|

市场调查报告书

商品编码

1773224

功能性麵粉市场机会、成长动力、产业趋势分析及2025-2034年预测Functional Flours Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

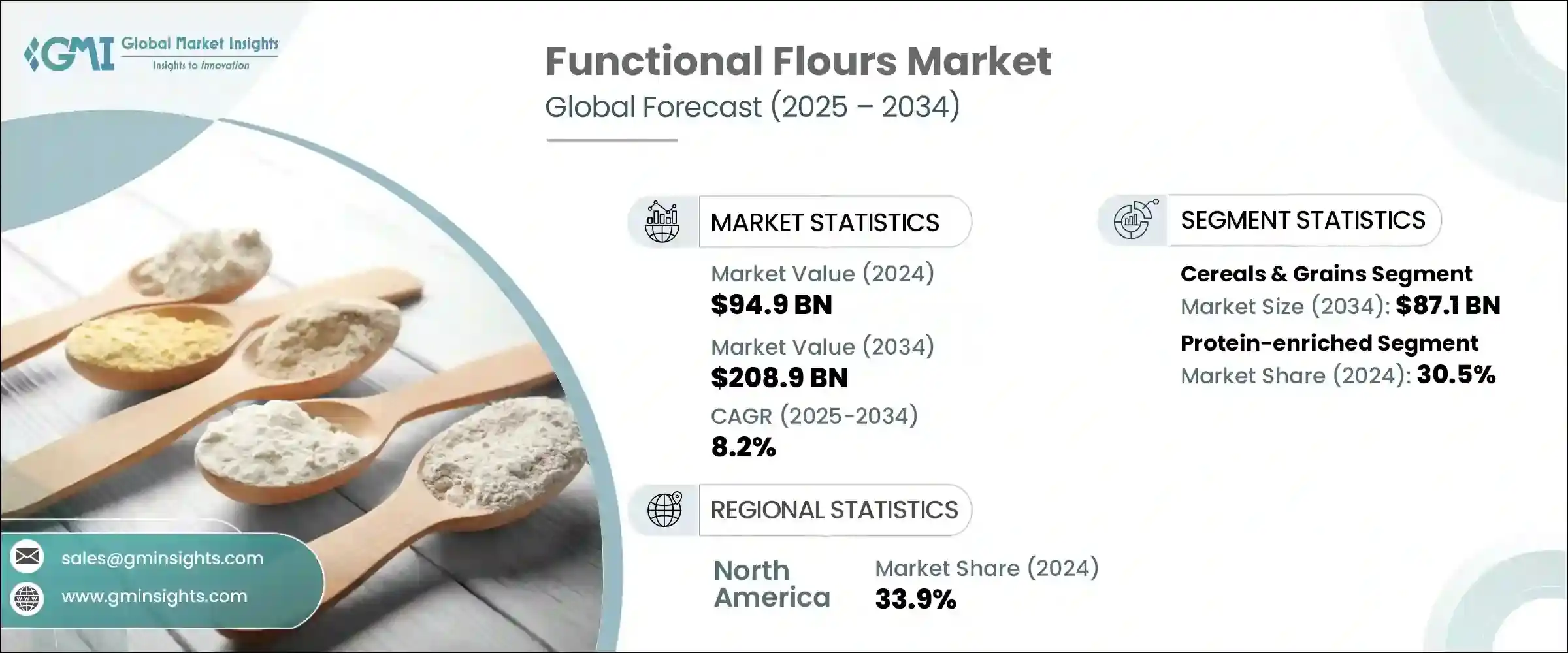

2024年,全球功能性麵粉市场规模达9,49亿美元,预计到2034年将以8.2%的复合年增长率成长,达到2,089亿美元。推动这一增长的动力源于人们日益意识到强化麵粉的健康益处,尤其是在控制肥胖和糖尿病等生活方式相关疾病方面。消费者日益寻求营养丰富的替代品,促使製造商在麵粉中添加纤维、蛋白质和微量营养素。此外,烘焙、零食和方便食品等应用领域(尤其是清洁标籤和无麸质食品领域)的需求不断增长,也增强了市场发展势头。製粉和生产技术的进步也提高了麵粉的标准,使得人们能够生产出质地、营养价值和功能性都得到改善的麵粉。

