|

市场调查报告书

商品编码

1766339

大肠直肠癌诊断市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Colorectal Cancer Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

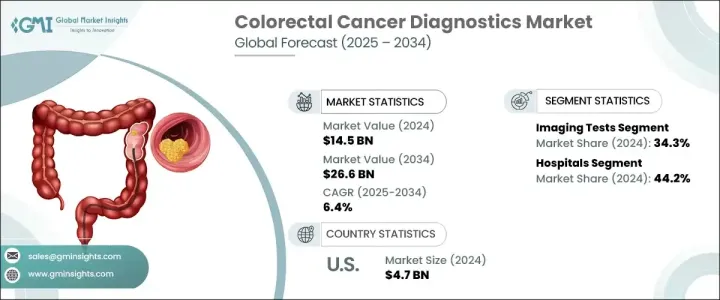

2024 年全球大肠直肠癌诊断市场价值为 145 亿美元,预计到 2034 年将以 6.4% 的复合年增长率增长至 266 亿美元。

市场成长的驱动力源于大肠直肠癌发病率的上升、公共卫生早期筛检倡议的不断推进以及诊断技术的持续进步。液体切片、人工智慧辅助影像和粪便DNA检测等创新技术正在重塑大肠直肠癌检测的格局,提供侵入性更低、更精准、更便捷的诊断方案。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 145亿美元 |

| 预测值 | 266亿美元 |

| 复合年增长率 | 6.4% |

日益增加的宣传活动和更新的筛检指南(例如将常规大肠癌筛检的建议年龄降至45岁)有助于提高早期诊断率。此外,全球人口老化,加上久坐不动和饮食习惯等生活方式因素,加重了全球大肠癌的负担,凸显了对有效且便捷的诊断方法的迫切需求。世界各国政府和医疗保健组织正在启动大规模计划,以改善大肠癌筛检的可近性,而私人企业也在大力投资研发,以将下一代诊断工具推向市场。人工智慧、新一代定序 (NGS) 和微流控技术有望显着提高诊断精度和患者预后。

大肠直肠癌诊断市场主要按检测类型细分,其中影像学检测在2024年占据34.3%的份额。 CT大肠造影、MRI和PET扫描等影像检查方式对于早期发现、分期和治疗计画仍然至关重要。采用AI增强影像技术提高了检测准确性,有助于在早期发现癌前病变。此外,影像学检查的非侵入性或微创性将继续推动患者接受度和筛检率的提高。

就终端用途而言,医院在2024年占据了44.2%的市场份额,巩固了其作为结直肠癌诊断领先终端用户的地位。医院是大肠直肠癌检测、诊断、分期和治疗计划的主要中心,并拥有完善的诊断基础设施,包括先进的影像系统、分子病理学实验室、内视镜设备和肿瘤外科病房。医院的多学科协作方法——汇集肿瘤科医生、放射科医生、病理科医生、胃肠科医生和外科医生——实现了结直肠癌患者从早期发现到治疗后监测的全程无缝衔接的护理协调。

2024年,北美大肠癌诊断市场占35.2%的市占率。该地区的主导地位源于其强大的医疗基础设施、筛检计画的广泛实施以及先进诊断技术的高采用率,例如人工智慧大肠镜检查、液体活检和分子生物标记检测。在美国,美国疾病管制与预防中心(CDC)的结直肠癌控制计画(CRCCP)等措施在提高早期筛检率方面发挥了重要作用,尤其是在医疗资源匮乏的人群中。

雅培实验室、Exact Sciences Corporation、西门子医疗股份公司、Guardant Health Inc.、罗氏公司和通用电气医疗科技公司等主要市场参与者正大力投资,透过液体活检、人工智慧成像和分子诊断领域的创新来扩展其诊断产品组合。策略合作伙伴关係、併购以及新产品的监管审批仍然是这些参与者加强全球影响力和推动未来市场成长的关键策略。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 大肠直肠癌发生率和盛行率不断上升

- 与癌症筛检测试相关的政府措施和政策

- 癌症诊断领域的技术进步

- 早期诊断意识不断增强

- 产业陷阱与挑战

- 诊断测试和程序成本高昂

- 缺乏诊断测试的报销政策

- 市场机会

- 非侵入性和人工智慧驱动的诊断技术的扩展和采用

- 新兴地区市场快速成长

- 成长动力

- 未来市场趋势

- 报销场景

- 消费者行为分析

- 成长潜力分析

- 技术格局

- 监管格局

- 差距分析

- 专利分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按测试类型,2021 - 2034 年

- 主要趋势

- 血液检查

- 粪便检查

- 粪便潜血试验(FOBT)

