|

市场调查报告书

商品编码

1766295

人类微生物组市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Human Microbiome Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

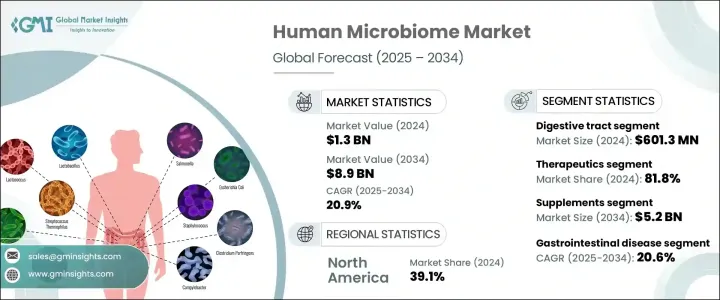

2024年,全球人体微生物组市场规模达13亿美元,预计2034年将以20.9%的复合年增长率成长,达到89亿美元。市场扩张的动力主要源自于全球日益认识到微生物组在维持人类健康和预防疾病的关键作用。人体内的微生物群落现已被公认为各种生物过程的基础,包括消化、免疫,甚至神经平衡。随着新的科学突破揭示了这些微生物如何影响整体健康,对基于微生物组的产品的需求正在加速成长。

人们对人类微生物组日益增长的兴趣正在改变医疗保健模式。一个关键驱动因素是精准医疗的兴起,精准医疗依赖于根据患者独特的微生物组特征量身定制治疗方案。这种个人化方法使基于微生物组的诊断和治疗更加有效,并推动了其应用范围的扩大。对标靶治疗的需求正推动製药公司、生物技术公司和研究机构之间的合作,进一步推动创新和商业成长。定序技术和生物资讯学的进步也提高了微生物组绘图能力,促进了新型治疗方案的开发,并使数据驱动的药物开发和疾病预防方法成为可能。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 13亿美元 |

| 预测值 | 89亿美元 |

| 复合年增长率 | 20.9% |

在研究的各类微生物组应用解剖部位中,消化道占据了相当大的份额,2024 年的市值为 6.013 亿美元。由于肠道中微生物的高密度和多样性,消化道将继续占据主导地位。这些肠道微生物在消化功能管理、新陈代谢调节、免疫功能支持和抵抗有害病原体方面发挥重要作用。肠道微生物组与代谢紊乱、自体免疫疾病和神经退化性疾病等慢性健康状况密切相关,使其成为持续研究和产品开发的重点。人们对肠道健康的广泛关注,催生了益生菌、益生元、后生元和基于微生物组的疗法等针对性解决方案的推出。

在应用方面,市场细分为治疗和诊断,其中治疗在2024年占据主导地位,占据81.8%的市场。这种主导地位归因于越来越多的健康状况与微生物组紊乱有关,包括代谢症候群、胃肠道疾病和神经系统疾病。活体生物治疗产品、基于微生物组的移植以及微生物组调节药物等创新正在加强这一领域。随着越来越多的医疗保健提供者根据个别微生物组特征采用个人化治疗,微生物组产品的治疗价值不断提升,为各种疾病提供量身定制且更有效率的解决方案。

依疾病类型,市场可分为胃肠道疾病、内分泌及代谢性疾病、传染病、癌症、中枢神经系统疾病等。预计胃肠道疾病领域在预测期内的复合年增长率将达到20.6%。肠道菌群紊乱与肠躁症、溃疡性结肠炎和克隆氏症等疾病的关联性日益增强。由于针对微生物组的干预措施提供了侵入性更低、针对性更强的治疗方案,因此对此类干预措施的需求正在增长。患者对恢復菌丛平衡的解决方案的偏好日益增长,预计将显着促进该领域的扩张。

按产品类型评估,市场包括药品、补充剂、诊断测试和其他产品。补充剂类别在2024年占据市场主导地位,预计2034年将达到52亿美元。这种主导地位源于人们对预防保健和健康日益增长的兴趣,这促使消费者转向支持肠道和免疫健康的非处方选择。益生菌和益生元补充剂易于取得且被广泛接受,这促进了其消费的成长。此外,随着消费者寻求量身定制的健康解决方案,包括合生元和个人化补充剂混合物在内的定製配方的出现,进一步刺激了这一领域的需求。

从区域来看,北美在2024年占据39.1%的市场份额,占据市场主导地位。光是美国市场就从2023年的4.002亿美元成长到2024年的4.766亿美元。高昂的医疗支出、不断上升的慢性病发病率以及强大的研究基础设施支撑了这一区域主导地位。监管机构的支持和领先市场参与者的存在进一步加速了其在临床和商业应用中的普及。