这些进步使生产商能够满足多样化的消费者期望,并进一步推动市场扩张,因为这些产品能够根据特定的饮食偏好、健康需求和文化趋势来客製化高度专业化的麵粉产品。随着消费者对透明度、功能性和清洁标籤成分的要求日益提高,製造商正在利用这些创新来生产营养价值更高、消化率更高、保质期更长的麵粉。客製化麵粉配方——无论是无麸质、低碳水化合物、高蛋白还是防过敏——的能力使品牌能够满足利基市场的需求,同时扩大其整体消费者群体。反过来,这种与不断发展的食品趋势的策略契合,既支持高端产品定位,也支持大众市场的可扩展性,从而增强了全球功能性麵粉行业的发展势头。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 949亿美元 |

| 预测值 | 2089亿美元 |

| 复合年增长率 | 8.2% |

预计2034年,谷物及杂粮市场规模将达871亿美元,复合年增长率为5.4%。其强大的市场地位得益于其广泛融入麵包、早餐谷物、零食棒和即食食品等日常产品中。消费者对「更健康」食品(尤其是无麸质、全谷物和高纤维配方)的偏好激增,这推动了该领域的成长。随着健康和保健趋势持续影响全球饮食习惯,谷物及杂粮市场在已开发市场和新兴市场都依然占有重要地位。儘管发展势头强劲,但原材料价格波动、运输成本以及偶尔出现的供应链中断仍构成持续的风险。为了应对这些挑战,生产者正致力于透过添加纤维、维生素和矿物质来提高谷物粉的营养密度,以吸引註重健康的消费者。

2024年,高蛋白麵粉市场占30.5%的市占率。预计到2034年,该市场的复合年增长率将达到5.2%,这主要得益于高蛋白饮食需求的激增。高蛋白饮食与提升体能、肌肉健康、饱足感和体重管理息息相关。消费者,尤其是老年人和特定人群,对蛋白质缺乏负面影响的认识不断提高,这加剧了人们对添加蛋白质的功能性麵粉的兴趣。为此,製造商正在开发使用扁豆、豌豆和大豆等植物蛋白的创新产品,以满足日益增长的素食者和纯素食者的需求,同时也满足乳製品或大豆过敏消费者的需求。

2024年,北美功能性麵粉市场占有33.9%的市占率。该地区领先的市场份额主要归功于人们对饮食客製化意识的不断提升,消费者积极寻求适合麸质不耐症、乳糜泻和其他基于生活方式的饮食模式的麵粉。这种需求推动了鹰嘴豆、藜麦和糙米等营养丰富的麵粉的生产和消费。一些老牌产业参与者透过创新和产品多元化不断拓展产品组合,这进一步支撑了市场的成长。

市场主要参与者包括罗盖特公司 (Roquette Freres)、宜瑞安公司 (Ingredion Incorporated)、阿彻丹尼尔斯米德兰公司 (ADM)、SunOpta 公司和英国联合食品公司 (Associated British Foods plc)。功能性麵粉领域的顶尖公司正专注于多元化发展、健康驱动创新和供应链稳健性。他们正在扩大产品范围,将植物蛋白粉和替代谷物纳入其中。在研发方面的大量投入使得客製化麵粉混合物的开发成为可能,这些混合物有助于血糖控制、肠道健康或高蛋白饮食。与烘焙和食品製造商的策略联盟正在提高产品渗透率和最终用途相容性。这些参与者正在透过采购合作伙伴关係和仓储基础设施来加强全球供应链,以对冲原材料价格波动。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 主要製造商

- 经销商

- 整个产业的利润率

- 供应链和分销分析

- 原物料采购

- 生产製造

- 冷链基础设施

- 分销管道

- 供应链挑战与优化

- 永续实践

- 贸易统计(HS编码)

- 2021-2024年主要出口国

- 2021-2024年主要出口国

(註:以上贸易统计仅提供重点国家)

- 衝击力

- 成长动力

- 健康意识不断增强

- 无麸质产品需求不断成长

- 增加蛋白质摄取

- 清洁标籤趋势

- 产业陷阱与挑战

- 与传统麵粉相比成本较高

- 保存期限有限

- 加工挑战

- 口味和质地的限制

- 市场机会

- 亚太新兴市场

- 植物性产品的创新

- 功能性食品应用

- 电子商务扩张

- 成长动力

- 原料景观

- 製造业趋势

- 技术演进

- 加工技术

- 强化方法

- 品质测试与分析

- 包装创新

- 定价分析和成本结构

- 价格趋势(美元/吨)