- 粪便生物标记检测

- CRC DNA筛检测试

- 影像学检查

- CT

- 超音波

- 磁振造影

- 宠物

- 大肠镜检查

- 其他影像学检查

- 活检

- 其他测试类型

第六章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 诊断影像中心

- 癌症研究中心

- 其他最终用途

第七章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第八章:公司简介

- Abbott Laboratories

- Danaher Corporation

- DiaCarta

- Exact Sciences Corporation

- F-Hoffmann-La Roche

- GE HealthCare Technologies

- Geneoscopy

- Guardant Health

- HU Group Holdings

- New Day Diagnostics

- Olympus Corporation

- Phase Scientific International

- QIAGEN NV

- Siemens Healthineers

- Sysmex Corporation

- Thermo Fisher Scientific

The Global Colorectal Cancer Diagnostics Market was valued at USD 14.5 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 26.6 billion by 2034.

The market growth is driven by the increasing incidence of colorectal cancer, rising public health initiatives for early screening, and continuous technological advancements in diagnostic modalities. Innovations such as liquid biopsy, AI-assisted imaging, and stool-based DNA tests are reshaping the landscape of colorectal cancer detection, offering less invasive, more accurate, and patient-friendly diagnostic options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.5 Billion |

| Forecast Value | $26.6 Billion |

| CAGR | 6.4% |

Growing awareness campaigns and updated screening guidelines, such as lowering the recommended age for routine CRC screening to 45, contribute to early diagnosis rates. Furthermore, an aging global population, combined with lifestyle factors like sedentary behavior and dietary habits, has heightened the global burden of colorectal cancer, underscoring the urgent need for effective and accessible diagnostics. Governments and healthcare organizations worldwide are launching large-scale initiatives to improve access to colorectal cancer screening, while private companies are investing heavily in R&D to bring next-generation diagnostic tools to the market. Artificial intelligence, next-generation sequencing (NGS), and microfluidic technologies are poised to enhance diagnostic precision and patient outcomes significantly.

The colorectal cancer diagnostics market is primarily segmented by test type, with the imaging tests segment holding 34.3% share in 2024. Imaging modalities such as CT colonography, MRI, and PET scans remain crucial for early detection, staging, and treatment planning. Adopting AI-enhanced imaging has improved detection accuracy, helping to identify precancerous lesions at earlier stages. Moreover, imaging tests' non-invasive or minimally invasive nature continues to drive patient acceptance and screening rates.

In terms of end-use, the hospitals segment held 44.2% share in 2024, solidifying its position as the leading end-user for colorectal cancer diagnostics. Hospitals are the primary centers for colorectal cancer detection, diagnosis, staging, and treatment planning, supported by a comprehensive diagnostic infrastructure that includes advanced imaging systems, molecular pathology labs, endoscopic equipment, and surgical oncology units. Their multidisciplinary approach-bringing together oncologists, radiologists, pathologists, gastroenterologists, and surgeons-enables the seamless coordination of care for colorectal cancer patients, from early detection through post-treatment monitoring.

North America Colorectal Cancer Diagnostics Market held a 35.2% share in 2024. The region's dominance stems from a robust healthcare infrastructure, widespread implementation of screening programs, and high adoption rates of advanced diagnostic technologies, such as AI-enabled colonoscopy, liquid biopsies, and molecular biomarker testing. In the United States, initiatives like the Colorectal Cancer Control Program (CRCCP) by the CDC have been instrumental in increasing early screening rates, particularly among underserved populations.

Key market players such as Abbott Laboratories, Exact Sciences Corporation, Siemens Healthineers AG, Guardant Health Inc., F-Hoffmann-La Roche Ltd., and GE HealthCare Technologies, Inc. are heavily investing in expanding their diagnostic portfolios through innovations in liquid biopsy, AI-driven imaging, and molecular diagnostics. Strategic partnerships, mergers and acquisitions, and regulatory approvals for new products remain crucial strategies for these players to strengthen their global presence and drive future market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Test type

- 2.2.2 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence and prevalence of colorectal cancer

- 3.2.1.2 Government initiatives and policies associated with cancer screening tests

- 3.2.1.3 Technological advancements in field of cancer diagnostics

- 3.2.1.4 Growing awareness regarding early diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of diagnostic tests and procedures