阿彻丹尼尔斯米德兰公司 (Archer Daniels Midland Company)、辉凌公司 (Ferring) 和 Seres Therapeutics, Inc. 等主要参与者合计占据全球约 40% 的市场份额。这些公司正在积极推行策略联盟、合併和研究合作等策略,以扩大其业务范围,进入新市场,并在不断发展的微生物组格局中增强其竞争地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 生活方式相关疾病负担加重,老年人口不断增加

- 增加资助计划和政府项目

- 精准医疗需求不断成长

- 产业陷阱与挑战

- 监理途径长,开发成本高

- 道德和安全问题

- 市场机会

- 扩大治疗应用

- 益生菌和益生元产品的需求不断增长

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 当前的技术趋势

- 新兴技术

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按站点,2021 - 2034 年

- 主要趋势

- 消化道

- 肺

- 生殖腔

- 皮肤

- 其他网站

第六章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 疗法

- 诊断

第七章:市场估计与预测:按疾病,2021 - 2034 年

- 主要趋势

- 传染病

- 胃肠道疾病

- 内分泌代谢疾病

- 癌症

- 中枢神经系统 (CNS) 疾病

- 其他疾病

第八章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 药物

- 补充品

- 益生菌

- 益生元

- 合生元

- 诊断测试

- 其他产品

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东和非洲

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Archer Daniels Midland Company

- Biohm Technologies

- BioGaia

- Biome Diagnostics

- BiomeBank

- Ferring

- Intralytix

- OptiBiotix

- Pendulum Therapeutics

- Prescient Metabiomics

- Seres Therapeutics

- Seed Health

- The BioArte

- Vedanta Biosciences

- Viome Life Sciences

The Global Human Microbiome Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 20.9% to reach USD 8.9 billion by 2034. Market expansion is largely fueled by the increasing global awareness about the critical role of microbiomes in maintaining human health and preventing disease. Microbial communities in the human body are now recognized as fundamental to various biological processes, including digestion, immunity, and even neurological balance. With new scientific breakthroughs uncovering how these microbes influence overall health, demand for microbiome-based products is accelerating.

Growing interest in the human microbiome is transforming the healthcare landscape. A key driver is the rising shift toward precision medicine, which relies on tailoring treatments to a patient's unique microbial profile. This personalization approach is making microbiome-based diagnostics and therapeutics more effective, driving increased adoption. The demand for targeted therapies is encouraging collaborations between pharmaceutical firms, biotech companies, and research institutes, further fueling innovation and commercial growth. Advancements in sequencing technologies and bioinformatics are also improving microbiome mapping capabilities, encouraging the development of novel treatment solutions, and enabling a data-driven approach to drug development and disease prevention.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $8.9 Billion |

| CAGR | 20.9% |

Among the various anatomical sites studied for microbiome applications, the digestive tract segment held a substantial share, with a market value of USD 601.3 million in 2024. This segment continues to dominate due to the high density and diversity of microbes found in the gut. These gut microorganisms are instrumental in managing digestion, regulating metabolism, supporting immune function, and defending against harmful pathogens. The gut microbiome's involvement in chronic health conditions such as metabolic disorders, autoimmune diseases, and neurodegenerative issues has positioned it as a central focus for ongoing research and product development. The widespread interest in gut health has led to the launch of targeted solutions like probiotics, prebiotics, postbiotics, and microbiome-based therapeutics.

In terms of application, the market is segmented into therapeutics and diagnostics, with therapeutics taking the lead in 2024 by capturing an 81.8% share. This dominance is attributed to the increasing number of health conditions now linked to disruptions in the microbiome, including metabolic syndromes, gastrointestinal diseases, and neurological disorders. Innovations such as live biotherapeutic products, microbiota-based transplants, and microbiome-modulating drugs are strengthening this segment. As more healthcare providers adopt personalized treatments based on individual microbiome profiles, the therapeutic value of microbiome products continues to expand, offering tailored and more efficient solutions across various diseases.

By disease type, the market is categorized into gastrointestinal disease, endocrine and metabolic diseases, infectious disease, cancer, central nervous system disorder, and others. The gastrointestinal disease segment is projected to grow at a CAGR of 20.6% over the forecast period. Disruptions in the gut microbiota are increasingly associated with conditions like irritable bowel syndrome, ulcerative colitis, and Crohn's disease. The demand for microbiome-targeted interventions is rising as these therapies offer less invasive and more focused treatment alternatives. Growing patient preference for solutions that restore microbiota balance is expected to significantly contribute to the expansion of this segment.

When evaluated by product type, the market includes drugs, supplements, diagnostic tests, and other offerings. The supplements category led the market in 2024 and is forecasted to reach USD 5.2 billion by 2034. This dominance stems from rising interest in preventive care and wellness, which is pushing consumers toward non-prescription options that support gut and immune health. Probiotic and prebiotic supplements are readily available and widely accepted, contributing to their growing consumption. Additionally, the emergence of customized formulations, including synbiotics and personalized supplement blends, is further boosting demand in this segment as consumers seek tailored health solutions.