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东非洲

- 定价因素(原料、能源、劳力)

- 区域价格差异

- 成本结构细分

- 获利能力分析

- 价格趋势(美元/吨)

- 监管框架和标准

- FDA 法规(美国)

- 欧盟法规

- 食品法典标准

- 区域监管机构

- 标籤要求

- 品质标准

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司热图分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

- Expansion

- Mergers & acquisition

- Collaborations

- New product launches

- Research & development

- 主要参与者的最新发展和影响分析

- 公司分类

- 参与者概述

- 财务表现

- 产品基准测试

第五章:市场估计与预测:按来源,2021-2034

- 主要趋势

- 谷物和谷类

- 小麦

- 米

- 玉米

- 燕麦

- 大麦

- 藜麦

- 其他谷物

- 豆类

- 鹰嘴豆

- 扁豆

- 豌豆

- 豆子

- 其他豆类

- 坚果和种子

- 杏仁

- 椰子

- 葵花籽

- 亚麻籽

- 其他坚果和种子

- 水果和蔬菜

- 香蕉

- 甘藷

- 木薯

- 其他水果和蔬菜

- 其他来源

- 昆虫

- 藻类

- 菇

第六章:市场估计与预测:依功能,2021-2034

- 主要趋势

- 富含蛋白质

- 富含纤维

- 不含麸质

- 强化维生素和矿物质

- 低碳水化合物

- 益生菌

- 富含抗氧化剂

- 其他功能

第七章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 烘焙和糖果

- 麵包

- 蛋糕和糕点

- 饼干和饼干

- 鬆饼和纸杯蛋糕

- 其他烘焙产品

- 小吃

- 挤压零食

- 饼干

- 洋芋片

- 其他小吃

- 饮料

- 蛋白质饮料

- 冰沙

- 功能性饮料

- 其他饮料

- 义大利麵和麵条

- 早餐麦片

- 汤和酱汁

- 肉类替代品

- 其他的

第八章:市场估计与预测:依形式,2021-2034

- 主要趋势

- 粉末

- 颗粒

- 薄片

- 颗粒

第九章:市场估计与预测:按配销通路,2021-2034

- 主要趋势

- B2b(企业对企业)

- 食品製造商

- 麵包店

- 餐饮服务

- 其他 B2B 频道

- B2c(企业对消费者)

- 超市和大卖场

- 专卖店

- 网路零售

- 便利商店

- 其他B2C频道

第十章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- MEA

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第 11 章:公司简介

- Cargill, Incorporated

- Archer Daniels Midland Company (ADM)

- Associated British Foods plc

- General Mills, Inc.

- Ingredion Incorporated

- Roquette Freres

- Tate & Lyle PLC

- SunOpta Inc.

- The Scoular Company

- Agrana Beteiligungs-AG

- Limagrain

- Bunge Limited

- The Andersons, Inc.

- Grain Millers, Inc.

- Hodgson Mill, Inc.

- Lifeway Foods, Inc.

- Manildra Group

- Unicorn Grain Specialties

- Bluebird Grain Farms

The Global Functional Flours Market was valued at USD 94.9 billion in 2024 and is estimated to grow at a CAGR of 8.2% to reach USD 208.9 billion by 2034. This surge is being driven by growing awareness of the health advantages that fortified flours offer-particularly their roles in managing lifestyle-related conditions like obesity and diabetes. Consumers increasingly seek nutritious alternatives, leading manufacturers to enrich flours with fibers, proteins, and micronutrients. Additionally, rising demand across applications such as bakery, snacks, and convenience foods-especially clean-label and gluten-free segments-has strengthened market momentum. Technological enhancements in milling and production have also raised the bar, enabling the creation of flours with improved texture, nutritional value, and functional performance.

