|

市场调查报告书

商品编码

1766340

局部麻醉药物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Local Anesthesia Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

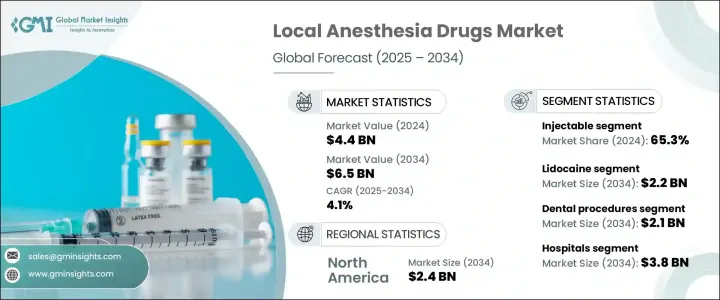

2024 年全球局部麻醉药物市场价值为 44 亿美元,预计到 2034 年将以 4.1% 的复合年增长率增长至 65 亿美元。这一增长主要归因于各类医疗机构手术和微创手术数量的增加。随着门诊、牙科诊所和美容治疗中心对针对性和短期疼痛管理的需求不断增长,对有效局部麻醉剂的需求持续稳定成长。人们越来越倾向于选择能够让患者更快康復并避免全身麻醉相关风险的手术,这有助于推动局部麻醉剂型的广泛使用。老年人口的成长是推动市场扩张的另一个因素,他们通常需要针对特定部位且全身影响较小的手术。此外,新兴市场医疗基础设施的不断发展和外科护理的可近性为这些药物的更广泛应用创造了有利条件。

随着医疗价值导向的转变,人们更加重视更快的復健速度和更短的住院时间,局部麻醉已成为许多治疗的首选。製药公司正积极投资研发,以提升麻醉剂型的疗效、起效时间和持续时间,从而进一步提升产品的可及性和临床应用。监管支援和更快捷的审批流程也在促进市场渗透和技术创新方面发挥着至关重要的作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 44亿美元 |

| 预测值 | 65亿美元 |

| 复合年增长率 | 4.1% |

局部麻醉是指使用药物麻醉特定身体部位,但不影响病人的整体意识。这类麻醉剂有多种形式,包括注射、外用溶液和喷雾剂。这类常用药物包括布比卡因、利多卡因、丙胺卡因、罗哌卡因、苯佐卡因和氯普鲁卡因。

根据药物类型,市场细分为布比卡因、利多卡因、苯佐卡因、丙胺卡因、罗哌卡因、氯普鲁卡因和其他变体。其中,利多卡因市场规模在2024年达到15亿美元,位居榜首,预计到2034年将成长至22亿美元,复合年增长率为3.7%。利多卡因起效迅速、用途广泛,应用范围广泛,尤其是在小手术、皮肤科、牙科和疼痛管理领域,因此仍是最广泛使用的局部麻醉药物之一。利多卡因既有註射剂型,也有外用剂型,这进一步增强了其在各个医学专科领域的吸引力。

根据给药途径,局部麻醉药可分为注射剂和外用剂。注射剂在2024年占据最大份额,达65.3%,预计在整个预测期内仍将保持主导地位。注射剂因其快速起效、精准靶向以及适用于多种临床操作(例如神经阻断和小型外科手术)而广受青睐。给药方法和缓释剂型的持续创新进一步支持了其广泛应用,尤其是在门诊和外科护理领域。

依应用领域划分,市场分为外科手术、牙科手术、美容及皮肤科手术、疼痛管理等。牙科手术在2024年成为领先细分市场,占据33.2%的市场份额,预计到2034年将达到21亿美元。局部麻醉在促进牙科护理方面发挥关键作用,它可以最大限度地减少根管治疗、拔牙和补牙等治疗过程中的不适感。全球口腔健康问题负担日益加重,以及常规牙科护理的普及率不断提高,进一步推动了这个细分市场的突出地位。

根据最终用途,市场包括医院、门诊手术中心和其他医疗保健提供者。 2024年,医院占据56.2%的市场份额,预计到2034年将创造38亿美元的收入,复合年增长率为4.4%。医院仍然是各种需要局部麻醉的外科和诊断程序的主要场所。先进的外科基础设施、训练有素的专业人员和全面的医疗服务巩固了医院作为关键终端使用者群体的地位。

从区域来看,北美地区以2024年17亿美元的收入引领全球市场,预计2034年将达到24亿美元,复合年增长率为3.8%。该地区受益于发达的医疗保健系统、对局部疼痛管理解决方案的认知度不断提高,以及使用局部麻醉的医疗和外科手术频率较高。稳定的研发活动和领先製药公司的存在也为该地区的市场领导地位做出了重要贡献。

