|

市场调查报告书

商品编码

1766219

导电聚合物(PEDOT、PANI)市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Conductive Polymers (PEDOT, PANI) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

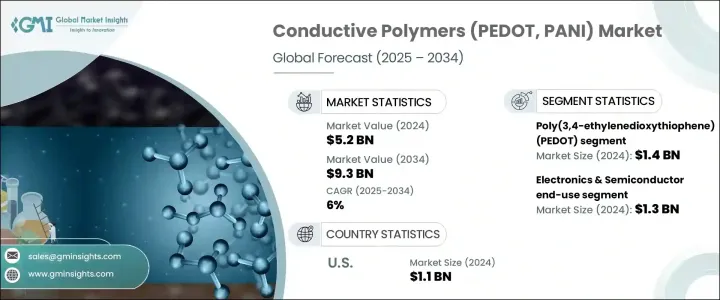

2024年,全球导电聚合物(PEDOT、PANI)市场规模达52亿美元,预计2034年将以6%的复合年增长率成长,达到93亿美元。市场扩张与基础设施建设、政府支出以及更广泛的工业产出密切相关,这些因素将继续作为宏观经济成长的催化剂。全球製造业和都市化的稳定发展,推动了导电材料需求的强劲成长。这些趋势与国际产业报告相符,显示全球需求不仅受资料和预测的影响,也受到更广泛的经济变化的影响。加工技术的持续进步降低了生产成本,并提高了效率,从而增强了市场竞争力。

同时,环境政策法规也推动了整个供应链的清洁生产实务和回收。这种转变正在为永续成长创造新的机会。新兴市场中产阶级的崛起进一步推动了电子、运输和储能解决方案的需求——所有这些都是关键的终端用户领域。儘管全球供应链挑战仍然存在,但适应性框架、自动化和技术创新正在推动市场在整个预测期内稳步成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 52亿美元 |

| 预测值 | 93亿美元 |

| 复合年增长率 | 6% |

聚苯胺 (PANI) 细分市场凭藉其在不同环境条件下适应性强的导电性和回弹性,在 2024 年创造了可观的收入。受工业和运输业活动成长的推动,该聚合物在防腐和感测器应用方面的需求年增长率约为 10%。展望未来,随着需求的成长,预计市场将保持这一上升趋势。其他类型的聚合物由于加工过程复杂且可扩展性有限,仍然面临限制。这表明,需要创新来提高其在大规模应用中的相容性、整合度和结构稳定性。

2024年,固有导电聚合物 (ICP) 市场规模达23亿美元,预计2034年将以6.1%的复合年增长率成长。导电聚合物复合材料(尤其是聚合物-金属和聚合物-碳复合材料)的使用日益增多,由于其增强的机械性能和导电性,正在推动需求成长。据报道,碳基复合材料的年需求量增加了20%,这主要得益于汽车和储能产业的应用。这些复合材料的强度来自其聚合物基质和导电填料,从而为下一代应用创造了用途广泛的材料。

德国导电聚合物(PEDOT、PANI)市场在2024年占据了相当大的份额,这得益于其高度重视永续聚合物复合材料与尖端製造製程的融合。绿色生产的推动与严格的环境政策一致。该地区导电聚合物的进口量年均成长12%,主要是为了满足汽车和航太製造商日益增长的需求。这凸显了当地产业正在转向先进的环保材料,以符合欧盟永续发展的要求。

主导全球导电聚合物(PEDOT、PANI)市场的关键参与者包括贺利氏控股和西格玛奥德里奇(隶属于其母公司默克集团),这两家公司都拥有强大的产品组合和稳固的市场影响力,为行业持续扩张做出了巨大贡献。在导电聚合物市场营运的公司正专注于创新、垂直整合和区域扩张相结合的方式,以巩固其市场地位。领先的公司正在投资研发,以改善聚合物加工方法、提高电气性能并开发符合不断发展的工业标准的复合材料。与最终用途产业(尤其是电子、汽车和储能领域)的合作使公司能够共同开发特定应用的材料。企业也正在加强其全球分销管道并确保原材料获取,以减少供应链的脆弱性。永续性是另一个重要的策略支柱,一些公司正在开发可回收聚合物并实施绿色製造技术。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 科技与创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计资料(HS 编码)(註:仅提供主要国家的贸易统计数据