These advancements allow producers to meet diverse consumer expectations, further fueling market expansion by enabling the development of highly specialized flour products tailored to specific dietary preferences, health needs, and cultural trends. As consumers increasingly demand transparency, functionality, and clean-label ingredients, manufacturers are leveraging these innovations to create flours with enhanced nutritional value, better digestibility, and improved shelf life. The ability to customize flour formulations-whether gluten-free, low-carb, protein-rich, or allergen-friendly-empowers brands to cater to niche markets while broadening their overall consumer base. In turn, this strategic alignment with evolving food trends supports both premium product positioning and mass-market scalability, reinforcing the momentum of the global functional flour industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $94.9 Billion |

| Forecast Value | $208.9 Billion |

| CAGR | 8.2% |

The cereals & grains segment is forecasted to reach USD 87.1 billion by 2034, expanding at a CAGR of 5.4%. Its strong market presence is supported by widespread incorporation in everyday products like bread, breakfast cereals, snack bars, and ready-to-eat foods. A surge in consumer preference for better-for-you options-especially gluten-free, whole-grain, and high-fiber formulations-is fueling this segment's growth. As health and wellness trends continue to shape eating habits globally, this segment remains a staple in both developed and emerging markets. Despite this momentum, fluctuating raw material prices, transportation costs, and occasional supply chain interruptions pose ongoing risks. To counteract these challenges, producers are focusing on increasing the nutritional density of cereal-based flours by fortifying them with added fiber, vitamins, and minerals to appeal to health-conscious buyers.

In 2024, protein-enriched flours segment held 30.5% share. This segment is projected to grow at a CAGR of 5.2% through 2034, driven by surging demand for protein-rich diets, which are widely associated with improved physical performance, muscle health, satiety, and weight management. Heightened consumer awareness of the negative impacts of protein deficiency, especially among older adults and specific demographic groups, is intensifying interest in functional flours with added protein. In response, manufacturers are developing innovative offerings using plant-based proteins like lentils, peas, and soy to support growing vegetarian and vegan populations, while also catering to consumers with dairy or soy allergies.

North America Functional Flours Market held a 33.9% share in 2024. The region's leading share is largely attributed to rising awareness around dietary customization, with consumers actively seeking flours suited for gluten intolerance, celiac disease, and other lifestyle-based eating patterns. This demand is driving the production and consumption of flours derived from nutrient-dense sources like chickpeas, quinoa, and brown rice. The strong presence of established industry players, who are consistently expanding their product portfolios through innovation and product diversification, is further supporting market growth.

Major players in the market include Roquette Freres, Ingredion Incorporated, Archer Daniels Midland Company (ADM), SunOpta Inc., and Associated British Foods plc. Top companies in the functional flour space are focusing on diversification, health-driven innovation, and supply chain robustness. They are expanding their product ranges to include plant-based protein flours and alternative grains. Heavy investment in R&D is enabling the development of custom-tailored flour blends that support blood sugar control, gut health, or high-protein diets. Strategic alliances with bakery and food manufacturers are improving product penetration and end-use compatibility. These players are strengthening global supply chains through sourcing partnerships and storage infrastructure to hedge against raw material price fluctuations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Key manufacturers

- 3.1.2 Distributors

- 3.1.3 Profit margins across the industry

- 3.1.4 Supply chain and distribution analysis

- 3.1.4.1 Raw material sourcing

- 3.1.4.2 Production and manufacturing

- 3.1.4.3 Cold chain infrastructure

- 3.1.4.4 Distribution channels

- 3.1.4.5 Supply chain challenges and optimization

- 3.1.4.6 Sustainable practices

- 3.2 Trade statistics (HS code)

- 3.2.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.2.2 Major exporting countries, 2021-2024 (Kilo Tons)

( Note: the above trade statistics will be provided for key countries only)

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising health consciousness

- 3.3.1.2 Growing demand for gluten-free products

- 3.3.1.3 Increasing protein consumption

- 3.3.1.4 Clean label trends

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High cost compared to conventional flour

- 3.3.2.2 Limited shelf life

- 3.3.2.3 Processing challenges

- 3.3.2.4 Taste and texture limitations

- 3.3.3 Market opportunity

- 3.3.3.1 Emerging markets in Asia-Pacific

- 3.3.3.2 Innovation in plant-based products

- 3.3.3.3 Functional food applications

- 3.3.3.4 E-commerce expansion

- 3.3.1 Growth drivers

- 3.4 Raw material landscape

- 3.4.1 Manufacturing trends

- 3.4.2 Technology evolution

- 3.4.2.1 Processing technologies

- 3.4.2.2 Fortification methods

- 3.4.2.3 Quality testing & analysis

- 3.4.2.4 Packaging innovations

- 3.5 Pricing analysis and cost structure

- 3.5.1 Pricing trends (USD/Ton)

- 3.5.1.1 North America

- 3.5.1.2 Europe

- 3.5.1.3 Asia Pacific

- 3.5.1.4 Latin America

- 3.5.1.5 Middle East Africa

- 3.5.2 Pricing factors (raw materials, energy, labor)

- 3.5.3 Regional price variations

- 3.5.4 Cost structure breakdown

- 3.5.5 Profitability analysis

- 3.5.1 Pricing trends (USD/Ton)

- 3.6 Regulatory framework and standards

- 3.6.1 FDA regulations (U.S.)