市场整合程度适中,前五大公司占约55%的总份额。辉瑞、费森尤斯卡比、B. Braun Melsungen、Septodont和Pacira Biosciences等主要公司继续凭藉创新、全球影响力和策略合作展开竞争,以抢占更大的市场份额。这些公司在拓展产品线、进入新市场和提升製造能力方面的持续努力预计将在未来几年影响市场动态。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 手术量不断增加

- 老年人口状况良好

- 局部麻醉药比阿片类药物的偏好度日益增加

- 药物输送技术的进步推动了需求

- 产业陷阱与挑战

- 剂量依赖性副作用和有限的作用持续时间

- 严格的监管复杂性

- 市场机会

- 扩大美容手术

- 长效麻醉药物的开发

- 成长动力

- 成长潜力分析

- 管道分析

- 未来市场趋势

- 监管格局

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

第五章:市场估计与预测:按药物类型,2021 - 2034 年

- 主要趋势

- 利多卡因

- 布比卡因

- 苯佐卡因

- 罗哌卡因

- 普鲁卡因

- 氯普鲁卡因

- 其他药物类型

第六章:市场估计与预测:按管理路线,2021 - 2034 年

- 主要趋势

- 外用

- 注射剂

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 牙科手术

- 外科手术

- 美容和皮肤科手术

- 疼痛管理

- 其他应用

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 门诊手术中心

- 牙医诊所

- 其他最终用途

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- AbbVie

- AdvaCare

- Aspen Pharmacare

- B. Braun Melsungen

- Baxter

- Fresenius Kabi

- GE Healthcare

- HANSAmed

- Hikima

- Pacira BioSciences

- Pfizer

- Pierrel Spa

- Piramal

- Septodont

The Global Local Anesthesia Drugs Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 4.1% to reach USD 6.5 billion by 2034. This growth is largely attributed to the rising volume of surgeries and minimally invasive procedures across various healthcare facilities. As demand rises for targeted and short-term pain management in outpatient clinics, dental offices, and cosmetic treatment centers, the need for effective local anesthetics continues to grow steadily. An increasing preference for procedures that allow quicker patient recovery and avoid the risks associated with general anesthesia is helping drive the widespread use of local anesthetic formulations. The growing population of older adults, who often require site-specific surgeries with fewer systemic effects, is another factor contributing to the market expansion. Additionally, ongoing development in healthcare infrastructure and access to surgical care in emerging markets are creating favorable conditions for the broader adoption of these drugs.

The shift toward value-based healthcare, where quicker recovery and shorter hospital stays are emphasized, has made local anesthesia a preferred choice in many treatments. Pharmaceutical companies are actively investing in research to improve the efficacy, onset, and duration of anesthetic formulations, further boosting product accessibility and clinical use. Regulatory support and faster approval pathways are also playing a vital role in facilitating market penetration and technological innovation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Billion |

| Forecast Value | $6.5 Billion |

| CAGR | 4.1% |

Local anesthesia refers to the administration of drugs that numb a specific part of the body without affecting the patient's overall consciousness. These anesthetics come in various forms, including injections, topical solutions, and sprays. Commonly used drugs in this category include bupivacaine, lidocaine, prilocaine, ropivacaine, benzocaine, and chloroprocaine.

Based on drug type, the market is segmented into bupivacaine, lidocaine, benzocaine, prilocaine, ropivacaine, chloroprocaine, and other variants. Among these, the lidocaine segment led the market with a value of USD 1.5 billion in 2024 and is expected to grow to USD 2.2 billion by 2034, advancing at a CAGR of 3.7%. Lidocaine remains one of the most extensively used local anesthetics due to its rapid onset, versatility, and wide range of applications, particularly in minor surgeries, dermatology, dentistry, and pain management. The availability of both injectable and topical lidocaine formulations adds to its appeal in various medical specialties.

By route of administration, local anesthetics are divided into injectable and topical types. The injectable segment held the largest share of 65.3% in 2024 and is expected to maintain its dominance throughout the forecast period. Injectables are widely preferred for their quick action, precise targeting, and suitability across numerous clinical procedures, such as nerve blocks and minor surgical interventions. Continuous innovation in delivery methods and extended-release formulations is further supporting their widespread use, particularly in outpatient and surgical care settings.

In terms of application, the market is classified into surgical procedures, dental procedures, cosmetic and dermatological procedures, pain management, and others. Dental procedures emerged as the leading segment in 2024, accounting for 33.2% of the market and projected to reach USD 2.1 billion by 2034. Local anesthesia plays a critical role in facilitating dental care by minimizing discomfort during treatments such as root canals, extractions, and cavity fillings. This segment's prominence is fueled by the increasing global burden of oral health issues and greater access to routine dental care.

