|

市场调查报告书

商品编码

1766241

多西他赛市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Docetaxel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

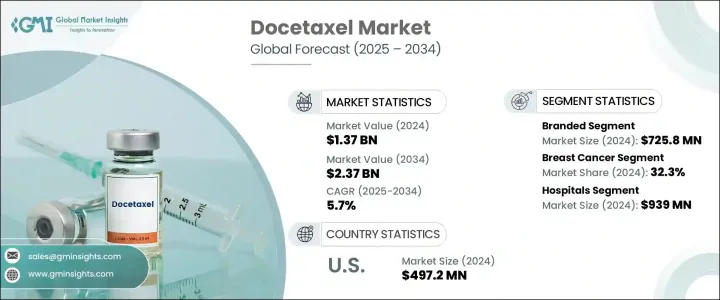

2024 年全球多西他赛市场价值为 13.7 亿美元,预计到 2034 年将以 5.7% 的复合年增长率增长至 23.7 亿美元。这一增长主要是由于乳腺癌、肺癌、前列腺癌和胃癌等多种癌症发病率不断上升所致,而多西他赛在这些疾病中被广泛使用。作为第二代紫杉烷,多西他赛可稳定微管并阻止癌细胞分裂,使其成为化疗方案的重要组成部分。它在联合疗法中尤其有效,有助于提高三阴性乳癌和去势抵抗性前列腺癌等晚期癌症患者的存活率。此外,奈米颗粒製剂和脂质体包覆等药物传递方法的创新提高了药物的生物利用度并降低了毒性,扩大了其临床应用。

生物相似药和多西他赛仿製药的核准数量不断增加,使得该药物更容易取得,尤其是在中低收入地区。同时,对肿瘤研发的日益关注也刺激了对这种重要细胞毒性药物的需求。数位医疗技术也发挥着重要作用,它可以透过远端监控治疗反应和副作用,实现更佳的个人化治疗。此外,癌症意识的提高、城市化进程的推进以及早期诊断的推进,也促进了人们对化疗和多西他赛等药物的更广泛依赖。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 13.7亿美元 |

| 预测值 | 23.7亿美元 |

| 复合年增长率 | 5.7% |

在多西他赛市场中,品牌药部分在2024年创造了7.258亿美元的收入,这得益于原厂药在临床上的良好声誉和疗效。儘管存在仿製药,但品牌药凭藉其可靠的安全性、监管部门的批准和高品质的标准,在已开发市场仍占据主导地位。品牌多西他赛通常是肿瘤学家治疗乳腺癌、非小细胞肺癌 (NSCLC) 和前列腺癌等复杂癌症的首选,尤其是在住院治疗中。此外,对新型给药方式和合併疗法的投入进一步提升了品牌价值。

2024年,乳癌领域占32.3%,主要得益于针对HER2阴性和三阴性乳癌患者的早期和晚期治疗方案。该药物常用于TAC(多西他赛、阿霉素和环磷酰胺)等联合治疗,这些方案已被证明可以改善存活结果。个人化肿瘤治疗系统的进展将继续增加对多西他赛在乳癌治疗的需求。

2024年,美国多西他赛市场规模达4.972亿美元。优惠的报销政策、日益增长的精准肿瘤学服务以及对个人化医疗的重视等因素正在推动市场需求。此外,门诊化疗可及性的扩大、癌症认知度的提高以及持续的临床研究也正在巩固美国市场的成长。製药公司与研究中心之间的战略合作伙伴关係进一步巩固了美国作为关键市场的地位,从而加速了药物开发和市场成长。

全球多西他赛产业的领导者包括 Alchem International、Alkem Labs、Arch Pharmalabs、Aspen Pharmacare、Cipla、Cisen Pharmaceutical、LGM Pharma、Phyton Biotech、齐鲁製药、Teva Active Pharmaceutical Ingredients (TAPI)、Teva Pharmaceuticals、Venus Remedies 和 Xiromed。在多西他赛市场运营的公司正致力于透过提供新配方、给药方式和联合疗法来扩展其产品组合。与研究机构和医院的合作对于加强多西他赛的临床应用和采用至关重要。许多参与者正在投资生物相似药和仿製药,以进入成本敏感市场,确保更广泛地获得这种基本药物。此外,个人化医疗和先进数位健康技术的发展使公司能够更好地满足患者需求,并改善治疗效果。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 全球癌症盛行率上升

