱和配料

- 麵包和吐司

- 饼干和咸味食品

- 其他传播应用

- 饮食和营养应用

- 生酮饮食

- 防弹咖啡和饮料

- 其他饮食用途

- 工业应用

- 食品製造

- 化妆品和个人护理

- 其他工业用途

- 其他的

第 11 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 家庭/零售消费者

- 食品服务业

- 高级餐厅

- 麵包店和糕点店

- 饭店和餐饮

- 其他餐饮服务机构

- 食品加工业

- 烘焙和糖果製造商

- 即食食品和预製食品

- 其他食品加工机

- 其他的

第 12 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十三章:公司简介

- Kerrygold (Ornua Co-operative Limited)

- Lurpak (Arla Foods amba)

- President (Lactalis Group)

- Anchor (Fonterra Co-operative Group)

- Amul (Gujarat Cooperative Milk Marketing Federation Ltd.)

- Land O'Lakes, Inc.

- Organic Valley

- Straus Family Creamery

- Vermont Creamery (Land O'Lakes, Inc.)

- Isigny Sainte-Mere

- Plugra (Dairy Farmers of America)

- Valio Ltd.

- Finlandia Cheese, Inc. (Valio Ltd.)

- Meggle Group GmbH

- Gourmet Food Holdings (Pepe Saya)

The Global High Fat (>85%) Butter Market was valued at USD 250.5 million in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 480.2 million by 2034. This steady growth is driven by a rising consumer preference for richer, more natural, and artisanal dairy products. High-fat butter, once limited to niche segments such as gourmet baking and fine dining, has now gained traction among health-conscious consumers following trends like low-carb and ketogenic diets. There is an emerging premium segment focused on clean-label, organically certified, and origin-verified butter produced through traditional churning methods.

Despite fluctuations in supply and price, the demand for indulgent, flavorful dairy items remains strong. Innovations in product offerings, increased awareness of fat's functional benefits, and growing global populations with high standards for quality and authenticity are all contributing to the market's expansion. Additionally, evolving retail strategies, greater access to emerging markets, and the rise of specialty food stores and e-commerce platforms support ongoing market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $250.5 Million |

| Forecast Value | $480.2 Million |

| CAGR | 6.8% |

The baking and confectionery segment is projected to grow at a faster pace, with a CAGR of 6.3%. Within the high-fat (>85%) butter market, baking and confectionery dominate application trends thanks to growing demand for superior texture, rich flavor, and consistent quality in premium pastries, cookies, and chocolates. Culinary uses are also on the rise, as chefs increasingly choose high-fat butter for sauteing, sauces, and boosting flavor profiles. Consumers seeking indulgent, creamy spreads and toppings are further driving this demand, while nutritional trends like keto and high-fat diets are expanding butter's role in dietary applications.

In 2024, the blocks and sticks segment accounted for a 41.5% share and is projected to grow at a CAGR of 6.4%, attracting a broader consumer base. These formats continue to dominate, especially in Western regions, due to their convenience, familiarity, and ease of measurement for cooking and baking. Urban health-conscious consumers particularly appreciate these soft, spreadable formats for their direct application on bread and crackers, combining convenience without compromising flavor.

Europe High Fat (>85%) Butter Market held a 34.3% share in 2024. This dominance is driven by the region's deep-rooted culinary heritage, where butter plays a vital role in traditional recipes and gourmet cooking. European consumers have a well-developed appreciation for high-quality dairy, prioritizing authenticity, rich flavor, and artisanal production methods. Additionally, widespread consumer education around premium and clean-label products fuels steady demand for high-fat butter across both retail and food service sectors. The presence of established dairy producers and a robust distribution network further strengthens Europe's position as a key player in this market, ensuring continuous availability of specialty butter products that meet the discerning tastes of its consumers.

Key players driving innovation and distribution in the High Fat (>85%) Butter Market include Ornua Co-operative Limited (Kerrygold), Arla Foods amba (Lurpak), Lactalis Group (President), Fonterra Co-operative Group (Anchor), and Gujarat Cooperative Milk Marketing Federation Ltd. (Amul). Danone S.A., Nestle S.A., The J.M. Smucker Company (Eagle Brand), Arla Foods, and Friesland Campina N.V. play influential roles in the condensed and evaporated milk segments.

