|

市场调查报告书

商品编码

1766328

医疗冷链储存设备市场机会、成长动力、产业趋势分析及2025-2034年预测Medical Cold Chain Storage Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

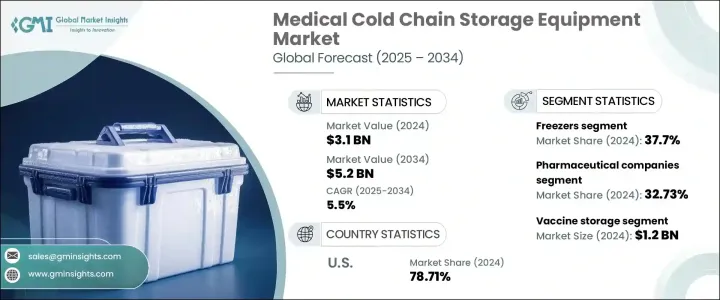

2024年,全球医疗冷链储存设备市场规模达31亿美元,预计到2034年将以5.5%的复合年增长率成长,达到52亿美元。由于敏感医药产品对温控物流的依赖日益增加,该市场正呈现强劲成长动能。随着全球医疗保健供应链日益复杂,对可靠、安全、高效的冷链解决方案的需求持续成长。生物製剂、细胞疗法和疫苗等药品需要恆定的低温环境,以确保其在运输和储存过程中的功效和安全性。世界各地的监管机构也正在执行更严格的温控准则,这推动了高性能冷冻系统的普及。

随着供应链挑战日益严峻,产业参与者正在整合先进技术,包括温度指示器、智慧感测器和即时资料记录器,以确保整个冷链的品质。此外,智慧製冷系统、自动化工具和环保冷媒的应用正在成为行业标准,使企业能够同时满足全球永续发展的要求和环境法规的要求。远端监控、物联网功能和预测分析的整合极大地提高了冷链管理的营运透明度和绩效。持续的数位基础设施投资,加上国际免疫接种计画和救命疗法的普及,进一步加速了各个医疗保健领域对医疗冷藏系统的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 31亿美元 |

| 预测值 | 52亿美元 |

| 复合年增长率 | 5.5% |

就产品类型而言,冷冻柜在 2024 年引领全球市场,占总营收的 37.7%,预计 2025 年至 2034 年的复合年增长率为 6%。其日益增长的使用是由于需要在特定的低温下储存疫苗、药物和实验室样本等关键医疗保健产品。这些系统因其稳定性和在不同环境条件下高效运作的能力而受到广泛认可。符合行业法规的要求也支持了这一需求,因为配备精确温度控制和警报机制的冷冻柜被认为是医疗物流中必不可少的。它们能够适应不同容量的处理,适用于不同的环境,包括医院、製药厂和诊断实验室。双隔间和节能设计等多功能特性也促使它们广受欢迎。

根据最终用户分析,製药公司在2024年占据了32.73%的市场份额,预计到2034年将以5.8%的复合年增长率扩张。这些公司在严格的温度要求下储存和运输疫苗、生物製剂和临床研究材料。遵守国际温度控制标准至关重要,尤其是在处理敏感或实验性化合物时。保持不间断的冷链对于产品活力和保质期至关重要。随着产量的增加,製药公司需要可扩展且合规的储存系统,以降低产品变质风险并优化库存管理。这些功能不仅有助于满足监管要求,还能提高营运效率,从而鼓励对先进冷藏设备的进一步投资。

在应用方面,疫苗储存在2024年占据全球市场主导地位,创造了12亿美元的收入。预计2025年至2034年期间的复合年增长率将达到5.8%。疫苗必须在较窄的温度范围内储存才能保持其效力,因此专用的冷链系统至关重要。全球为提高疫苗接种的可及性和提高疫苗接种意识所做的努力持续推动了对疫苗储存设备的需求。即时监控技术与高效能冷冻设备结合,可确保在运输和储存过程中始终保持一致的温度控制。由于疫苗在公共卫生中发挥着至关重要的作用,这一应用领域仍然是医疗冷链产业的基石。

从地区来看,美国在2024年引领全球市场,占北美总份额的78.71%,营收达8亿美元。美国受惠于强大的医疗基础设施和高度监管的医药物流环境。对创新储存技术和端到端供应链视觉化工具的投资,使美国在冷链管理领域处于领先地位。此外,大型医疗物流供应商的存在以及製药厂的高度集中,也有助于巩固其在该地区的优势地位。美国机构的严格监管也促使企业部署先进的冷藏系统,以提供能源效率和即时合规追踪。

全球医疗冷链储存设备市场的主要公司包括Binder、Azenta、Cardinal Health、Darwin Chambers、Carebios Biological Technology、Elanpro、海尔生物医疗、Farrar、Hoshizaki America、Memmert、Philipp Kirsch、Kendall Cold Chain System、Summit Appliances、Rommert、Philipp Kirsch、Kendall Cold Chain System、Summit Appliances、Roemer Kuhlung。这些公司持续投资于产品创新和数位解决方案,以满足不断变化的市场需求并保持竞争优势。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 生物製剂和疫苗需求不断成长