- 越来越多地采用联合疗法

- 有利的监管批准和指导方针

- 药物配方技术进步

- 产业陷阱与挑战

- 严重的副作用和毒性问题

- 专利到期和仿製药竞争

- 市场机会

- 个人化肿瘤治疗方法的扩展

- 增加肿瘤学研发的投资

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 报销场景

- 报销政策对市场成长的影响

- 消费者行为分析

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 品牌

- 泛型

第六章:市场估计与预测:按适应症,2021 - 2034 年

- 主要趋势

- 乳癌

- 非小细胞肺癌(NSCLC)

- 荷尔蒙难治性前列腺癌

- 胃腺癌

- 头颈部鳞状细胞癌(HNSCC)

- 其他适应症

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 肿瘤诊所

- 其他最终用途

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Alchem International

- Alkem Labs

- Arch Pharmalabs

- Aspen Pharmacare

- Cipla

- Cisen Pharmaceutical

- LGM Pharma

- Phyton Biotech

- Qilu Pharmaceutical

- Teva Active Pharmaceutical Ingredients (TAPI)

- Teva Pharmaceuticals

- Venus Remedies

- Xiromed

The Global Docetaxel Market was valued at USD 1.37 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 2.37 billion by 2034. This growth is largely driven by the increasing incidence of various cancers, including breast, lung, prostate, and gastric cancers, where docetaxel is widely used. As a second-generation taxane, docetaxel stabilizes microtubules and halts the division of cancer cells, making it a crucial part of chemotherapy regimens. It is particularly effective in combination therapies, helping to improve survival rates for patients with advanced cancers, such as triple-negative breast cancer and castration-resistant prostate cancer. Additionally, innovations in drug delivery methods, such as nanoparticle formulations and liposomal encapsulations, have improved their bioavailability and reduced toxicity, expanding their clinical applications.

The growing approvals for biosimilars and generic docetaxel are making the drug more accessible, particularly in lower-middle-income regions, while the increasing focus on oncology R&D boosts demand for this essential cytotoxic agent. Digital health technologies also play a role by enabling better treatment personalization through remote monitoring of treatment responses and side effects. Furthermore, greater cancer awareness, urbanization, and early diagnosis efforts are contributing to the broader reliance on chemotherapy and drugs like docetaxel.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.37 Billion |

| Forecast Value | $2.37 Billion |

| CAGR | 5.7% |

The branded segment of the docetaxel market generated USD 725.8 million in 2024, benefiting from the established clinical reputation and efficacy of original formulations. Despite the presence of generics, branded products continue to dominate in developed markets due to their trusted safety profiles, regulatory approvals, and high-quality standards. Branded docetaxel is often preferred by oncologists for treating complex cancers such as breast cancer, non-small cell lung cancer (NSCLC), and prostate cancer, particularly in hospital settings. Moreover, the investment in new delivery methods and combination therapies further strengthens the brand's value.

In 2024, breast cancer segment held 32.3% driven by early and advanced treatment regimens for HER2-negative and triple-negative breast cancer patients. It is commonly used in combination treatments like TAC (docetaxel, doxorubicin, and cyclophosphamide), which have been shown to improve survival outcomes. Advances in personalized oncology systems continue to increase the demand for docetaxel in managing breast cancer cases.

U.S. Docetaxel Market was valued at USD 497.2 million in 2024. Factors such as favorable reimbursement policies, growing precision oncology services, and a focus on personalized medicine are fueling the demand. Furthermore, the expansion of outpatient chemotherapy access, increasing cancer awareness, and continuous clinical research are reinforcing the U.S. market's growth. The role of the U.S. as a key market is further strengthened by strategic partnerships between pharmaceutical companies and research centers, which accelerate drug development and market growth.