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 - 2034 年

- 聚(3,4-乙撑二氧噻吩)(PEDOT)

- 聚苯胺(PANI)

- 聚吡咯(PPy)

- 聚噻吩(PTh)

- 其他导电聚合物

第六章:市场估计与预测:依传导机制,2021 - 2034 年

- 主要趋势

- 固有导电聚合物(ICP)

- 导电聚合物复合材料(CPC)

- 聚合物-碳复合材料

- 聚合物金属复合材料

- 其他复合材料

- 有机混合离子电子导体(OMIEC)

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 防静电包装

- 电容器

- 电池

- 感应器

- 有机发光二极体 (OLED)

- 太阳能电池

- 执行器

- 电致变色装置

- 电磁干扰(EMI)屏蔽

- 印刷电路板(PCB)

- 超级电容器

- 其他的

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 电子和半导体

- 活力

- 医疗保健和生物医学

- 汽车

- 航太与国防

- 纺织品和穿戴式设备

- 工业的

- 包装

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Agfa-Gevaert NV

- Celanese Corporation

- Merck KGaA

- Solvay SA

- 3M Company

- SABIC

- Covestro AG

- Henkel AG & Co. KGaA

- Heraeus Holding GmbH

- PolyOne Corporation (Avient Corporation)

- Rieke Metals, LLC

- RTP Company

- Lubrizol Corporation

- Asbury Carbons

- Sigma-Aldrich Corporation (Merck Group)

- Panipol Oy

- Polyone Corporation

- Premix Group

- Hyperion Catalysis International

- Ormecon GmbH

The Global Conductive Polymers (PEDOT, PANI) Market was valued at USD 5.2 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 9.3 billion by 2034. Market expansion is closely tied to infrastructure development, government spending, and broader industrial output, which continue to act as macroeconomic growth catalysts. The steady rise in global manufacturing and urbanization contributes to a robust demand curve for conductive materials. These trends align with international industry reports and illustrate how global demand, while influenced by data and projections, is also shaped by broader economic shifts. The continued progress in processing technologies has lowered production costs and boosted efficiency, driving market competitiveness.

At the same time, environmental policy regulations have prompted cleaner production practices and recycling across supply chains. This transition is creating new opportunities for sustainable growth. The rising middle class in emerging markets adds further momentum, boosting demand for electronics, transportation, and energy storage solutions-all key end-user sectors. While supply chain challenges persist globally, adaptive frameworks, automation, and technical innovation are enabling the market to grow steadily throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 billion |

| Forecast Value | $9.3 billion |

| CAGR | 6% |

The polyaniline (PANI) segment generated notable revenues in 2024 due to its adaptable conductivity and resilience under varying environmental conditions. The polymer has seen approximately 10% annual growth in demand from corrosion protection and sensor-based applications, driven by increased activity across industrial and transportation sectors. Looking ahead, the market is expected to maintain this upward trend as demand accelerates. Other polymer types still face constraints due to complex processing challenges and limited scalability. This points to a need for innovation to improve compatibility, integration, and structural stability in large-scale use.

In 2024, the inherently conductive polymers (ICPs) segment stood at USD 2.3 billion and is anticipated to grow at a 6.1% CAGR through 2034. The rising use of conductive polymer composites-especially Polymer-Metal and Polymer-Carbon combinations-is driving demand due to their enhanced mechanical performance and conductivity. Annual demand for carbon-based composites has reportedly grown by 20%, largely fueled by adoption in the automotive and energy storage industries. These composites gain strength from both their polymer matrices and conductive fillers, creating highly versatile materials for next-gen applications.

Germany Conductive Polymers (PEDOT, PANI) Market held a sizeable share in 2024, due to its strong focus on integrating sustainable polymer composites alongside cutting-edge manufacturing practices. The push toward greener production is aligned with strict environmental policies. Imports of conductive polymers into the region have seen a 12% annual increase, largely to meet the rising demand from automotive and aerospace manufacturers. This highlights how local industries are shifting toward advanced, eco-friendly materials in compliance with EU sustainability mandates.