- 严格遵守法规

- 技术进步

- 产业陷阱与挑战

- 初始资本投入高

- 新兴市场的基础建设差距

- 机会

- 成长动力

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依设备类型

- 监理框架

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 贸易统计(84186990)

- 主要进口国

- 主要出口国

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按设备类型,2021 - 2034 年(十亿美元)

- 冰箱

- 实验室冰箱

- 血库冰箱

- 药房冰箱

- 色谱冰箱

- 冷冻机

- 超低温冷冻机

- 血浆冷冻机

- 速冻机

- 低温储存系统

- 液态氮储存系统

- 气相储存系统

- 冷藏室

- 其他的

第六章:市场估计与预测:依温度范围,2021 年至 2034 年(十亿美元)

- 2°C 至 8°C

- -20°C 至 -40°C

- -40°C 至 -80°C

- 低于-80°C

第七章:市场估计与预测:按产能,2021 - 2034 年(十亿美元)

- 小型(最多 300 公升)

- 中型(300-700公升)

- 大型(700公升以上)

第八章:市场估计与预测:按技术分类,2021 - 2034 年(十亿美元)

- 基于压缩机的系统

- 基于吸收的系统

- 基于热电的系统

第九章:市场估计与预测:按应用,2021 - 2034 年(十亿美元)

- 主要趋势

- 疫苗储存

- 血液及血液製品储存

- 生物样本储存

- 药品和药物储存

- 其他的

第 10 章:市场估计与预测:按最终用途,2021 年至 2034 年(十亿美元)

- 主要趋势

- 医院和诊所

- 製药公司

- 研究实验室

- 血库

- 药局

- 其他的

第 11 章:市场估计与预测:按地区,2021 年至 2034 年(十亿美元)

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十二章:公司简介

- Azenta Inc.

- Binder

- Cardinal Health

- Carebios Biological Technology

- Darwin Chambers

- Elanpro

- Farrar

- Haier Biomedical

- Hoshizaki America

- Kendall Cold Chain System

- Memmert

- Philipp Kirsch

- Roemer Industries

- Summit Appliances

- Thalheimer Kuhlung

The Global Medical Cold Chain Storage Equipment Market was valued at USD 3.1 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 5.2 billion by 2034. The market is witnessing significant momentum due to the growing reliance on temperature-controlled logistics for sensitive pharmaceutical products. As global healthcare supply chains become more complex, the demand for reliable, secure, and efficient cold chain solutions continues to rise. Pharmaceuticals such as biologics, cell therapies, and vaccines require consistent low-temperature environments to maintain efficacy and safety throughout transportation and storage. Regulatory agencies worldwide are also enforcing stricter temperature-control guidelines, which drives the adoption of high-performance refrigeration systems.

With increasing supply chain challenges, industry participants are integrating advanced technologies, including temperature indicators, intelligent sensors, and real-time data loggers, to ensure quality assurance across the entire cold chain. Furthermore, the adoption of smart cooling systems, automation tools, and eco-conscious refrigerants is becoming a standard, enabling companies to align with global sustainability mandates while remaining compliant with environmental regulations. The integration of remote monitoring, IoT capabilities, and predictive analytics has greatly enhanced operational transparency and performance in cold chain management. The ongoing investment in digital infrastructure, combined with international immunization initiatives and expanded access to life-saving treatments, is further accelerating the need for medical cold storage systems across various healthcare segments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 5.5% |

In terms of product type, freezers led the global market in 2024, accounting for 37.7% of total revenue, and are projected to register a CAGR of 6% from 2025 to 2034. Their growing use is driven by the need to store critical healthcare products such as vaccines, drugs, and laboratory samples at specific low temperatures. These systems are widely regarded for their stability and ability to function efficiently under diverse environmental conditions. The demand is also supported by the need for compliance with industry regulations, as freezers equipped with accurate temperature controls and alarm mechanisms are considered essential in medical logistics. Their adaptability in handling varying volumes makes them suitable for use in different environments, including hospitals, pharmaceutical manufacturing units, and diagnostic laboratories. Multipurpose features such as dual compartments and energy-efficient designs also contribute to their widespread preference.

Based on end-user analysis, pharmaceutical companies held a 32.73% share of the market in 2024 and are anticipated to expand at a CAGR of 5.8% through 2034. These companies operate under strict temperature requirements to store and transport vaccines, biologics, and clinical research materials. Adherence to international standards for temperature control is non-negotiable, especially when dealing with sensitive or experimental compounds. Maintaining an uninterrupted cold chain is critical for product viability and shelf life. As production volumes increase, pharmaceutical firms require scalable and compliant storage systems that reduce the risk of spoilage and optimize inventory management. These capabilities not only help in meeting regulatory requirements but also enhance operational efficiency, encouraging further investment in advanced cold storage equipment.

In terms of applications, vaccine storage dominated the global market in 2024, generating USD 1.2 billion in revenue. It is expected to grow at a CAGR of 5.8% from 2025 to 2034. Vaccines must be stored within a narrow temperature range to retain their potency, making dedicated cold chain systems essential. Global efforts to improve vaccination access and awareness continue to boost demand for vaccine storage equipment. Real-time monitoring technologies, coupled with high-performance refrigeration units, ensure consistent temperature control during transit and storage. This application segment remains a cornerstone of the medical cold chain industry due to the critical role vaccines play in public health.