To strengthen their market position, companies in the high-fat butter sector are prioritizing product innovation, focusing on clean-label and organic certifications to meet growing consumer demands for transparency and quality. They are expanding their flavor portfolios by introducing infused butter with herbs, spices, and probiotics to capture niche culinary and health-focused segments. Marketing efforts emphasize the authentic, artisanal nature of their products, connecting with consumers seeking premium, natural dairy options. Strategic partnerships with specialty retailers and online platforms enhance accessibility and consumer reach. Furthermore, investments in sustainable sourcing and production practices are improving brand reputation while aligning with environmental concerns. These combined strategies allow companies to build loyalty and tap into expanding global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 By fat content

- 5.2.1 85-90% fat content

- 5.2.2 90-95% fat content

- 5.2.3 95%+ fat content (Anhydrous Milk Fat/Butter Oil)

- 5.3 By flavor profile

- 5.3.1 Salted

- 5.3.2 Unsalted

- 5.3.3 Cultured/Fermented

- 5.3.4 Flavored & Infused

Chapter 6 Market Estimates and Forecast, By Form, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Block/Stick

- 6.3 Spreadable

- 6.4 Clarified/Ghee

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Source, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 Organic

- 7.4 Grass-Fed

- 7.5 Specialty animal sources

- 7.5.1 Buffalo

- 7.5.2 Goat

- 7.5.3 Sheep

- 7.5.4 Others

Chapter 8 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Blocks/Sticks

- 8.3 Tubs & Containers

- 8.4 Bulk packaging

- 8.5 Specialty & Gift packaging

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Supermarkets & Hypermarkets

- 9.3 Specialty & gourmet stores

- 9.4 Online retail

- 9.4.1 E-commerce platforms

- 9.4.2 Direct-to-consumer websites

- 9.4.3 Subscription services

- 9.5 Foodservice industry

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Culinary Applications

- 10.2.1 Cooking & Sauteing

- 10.2.2 Sauces & Emulsions

- 10.2.3 Other culinary uses

- 10.3 Baking & Confectionery

- 10.3.1 Pastries & laminated dough

- 10.3.2 Cakes & Cookies

- 10.3.3 Confectionery products

- 10.4 Spreads & toppings

- 10.4.1 Bread & toast

- 10.4.2 Crackers & savory items

- 10.4.3 Other spread applications

- 10.5 Dietary & nutritional applications

- 10.5.1 Ketogenic diet

- 10.5.2 Bulletproof coffee & beverages

- 10.5.3 Other dietary uses

- 10.6 Industrial applications

- 10.6.1 Food manufacturing

- 10.6.2 Cosmetics & personal care

- 10.6.3 Other industrial uses

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 Household/Retail consumers

- 11.3 Food service industry

- 11.3.1 Fine dining restaurants

- 11.3.2 Bakeries & patisseries

- 11.3.3 Hotels & catering

- 11.3.4 Other foodservice establishments

- 11.4 Food processing industry

- 11.4.1 Bakery & confectionery manufacturers

- 11.4.2 Ready meals & prepared foods

- 11.4.3 Other food processors

- 11.5 Others

Chapter 12 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 Saudi Arabia

- 12.6.2 South Africa

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Kerrygold (Ornua Co-operative Limited)

- 13.2 Lurpak (Arla Foods amba)

- 13.3 President (Lactalis Group)

- 13.4 Anchor (Fonterra Co-operative Group)

- 13.5 Amul (Gujarat Cooperative Milk Marketing Federation Ltd.)

- 13.6 Land O'Lakes, Inc.

- 13.7 Organic Valley

- 13.8 Straus Family Creamery

- 13.9 Vermont Creamery (Land O'Lakes, Inc.)

- 13.10 Isigny Sainte-Mere

- 13.11 Plugra (Dairy Farmers of America)

- 13.12 Valio Ltd.

- 13.13 Finlandia Cheese, Inc. (Valio Ltd.)

- 13.14 Meggle Group GmbH

- 13.15 Gourmet Food Holdings (Pepe Saya)