- 3.2.2.2 Lack of reimbursement policies for diagnostic tests

- 3.2.3 Market Opportunities

- 3.2.3.1 Expansion and Adoption of Non-Invasive and AI-Driven Diagnostic Technologies

- 3.2.3.2 Rapid Market Growth in Emerging Regions

- 3.2.1 Growth drivers

- 3.3 Future market trends

- 3.4 Reimbursement scenario

- 3.5 Consumer behaviour analysis

- 3.6 Growth potential analysis

- 3.7 Technology landscape

- 3.8 Regulatory landscape

- 3.9 Gap analysis

- 3.10 Patent analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Blood tests

- 5.3 Stool tests

- 5.3.1 Fecal occult blood test (FOBT)

- 5.3.2 Fecal biomarker test

- 5.3.3 CRC DNA screening test

- 5.4 Imaging tests

- 5.4.1 CT

- 5.4.2 Ultrasound

- 5.4.3 MRI

- 5.4.4 PET

- 5.4.5 Colonoscopy

- 5.4.6 Other imaging tests

- 5.5 Biopsy

- 5.6 Other test types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Diagnostic imaging centers

- 6.4 Cancer research centers

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 Danaher Corporation

- 8.3 DiaCarta

- 8.4 Exact Sciences Corporation

- 8.5 F-Hoffmann-La Roche

- 8.6 GE HealthCare Technologies

- 8.7 Geneoscopy

- 8.8 Guardant Health

- 8.9 H.U. Group Holdings

- 8.10 New Day Diagnostics

- 8.11 Olympus Corporation

- 8.12 Phase Scientific International

- 8.13 QIAGEN N.V.

- 8.14 Siemens Healthineers

- 8.15 Sysmex Corporation

- 8.16 Thermo Fisher Scientific

大肠直肠癌筛检和诊断市场:按类型、产品类型、应用和最终用户划分-2026-2032年全球市场预测

大肠直肠癌筛检和诊断市场:按类型、产品类型、应用和最终用户划分-2026-2032年全球市场预测 全球大肠直肠癌诊断市场规模、份额、趋势和成长分析报告(2026-2034年)图卡替尼片剂市场按治疗方法、剂量强度、治疗线、支付方类型、最终用户和分销管道划分 - 全球预测(2026-2032 年)大肠直肠癌分子诊断市场按技术、产品类型、应用、生物标记、检体类型和最终用户划分-2026-2032年全球预测

全球大肠直肠癌诊断市场规模、份额、趋势和成长分析报告(2026-2034年)图卡替尼片剂市场按治疗方法、剂量强度、治疗线、支付方类型、最终用户和分销管道划分 - 全球预测(2026-2032 年)大肠直肠癌分子诊断市场按技术、产品类型、应用、生物标记、检体类型和最终用户划分-2026-2032年全球预测 大肠直肠癌药物市场规模、份额和成长分析(按药物类别、分销管道、癌症类型和地区划分):产业预测(2026-2033 年)

大肠直肠癌药物市场规模、份额和成长分析(按药物类别、分销管道、癌症类型和地区划分):产业预测(2026-2033 年) 大肠直肠癌诊断市场-全球产业规模、份额、趋势、机会和预测,按诊断类型(诊断影像、粪便检查、活检等)、按应用、按地区和竞争细分,2020 年至 2030 年

大肠直肠癌诊断市场-全球产业规模、份额、趋势、机会和预测,按诊断类型(诊断影像、粪便检查、活检等)、按应用、按地区和竞争细分,2020 年至 2030 年 转移性大肠直肠癌市场(按药物类别和地区)分析与预测(2025-2035)大肠癌筛检和诊断市场—全球产业规模、份额、趋势、机会和预测(按筛检、诊断、最终用户、地区和竞争细分,2020-2030 年)转移性大肠直肠癌药物市场-全球产业规模、份额、趋势、机会及预测(按药物类别、配销通路、地区和竞争情况划分,2020-2030 年预测)

转移性大肠直肠癌市场(按药物类别和地区)分析与预测(2025-2035)大肠癌筛检和诊断市场—全球产业规模、份额、趋势、机会和预测(按筛检、诊断、最终用户、地区和竞争细分,2020-2030 年)转移性大肠直肠癌药物市场-全球产业规模、份额、趋势、机会及预测(按药物类别、配销通路、地区和竞争情况划分,2020-2030 年预测) 大肠癌筛检与诊断:全球市场

大肠癌筛检与诊断:全球市场