According to end use, the market includes hospitals, ambulatory surgical centers, and other healthcare providers. Hospitals represented the dominant share of 56.2% in 2024 and are expected to generate USD 3.8 billion in revenue by 2034, growing at a CAGR of 4.4%. Hospitals continue to serve as the primary site for various surgical and diagnostic procedures that demand the use of local anesthesia. The availability of advanced surgical infrastructure, trained professionals, and comprehensive medical services solidifies their position as a key end-user segment.

Regionally, North America led the global market with USD 1.7 billion in revenue in 2024 and is forecast to reach USD 2.4 billion by 2034, expanding at a CAGR of 3.8%. The region benefits from well-developed healthcare systems, increased awareness regarding localized pain management solutions, and a high frequency of medical and surgical procedures that utilize local anesthesia. Steady R&D activities and the presence of leading pharmaceutical players also contribute significantly to the region's market leadership.

The market is moderately consolidated, with the top five players accounting for approximately 55% of the overall share. Key companies such as Pfizer, Fresenius Kabi, B. Braun Melsungen, Septodont, and Pacira Biosciences continue to compete based on innovation, global presence, and strategic collaborations to capture greater market share. Their ongoing efforts in expanding product lines, entering new markets, and enhancing manufacturing capabilities are expected to influence market dynamics over the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drug type

- 2.2.3 Route of administration

- 2.2.4 Application

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising surgical volume

- 3.2.1.2 Favorable geriatric demographics

- 3.2.1.3 Increasing preference for local anesthetics over opioids

- 3.2.1.4 Advancement in drug delivery drives the demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dose dependent side effects and limited duration of action

- 3.2.2.2 Stringent regulatory complexities

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding aesthetic procedures

- 3.2.3.2 Development of long-acting anesthetics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Lidocaine

- 5.3 Bupivacaine

- 5.4 Benzocaine

- 5.5 Ropivacaine

- 5.6 Prilocaine

- 5.7 Chloroprocaine

- 5.8 Other drug types

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Topical

- 6.3 Injectable

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Dental procedures

- 7.3 Surgical procedures

- 7.4 Cosmetic and dermatological procedures

- 7.5 Pain management

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Dental clinics

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 AdvaCare

- 10.3 Aspen Pharmacare

- 10.4 B. Braun Melsungen

- 10.5 Baxter

- 10.6 Fresenius Kabi

- 10.7 GE Healthcare

- 10.8 HANSAmed

- 10.9 Hikima

- 10.10 Pacira BioSciences

- 10.11 Pfizer

- 10.12 Pierrel Spa

- 10.13 Piramal

- 10.14 Septodont

局部麻醉剂市场规模、份额和成长分析(按药物类型、应用和地区划分)-2026-2033年产业预测

局部麻醉剂市场规模、份额和成长分析(按药物类型、应用和地区划分)-2026-2033年产业预测 全身麻醉剂市场规模、份额和成长分析(按药物类型、给药途径、最终用途、应用领域和地区划分)-2026-2033年产业预测

全身麻醉剂市场规模、份额和成长分析(按药物类型、给药途径、最终用途、应用领域和地区划分)-2026-2033年产业预测 Propofol药物:全球市场份额和排名、总收入和需求预测(2025-2031 年)

Propofol药物:全球市场份额和排名、总收入和需求预测(2025-2031 年) 局部麻醉剂市场按给药途径、药物类别、产品类型、剂型、最终用户、分销管道和应用划分-全球预测,2025-2032年阿法多龙市场按产品形式、治疗领域、应用、通路和最终用户划分-2025-2032年全球预测

局部麻醉剂市场按给药途径、药物类别、产品类型、剂型、最终用户、分销管道和应用划分-全球预测,2025-2032年阿法多龙市场按产品形式、治疗领域、应用、通路和最终用户划分-2025-2032年全球预测 全球全身麻醉药物市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)

全球全身麻醉药物市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年) 氯胺酮诊所市场:依治疗方式、临床指征、给药途径、病患年龄层、治疗类型、转诊管道、经营模式和地区划分麻醉剂市场(按药物类型、给药途径、作用持续时间、用途和最终用户划分)—2025-2030 年全球预测动物麻醉剂市场:依麻醉剂类别、按动物类型、按给药途径、按应用、按分销管道、按最终用户、按地区

氯胺酮诊所市场:依治疗方式、临床指征、给药途径、病患年龄层、治疗类型、转诊管道、经营模式和地区划分麻醉剂市场(按药物类型、给药途径、作用持续时间、用途和最终用户划分)—2025-2030 年全球预测动物麻醉剂市场:依麻醉剂类别、按动物类型、按给药途径、按应用、按分销管道、按最终用户、按地区 局部麻醉剂市场规模、份额、趋势分析报告:按药物、应用、地区、细分市场预测,2025-2030 年

局部麻醉剂市场规模、份额、趋势分析报告:按药物、应用、地区、细分市场预测,2025-2030 年