- 3.6.2 EU regulations

- 3.6.3 Codex alimentarius standards

- 3.6.4 Regional regulatory bodies

- 3.6.5 Labeling requirements

- 3.6.6 Quality standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Company heat map analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.6.1 Expansion

- 4.6.2 Mergers & acquisition

- 4.6.3 Collaborations

- 4.6.4 New product launches

- 4.6.5 Research & development

- 4.7 Recent developments & impact analysis by key players

- 4.7.1 Company categorization

- 4.7.2 Participant’s overview

- 4.7.3 Financial performance

- 4.8 Product benchmarking

Chapter 5 Market Estimates & Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cereals & grains

- 5.2.1 Wheat

- 5.2.2 Rice

- 5.2.3 Corn

- 5.2.4 Oats

- 5.2.5 Barley

- 5.2.6 Quinoa

- 5.2.7 Other cereals & grains

- 5.3 Legumes

- 5.3.1 Chickpeas

- 5.3.2 Lentils

- 5.3.3 Peas

- 5.3.4 Beans

- 5.3.5 Other legumes

- 5.4 Nuts & seeds

- 5.4.1 Almonds

- 5.4.2 Coconut

- 5.4.3 Sunflower seeds

- 5.4.4 Flax seeds

- 5.4.5 Other nuts & seeds

- 5.5 Fruits & vegetables

- 5.5.1 Banana

- 5.5.2 Sweet potato

- 5.5.3 Cassava

- 5.5.4 Other fruits & vegetables

- 5.6 Other sources

- 5.6.1 Insects

- 5.6.2 Algae

- 5.6.3 Mushrooms

Chapter 6 Market Estimates & Forecast, By Functionality, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Protein enriched

- 6.3 Fiber enriched

- 6.4 Gluten-free

- 6.5 Vitamin & mineral fortified

- 6.6 Low carbohydrate

- 6.7 Probiotic

- 6.8 Antioxidant rich

- 6.9 Other functionalities

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery & confectionery

- 7.2.1 Bread

- 7.2.2 Cakes & pastries

- 7.2.3 Cookies & biscuits

- 7.2.4 Muffins & cupcakes

- 7.2.5 Other bakery products

- 7.3 Snacks

- 7.3.1 Extruded snacks

- 7.3.2 Crackers

- 7.3.3 Chips

- 7.3.4 Other snacks

- 7.4 Beverages

- 7.4.1 Protein drinks

- 7.4.2 Smoothies

- 7.4.3 Functional beverages

- 7.4.4 Other beverages

- 7.5 Pasta & noodles

- 7.6 Breakfast cereals

- 7.7 Soups & sauces

- 7.8 Meat alternatives

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Powder

- 8.3 Granules

- 8.4 Flakes

- 8.5 Pellets

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 B2b (business-to-business)

- 9.2.1 Food manufacturers

- 9.2.2 Bakeries

- 9.2.3 Foodservice

- 9.2.4 Other b2b channels

- 9.3 B2c (business-to-consumer)

- 9.3.1 Supermarkets & hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Online retail

- 9.3.4 Convenience stores

- 9.3.5 Other b2c channels

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Cargill, Incorporated

- 11.2 Archer Daniels Midland Company (ADM)

- 11.3 Associated British Foods plc

- 11.4 General Mills, Inc.

- 11.5 Ingredion Incorporated

- 11.6 Roquette Freres

- 11.7 Tate & Lyle PLC

- 11.8 SunOpta Inc.

- 11.9 The Scoular Company

- 11.10 Agrana Beteiligungs-AG

- 11.11 Limagrain

- 11.12 Bunge Limited

- 11.13 The Andersons, Inc.

- 11.14 Grain Millers, Inc.

- 11.15 Hodgson Mill, Inc.

- 11.16 Lifeway Foods, Inc.

- 11.17 Manildra Group

- 11.18 Unicorn Grain Specialties

- 11.19 Bluebird Grain Farms