Leading players in the Global Docetaxel Industry include Alchem International, Alkem Labs, Arch Pharmalabs, Aspen Pharmacare, Cipla, Cisen Pharmaceutical, LGM Pharma, Phyton Biotech, Qilu Pharmaceutical, Teva Active Pharmaceutical Ingredients (TAPI), Teva Pharmaceuticals, Venus Remedies, and Xiromed. Companies operating in the docetaxel market are focusing on expanding their product portfolios by offering new formulations, delivery methods, and combination therapies. Partnerships with research institutions and hospitals are vital to enhancing the clinical applications and adoption of docetaxel. Many players are investing in biosimilars and generics to tap into cost-sensitive markets, ensuring broader access to this essential drug. Additionally, the development of personalized medicine and advanced digital health technologies allows companies to better cater to patient needs, improving treatment outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Indication

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global cancer prevalence

- 3.2.1.2 Increasing adoption of combination therapies

- 3.2.1.3 Favorable regulatory approvals and guidelines

- 3.2.1.4 Technological advancements in drug formulation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Severe side effects and toxicity concerns

- 3.2.2.2 Patent expirations and generic competition

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of personalized oncology treatment approaches

- 3.2.3.2 Increasing investments in oncology research and development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Reimbursement scenario

- 3.10.1 Impact of reimbursement policies on market growth

- 3.11 Consumer behaviour analysis

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded

- 5.3 Generics

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Breast cancer

- 6.3 Non-small cell lung cancer (NSCLC)

- 6.4 Hormone refractory prostate cancer

- 6.5 Gastric adenocarcinoma

- 6.6 Head and neck squamous cell carcinoma (HNSCC)

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Oncology clinics

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alchem International

- 9.2 Alkem Labs

- 9.3 Arch Pharmalabs

- 9.4 Aspen Pharmacare

- 9.5 Cipla

- 9.6 Cisen Pharmaceutical

- 9.7 LGM Pharma

- 9.8 Phyton Biotech

- 9.9 Qilu Pharmaceutical

- 9.10 Teva Active Pharmaceutical Ingredients (TAPI)

- 9.11 Teva Pharmaceuticals

- 9.12 Venus Remedies

- 9.13 Xiromed

全球抗癌药物市场规模、份额、趋势和成长分析报告(2026-2034年)

全球抗癌药物市场规模、份额、趋势和成长分析报告(2026-2034年) 半导体超高纯度波纹管阀市场按材料、驱动类型、流量和应用划分,全球预测(2026-2032)

半导体超高纯度波纹管阀市场按材料、驱动类型、流量和应用划分,全球预测(2026-2032) 抗癌药物市场-全球产业规模、份额、趋势、机会和预测,按适应症、药物、给药途径、最终用户、地区和竞争格局划分,2020-2030年预测

抗癌药物市场-全球产业规模、份额、趋势、机会和预测,按适应症、药物、给药途径、最终用户、地区和竞争格局划分,2020-2030年预测 抗癌药物市场:依给药途径、药物类别、适应症、通路、剂型、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测

抗癌药物市场:依给药途径、药物类别、适应症、通路、剂型、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测 非洲抗癌药物市场规模及预测(2021 - 2031 年)、区域份额、趋势及成长机会分析报告,涵盖:依药物类别、适应症、剂型、疗法、产业及国家/地区

非洲抗癌药物市场规模及预测(2021 - 2031 年)、区域份额、趋势及成长机会分析报告,涵盖:依药物类别、适应症、剂型、疗法、产业及国家/地区 多西他赛市场规模、份额、趋势分析报告:按适应症、分销管道、地区、细分市场预测,2025-2030 年

多西他赛市场规模、份额、趋势分析报告:按适应症、分销管道、地区、细分市场预测,2025-2030 年 铂类抗癌药物市场规模、占有率、趋势、行业分析报告(按类型、应用、分销管道和地区)- 市场预测,2025-2034 年计时疗法服务市场,按产品类型、治疗领域、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测全球抗癌药物市场规模(按产品、应用、地区、范围和预测)

铂类抗癌药物市场规模、占有率、趋势、行业分析报告(按类型、应用、分销管道和地区)- 市场预测,2025-2034 年计时疗法服务市场,按产品类型、治疗领域、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测全球抗癌药物市场规模(按产品、应用、地区、范围和预测) 计时疗法服务市场 - 2024-2034 年全球产业分析、规模、份额、成长、趋势和预测

计时疗法服务市场 - 2024-2034 年全球产业分析、规模、份额、成长、趋势和预测