Key players dominating the Global Conductive Polymers (PEDOT, PANI) Market include Heraeus Holding and Sigma-Aldrich (operating under its parent group, Merck), both of which possess strong product portfolios and established market influence that contribute significantly to ongoing industry expansion. Companies operating in the conductive polymers market are focusing on a mix of innovation, vertical integration, and regional expansion to reinforce their market presence. Leading firms are investing in R&D to advance polymer processing methods, enhance electrical properties, and develop composites that meet evolving industrial standards. Partnerships with end-use industries-especially in electronics, automotive, and energy storage-allow companies to co-develop application-specific materials. Firms are also strengthening their global distribution channels and securing raw material access to reduce supply chain vulnerabilities. Sustainability is another major strategic pillar, with several companies developing recyclable polymers and implementing green manufacturing techniques.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Conduction mechanism

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Poly(3,4-ethylenedioxythiophene) (PEDOT)

- 5.2 Polyaniline (PANI)

- 5.3 Polypyrrole (PPy)

- 5.4 Polythiophene (PTh)

- 5.5 Other conductive polymers

Chapter 6 Market Estimates & Forecast, By Conduction Mechanism, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Inherently conductive polymers (ICPs)

- 6.3 Conductive polymer composites (CPCs)

- 6.3.1 Polymer-carbon composites

- 6.3.2 Polymer-metal composites

- 6.3.3 Other composites

- 6.4 Organic mixed ionic-electronic conductors (OMIECs)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Anti-static packaging

- 7.3 Capacitors

- 7.4 Batteries

- 7.5 Sensors

- 7.6 Organic light-emitting diodes (OLEDs)

- 7.7 Solar cells

- 7.8 Actuators

- 7.9 Electrochromic devices

- 7.10 Electromagnetic interference (EMI) shielding

- 7.11 Printed circuit boards (PCBs)

- 7.12 Supercapacitors

- 7.13 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Electronics & semiconductor

- 8.3 Energy

- 8.4 Healthcare & biomedical

- 8.5 Automotive

- 8.6 Aerospace & defense

- 8.7 Textiles & wearables

- 8.8 Industrial

- 8.9 Packaging

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Agfa-Gevaert N.V.

- 10.2 Celanese Corporation

- 10.3 Merck KGaA

- 10.4 Solvay S.A.

- 10.5 3M Company

- 10.6 SABIC

- 10.7 Covestro AG

- 10.8 Henkel AG & Co. KGaA

- 10.9 Heraeus Holding GmbH

- 10.10 PolyOne Corporation (Avient Corporation)

- 10.11 Rieke Metals, LLC

- 10.12 RTP Company

- 10.13 Lubrizol Corporation

- 10.14 Asbury Carbons

- 10.15 Sigma-Aldrich Corporation (Merck Group)

- 10.16 Panipol Oy

- 10.17 Polyone Corporation

- 10.18 Premix Group

- 10.19 Hyperion Catalysis International

- 10.20 Ormecon GmbH

全球导电聚合物市场规模、份额、趋势和成长分析报告(2026-2034)

全球导电聚合物市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球导电聚合物市场报告

2026年全球导电聚合物市场报告 导电聚合物市场-全球产业规模、份额、趋势、机会及按类型、应用、地区和竞争格局分類的预测(2021-2031年)

导电聚合物市场-全球产业规模、份额、趋势、机会及按类型、应用、地区和竞争格局分類的预测(2021-2031年) 导电聚合物钽固体电容器市场(依最终用途产业、应用、容量、额定电压和封装划分),全球预测(2026-2032年)石墨聚四氟乙烯丝填料市场按材料类型、应用、终端用户产业、形式和销售管道划分-2026-2032年全球预测

导电聚合物钽固体电容器市场(依最终用途产业、应用、容量、额定电压和封装划分),全球预测(2026-2032年)石墨聚四氟乙烯丝填料市场按材料类型、应用、终端用户产业、形式和销售管道划分-2026-2032年全球预测 导电聚合物市场预测至2032年:按产品类型、导电机制、应用、最终用户和地区分類的全球分析

导电聚合物市场预测至2032年:按产品类型、导电机制、应用、最终用户和地区分類的全球分析 导电聚合物市场规模、份额及成长分析(按类型及地区划分)-2026-2033年产业预测

导电聚合物市场规模、份额及成长分析(按类型及地区划分)-2026-2033年产业预测 石墨烯增强导电聚合物市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)离子导电聚合物市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)

石墨烯增强导电聚合物市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)离子导电聚合物市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年) 2025年全球导电聚合物市场

2025年全球导电聚合物市场