|

市场调查报告书

商品编码

1766216

汽车触觉回馈系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Haptic Feedback System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

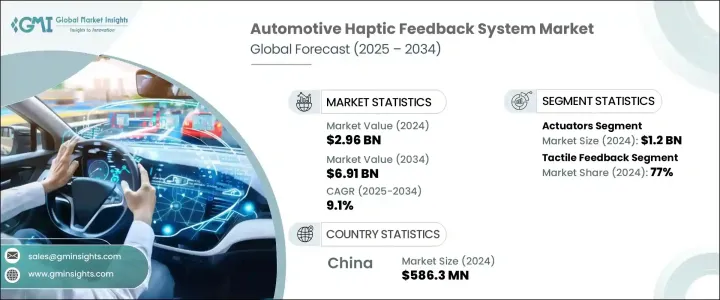

2024 年全球汽车触觉回馈系统市值为 29.6 亿美元,预计到 2034 年将以 9.1% 的复合年增长率成长,达到 69.1 亿美元。数位化趋势和高级驾驶辅助系统 (ADAS) 的兴起,扩大了触觉在各种汽车应用中的使用。製造商正在将复杂的触觉回馈整合到方向盘、触控萤幕和中控台中,以增强用户体验。对电动车和自动驾驶汽车日益增长的需求进一步加速了这种应用,因为这些汽车严重依赖先进的人机介面。消费者现在期望个人化、反应迅速的功能,促使汽车製造商投资于尖端的触觉解决方案。北美和欧洲引领这项技术的采用,而亚太地区预计将在汽车产量成长和技术娴熟的消费者的推动下实现最快成长。

政府法规和安全标准也强调减少驾驶分心并提高道路安全,从而推动了市场成长。触觉回馈系统会在紧急情况下(例如车道偏离或碰撞警告)提醒驾驶者,使他们能够专注于路况,而不会分散视线。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 29.6亿美元 |

| 预测值 | 69.1亿美元 |

| 复合年增长率 | 9.1% |

执行器细分市场在2024年以12亿美元的营收领先市场。执行器在方向盘、资讯娱乐显示器和触控萤幕中提供即时触觉响应、产生振动和触感方面发挥着至关重要的作用。随着高阶驾驶辅助系统和触控介面日益普及,对高性能执行器的需求也日益增长。这些组件能够提供快速、精准的回馈,透过在虚拟控制上复製实体按钮的触感,从而提升驾驶安全性和舒适性。随着连网汽车和自动驾驶汽车的兴起,对可靠且即时的触觉回馈的需求日益增长,这进一步巩固了执行器的市场主导地位。

2024年,触觉回馈细分市场占了77%的市占率。该技术利用细微的振动或脉衝来模拟资讯娱乐单元、触控萤幕和空调控制面板等表面的触感。基于触控的人机介面 (HMI) 透过提供直觉易用的控件,帮助驾驶者保持专注并减少分心。与模拟阻力且主要用于转向系统的力回馈相比,触觉回馈更具成本效益且更易于实现。电容式触控技术体积小巧、效率高且可靠性高,使其成为汽车製造商在虚拟按钮、换檔桿和座椅调整方面的热门选择。高端汽车对响应迅速且直观的用户介面的需求日益增长,极大地推动了触觉反馈市场份额的成长。

亚太地区汽车触觉回馈系统市场占54%的份额。中国以2024年5.863亿美元的估值领先该地区市场。中国的优势源于其强大的製造业基础、快速的汽车产量成长以及ADAS和资讯娱乐技术的广泛应用。中国、日本和韩国强劲的汽车产业为触觉系统在下一代汽车中的整合做出了贡献。中国在汽车创新领域的领导地位得益于政府的倡议、大量的研发投入以及消费者对连网汽车和电动车日益增长的需求。随着中国朝向智慧移动和自动驾驶方向发展,触觉回馈系统的应用正在加速推进。

活跃于汽车触觉回馈系统市场的主要参与者包括博世、德州仪器、ALPS Alpine、电装、大陆集团、松下汽车、Immersion、TDK、Aptiv 和 ZF Friedrichshafen。汽车触觉回馈系统市场中的公司专注于创新以维持和扩大其市场份额。他们在研发方面投入巨资,以开发更先进、更快回应、更节能的执行器和触觉回馈技术。与汽车製造商和科技公司的策略合作伙伴关係和合作有助于加速产品开发和与新车型的整合。透过合资企业扩大地理覆盖范围并建立本地製造中心,公司可以进入快速成长的地区,尤其是亚太地区。参与者强调创建可自订、可扩展的解决方案,以满足电动和自动驾驶汽车的多样化需求。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 对先进资讯娱乐和 HMI 系统的需求不断增长