Regionally, North America led the market with a commanding share of 39.1% in 2024. The U.S. market alone grew from USD 400.2 million in 2023 to USD 476.6 million in 2024. This regional dominance is supported by high healthcare spending, rising incidences of chronic illnesses, and strong research infrastructure. Regulatory backing and the presence of leading market players have further accelerated adoption across clinical and commercial applications.

Key participants such as Archer Daniels Midland Company, Ferring, and Seres Therapeutics, Inc. collectively account for around 40% of the global market share. These companies are actively pursuing strategies such as strategic alliances, mergers, and research collaborations to expand their footprint, gain access to new markets, and enhance their competitive positioning in the evolving microbiome landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Site

- 2.2.3 Application

- 2.2.4 Disease

- 2.2.5 Product

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing burden of lifestyle-related diseases and the growing geriatric population

- 3.2.1.2 Increasing funding initiatives and government programs

- 3.2.1.3 Increasing demand for precision medicine

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Long regulatory pathways and high development costs

- 3.2.2.2 Ethical and safety concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding therapeutic applications

- 3.2.3.2 Growing demand for probiotic and prebiotic products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Site, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Digestive tract

- 5.3 Lung

- 5.4 Reproductive cavity

- 5.5 Skin

- 5.6 Other sites

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Therapeutics

- 6.3 Diagnostics

Chapter 7 Market Estimates and Forecast, By Disease, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Infectious diseases

- 7.3 Gastrointestinal diseases

- 7.4 Endocrine and metabolic diseases

- 7.5 Cancer

- 7.6 Central nervous system (CNS) disorder

- 7.7 Other diseases

Chapter 8 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Drugs

- 8.3 Supplements

- 8.3.1 Probiotics

- 8.3.2 Prebiotics

- 8.3.3 Synbiotics

- 8.4 Diagnostic tests

- 8.5 Other products

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Archer Daniels Midland Company

- 10.2 Biohm Technologies

- 10.3 BioGaia

- 10.4 Biome Diagnostics

- 10.5 BiomeBank

- 10.6 Ferring

- 10.7 Intralytix

- 10.8 OptiBiotix

- 10.9 Pendulum Therapeutics

- 10.10 Prescient Metabiomics

- 10.11 Seres Therapeutics

- 10.12 Seed Health

- 10.13 The BioArte

- 10.14 Vedanta Biosciences

- 10.15 Viome Life Sciences

人类微生物组市场:按类型、部位、应用和最终用户划分-2026-2032年全球市场预测

人类微生物组市场:按类型、部位、应用和最终用户划分-2026-2032年全球市场预测 人类微生物组市场(第五版):产业趋势及全球预测(至 2035 年)-依产品类型、生物製剂类型、给药途径、药物製剂、目标适应症、目标治疗领域及地区划分

人类微生物组市场(第五版):产业趋势及全球预测(至 2035 年)-依产品类型、生物製剂类型、给药途径、药物製剂、目标适应症、目标治疗领域及地区划分 日本人类微生物组市场报告(按产品、应用、疾病类型和地区划分,2026-2034年)

日本人类微生物组市场报告(按产品、应用、疾病类型和地区划分,2026-2034年) 人类微生物组市场规模、份额和成长分析(按产品、疾病、类型、最终用户和地区划分)—2026-2033年产业预测2025 年至 2033 年人类微生物组市场规模、份额、趋势及预测(依产品、应用、疾病类型及地区)

人类微生物组市场规模、份额和成长分析(按产品、疾病、类型、最终用户和地区划分)—2026-2033年产业预测2025 年至 2033 年人类微生物组市场规模、份额、趋势及预测(依产品、应用、疾病类型及地区) 2021-2031年亚太地区人类微生物组市场报告:范围、细分、动态和竞争分析

2021-2031年亚太地区人类微生物组市场报告:范围、细分、动态和竞争分析 全球人体微生物组市场(按产品、类型、疾病、给药途径、服务、最终用户和地区划分)- 预测至 2031 年

全球人体微生物组市场(按产品、类型、疾病、给药途径、服务、最终用户和地区划分)- 预测至 2031 年 人类微生物组市场-全球产业规模、份额、趋势、机会和预测,按产品、应用、疾病、技术、类型、地区和竞争细分,2020-2030 年

人类微生物组市场-全球产业规模、份额、趋势、机会和预测,按产品、应用、疾病、技术、类型、地区和竞争细分,2020-2030 年 人体微生物组市场,按产品、按疾病、按类型、按给药途径、按最终用户、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

人体微生物组市场,按产品、按疾病、按类型、按给药途径、按最终用户、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测 人类微生物组市场:2025-2030 年预测

人类微生物组市场:2025-2030 年预测