Regionally, the United States led the global market in 2024, accounting for 78.71% of North America's total share, with revenue reaching USD 800 million. The country benefits from a robust healthcare infrastructure and a highly regulated pharmaceutical logistics environment. Investments in innovative storage technologies and end-to-end supply chain visibility tools have made the US a leader in cold chain management. Additionally, the presence of major healthcare logistics providers and a high concentration of pharmaceutical manufacturing facilities contribute to regional dominance. Stringent regulations from US agencies have also pushed companies to deploy advanced cold storage systems that offer energy efficiency and real-time compliance tracking.

Key companies operating in the global medical cold chain storage equipment market include Binder, Azenta, Cardinal Health, Darwin Chambers, Carebios Biological Technology, Elanpro, Haier Biomedical, Farrar, Hoshizaki America, Memmert, Philipp Kirsch, Kendall Cold Chain System, Summit Appliances, Roemer Industries, and Thalheimer Kuhlung. These players continue to invest in product innovation and digital solutions to meet evolving market demands and maintain a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collections methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 By region

- 2.2.2 By equipment type

- 2.2.3 By temperature range

- 2.2.4 By capacity

- 2.2.5 By technology

- 2.2.6 By application

- 2.2.7 By end use

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for biologics and vaccines

- 3.2.1.2 Stringent regulatory compliance

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Infrastructure gaps in emerging markets

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Equipment type

- 3.7 Regulatory framework

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (84186990)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger & acquisitions

- 4.6.2 Partnership & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021 - 2034 ($Bn) (Thousand Units)

- 5.1 Refrigerators

- 5.1.1 Laboratory refrigerators

- 5.1.2 Blood bank refrigerators

- 5.1.3 Pharmacy refrigerators

- 5.1.4 Chromatography refrigerators

- 5.2 Freezers

- 5.2.1 Ultra-low temperature freezers

- 5.2.2 Plasma freezers

- 5.2.3 Shock freezers

- 5.3 Cryogenic storage systems

- 5.3.1 Liquid nitrogen storage systems

- 5.3.2 Vapor phase storage systems

- 5.4 Cold rooms

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Temperature Range, 2021 - 2034 ($Bn) (Thousand Units)

- 6.1 2°C to 8°C

- 6.2 -20°C to -40°C

- 6.3 -40°C to -80°C

- 6.4 Below -80°C

Chapter 7 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Bn) (Thousand Units)

- 7.1 Small (up to 300 liters)

- 7.2 Medium (300-700 liters)

- 7.3 Large (above 700 liters)

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn) (Thousand Units)

- 8.1 Compressor-based systems

- 8.2 Absorption-based systems

- 8.3 Thermoelectric-based systems

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn) (Thousand Units)

- 9.1 Key trends

- 9.2 Vaccine storage

- 9.3 Blood & blood products storage

- 9.4 Biological sample storage

- 9.5 Drug & pharmaceutical storage

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn) (Thousand Units)

- 10.1 Key trends

- 10.2 Hospitals & clinics

- 10.3 Pharmaceutical companies

- 10.4 Research laboratories

- 10.5 Blood banks

- 10.6 Pharmacies

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Azenta Inc.

- 12.2 Binder

- 12.3 Cardinal Health

- 12.4 Carebios Biological Technology

- 12.5 Darwin Chambers

- 12.6 Elanpro

- 12.7 Farrar

- 12.8 Haier Biomedical

- 12.9 Hoshizaki America

- 12.10 Kendall Cold Chain System

- 12.11 Memmert

- 12.12 Philipp Kirsch

- 12.13 Roemer Industries

- 12.14 Summit Appliances

- 12.15 Thalheimer Kuhlung

低温运输商业仓储物流市场:按服务类型、温度类型、所有权和应用划分-全球预测,2026-2032年

低温运输商业仓储物流市场:按服务类型、温度类型、所有权和应用划分-全球预测,2026-2032年 2025年全球医疗低温运输监控市场报告

2025年全球医疗低温运输监控市场报告 冷藏运输市场,按运输方式、按温度、按技术、按最终用户、按应用、按国家/地区划分 - 2025 年至 2032 年全球行业分析、市场规模、市场份额及预测医疗冷链储存设备市场,按产品类型、按温度范围、按技术、按应用、按最终用户、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

冷藏运输市场,按运输方式、按温度、按技术、按最终用户、按应用、按国家/地区划分 - 2025 年至 2032 年全球行业分析、市场规模、市场份额及预测医疗冷链储存设备市场,按产品类型、按温度范围、按技术、按应用、按最终用户、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测 冷链仓储和物流市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2019-2029F

冷链仓储和物流市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2019-2029F 冷藏运输市场、机会、成长动力、产业趋势分析与预测,2024-2032

冷藏运输市场、机会、成长动力、产业趋势分析与预测,2024-2032