- 注重驾驶员安全并减少干扰

- 消费者对高阶功能的偏好日益增加

- 触觉技术的技术进步

- 产业陷阱与挑战

- 整合成本高

- 系统设计和整合的复杂性

- 市场机会

- 转向基于触控的介面和简约的内饰

- 扩展安全和驾驶辅助应用

- 成长动力

- 成长潜力分析

- 监管格局

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利分析

- 价格趋势

- 按地区

- 按组件

- 生产统计

- 生产中心

- 消费中心

- 汇出和汇入

- 成本細項分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 执行器

- 控制器

- 软体

- 感应器

第六章:市场估计与预测:按回馈,2021 - 2034 年

- 主要趋势

- 触觉回馈

- 力回馈

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 商用车

- 轻型商用车

- 中型商用车

- 重型商用车

- 电动车(EV)

第八章:市场估计与预测:按销售管道,2021 - 2034 年

- 主要趋势

- 原始设备製造商

- 售后市场

第九章:市场估计与预测:依技术分类,2021 - 2034 年

- 主要趋势

- 机械触觉

- 超音波触觉

- 电磁触觉

- 电活性聚合物(EAP)

- 其他的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第 11 章:公司简介

- ALPS Alpine

- Analog Devices

- Aptiv

- Bosch

- Continental

- Denso

- Immersion

- Johnson Electric

- Methode Electronics

- Microchip Technology

- Neonode

- Nidec

- Panasonic Automotive

- Precision Microdrives

- Stanley Electric

- Synaptics

- TDK

- Texas Instruments

- Valeo

- ZF Friedrichshafen

The Global Automotive Haptic Feedback System Market was valued at USD 2.96 billion in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 6.91 billion by 2034. The rise of digital trends and advanced driver-assistance systems (ADAS) has expanded the use of haptics across various automotive applications. Manufacturers are integrating sophisticated haptic feedback into steering wheels, touchscreens, and center consoles to enhance user experience. The growing demand for electric and autonomous vehicles further accelerates this adoption, as these cars rely heavily on advanced human-machine interfaces. Consumers now expect personalized, responsive features, prompting automakers to invest in cutting-edge haptic solutions. North America and Europe lead the adoption of this technology, while the Asia-Pacific region is poised to grow the fastest, driven by increasing vehicle production and tech-savvy consumers.

Government regulations and safety standards also fuel market growth by emphasizing reduced driver distraction and improved road safety. Haptic feedback systems alert drivers during critical situations, such as lane departures or collision warnings, allowing them to stay focused on the road without diverting their gaze.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.96 Billion |

| Forecast Value | $6.91 Billion |

| CAGR | 9.1% |

The actuators segment led the market with revenues of USD 1.2 billion in 2024. Actuators play a crucial role in delivering real-time tactile responses, generating vibrations, and touch sensations in steering wheels, infotainment displays, and touchscreens. As advanced driver-assistance systems and touch interfaces become more prevalent, demand for high-performance actuators grows. These components provide fast, precise feedback that enhances driving safety and comfort by replicating the feel of physical buttons on virtual controls. With the rise of connected and autonomous vehicles, the need for reliable and instantaneous haptic feedback is increasing, solidifying actuators' dominant market position.

The tactile feedback segment accounted for a 77% share in 2024. This technology uses subtle vibrations or pulses to mimic touch sensations on surfaces like infotainment units, touchscreens, and climate control panels. Touch-based human-machine interfaces (HMIs) help drivers stay attentive and reduce distraction by offering intuitive and easy-to-use controls. Compared to force feedback, which simulates resistance and is mostly used in steering systems, tactile feedback is more cost-effective and simpler to implement. Its compact size, efficiency, and reliability make capacitive touch technology a popular choice among automakers for virtual buttons, gear selectors, and seat adjustments. The increasing demand for responsive and intuitive user interfaces in premium vehicles has significantly driven the market share of haptic feedback.

Asia-Pacific Automotive Haptic Feedback System Market held a 54% share. China leads this regional market with a valuation of USD 586.3 million in 2024. China's prominence stems from a robust manufacturing base, rapid vehicle production growth, and widespread adoption of ADAS and infotainment technologies. The strong automotive sectors in China, Japan, and South Korea contribute to the integration of haptic systems in next-generation vehicles. China's leadership in automotive innovation is supported by government initiatives, substantial R&D investments, and rising consumer demand for connected and electric vehicles. As the country pushes towards intelligent mobility and autonomous driving, haptic feedback systems are being adopted at an accelerated pace.

Key players active in the Automotive Haptic Feedback System Market include Bosch, Texas Instruments, ALPS Alpine, Denso, Continental, Panasonic Automotive, Immersion, TDK, Aptiv, and ZF Friedrichshafen. Companies in the automotive haptic feedback system market focus on innovation to maintain and grow their market share. They invest heavily in R&D to develop more advanced, responsive, and energy-efficient actuators and tactile feedback technologies. Strategic partnerships and collaborations with automakers and technology firms help accelerate product development and integration into new vehicle models. Expanding geographic reach through joint ventures and establishing local manufacturing hubs allows companies to tap into fast-growing regions, particularly in Asia-Pacific. Players emphasize creating customizable, scalable solutions to cater to the diverse needs of electric and autonomous vehicles.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for advanced infotainment and HMI systems

- 3.2.1.2 Focus on driver safety and reduction of distractions

- 3.2.1.3 Increasing consumer preference for premium features

- 3.2.1.4 Technological advancements in haptic technologies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of integration

- 3.2.2.2 Complexity in system design and integration

- 3.2.3 Market opportunities

- 3.2.3.1 Shift toward touch-based interfaces and minimalist interiors

- 3.2.3.2 Expansion of safety and driver assistance applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By component

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Actuators

- 5.3 Controllers

- 5.4 Software

- 5.5 Sensors

Chapter 6 Market Estimates & Forecast, By Feedback, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Tactile feedback

- 6.3 Force feedback

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles

- 7.3.2 Medium commercial vehicles

- 7.3.3 Heavy commercial vehicles

- 7.4 Electric vehicles (EVs)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Mechanical haptics

- 9.3 Ultrasonic haptics

- 9.4 Electromagnetic haptics

- 9.5 Electroactive polymers (EAP)

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 ALPS Alpine

- 11.2 Analog Devices

- 11.3 Aptiv

- 11.4 Bosch

- 11.5 Continental

- 11.6 Denso

- 11.7 Immersion

- 11.8 Johnson Electric

- 11.9 Methode Electronics

- 11.10 Microchip Technology

- 11.11 Neonode

- 11.12 Nidec

- 11.13 Panasonic Automotive

- 11.14 Precision Microdrives

- 11.15 Stanley Electric

- 11.16 Synaptics

- 11.17 TDK

- 11.18 Texas Instruments

- 11.19 Valeo

- 11.20 ZF Friedrichshafen

汽车触觉油门踏板市场规模、份额和成长分析(按技术类型、触觉回馈机制、车辆类型、销售管道和地区划分)—2026-2033年产业预测

汽车触觉油门踏板市场规模、份额和成长分析(按技术类型、触觉回馈机制、车辆类型、销售管道和地区划分)—2026-2033年产业预测 汽车踏板市场规模、份额和成长分析(按应用、车辆类型、材质、技术和地区划分)-2026-2033年产业预测

汽车踏板市场规模、份额和成长分析(按应用、车辆类型、材质、技术和地区划分)-2026-2033年产业预测 2032 年触觉回馈运动市场预测:按产品类型、技术、分销管道、应用、最终用户和地区进行的全球分析

2032 年触觉回馈运动市场预测:按产品类型、技术、分销管道、应用、最终用户和地区进行的全球分析 全球汽车踏板市场报告(2025年)全球汽车离合器踏板市场预测(至2032年):按车型、材料、传动类型、销售管道、技术和地区划分

全球汽车踏板市场报告(2025年)全球汽车离合器踏板市场预测(至2032年):按车型、材料、传动类型、销售管道、技术和地区划分 2025 年至 2033 年油门踏板模组市场报告,按踏板材料(塑胶、金属)、踏板类型(地板安装式、悬挂式)、车辆类型(乘用车、商用车)、最终用户(OEM、售后市场)和地区划分

2025 年至 2033 年油门踏板模组市场报告,按踏板材料(塑胶、金属)、踏板类型(地板安装式、悬挂式)、车辆类型(乘用车、商用车)、最终用户(OEM、售后市场)和地区划分 全球油门踏板模组市场

全球油门踏板模组市场 汽车用触觉油门踏板的全球市场规模:各产品,各用途,各地区,范围及预测全球汽车离合器踏板市场规模(按产品、应用、地区、范围和预测)

汽车用触觉油门踏板的全球市场规模:各产品,各用途,各地区,范围及预测全球汽车离合器踏板市场规模(按产品、应用、地区、范围和预测)