|

市场调查报告书

商品编码

1773227

反刍动物甲烷减量市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Ruminant Methane Reduction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

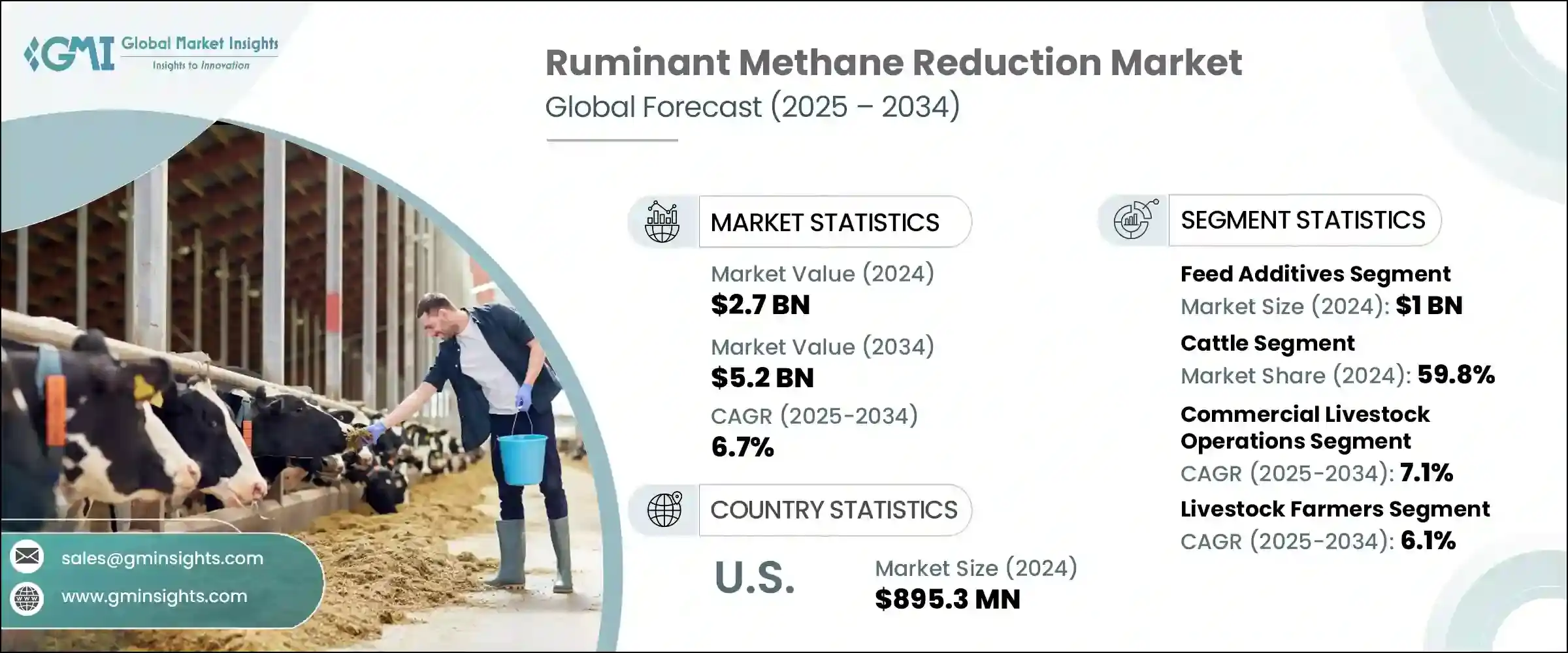

2024年,全球反刍动物甲烷减量市场规模达27亿美元,预计到2034年将以6.7%的复合年增长率成长,达到52亿美元。这一增长反映了减少牛、羊和山羊甲烷排放的迫切需求,这些甲烷排放主要来自肠道发酵。随着全球对动物性蛋白质的需求不断增长,降低反刍动物甲烷排放对于实现气候目标、提高生产效率和支持永续农业实践至关重要。

缓解措施包括日粮添加剂、基因选择、牧场管理和提高畜群生产力。 3-硝基氧丙醇 (3-NOP) 等饲料添加剂和海藻衍生产品已被证明可在不影响动物生产性能的情况下减少高达 80% 的甲烷排放。国家和企业气候计画正在结合补贴、碳信用额度系统和政策框架来推动相关措施的采用。儘管可扩展性和本地适应性挑战依然存在,但将基于饲料的策略与粪便消化器等循环生物经济解决方案相结合,正在进一步加强甲烷减排工作。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 27亿美元 |

| 预测值 | 52亿美元 |

| 复合年增长率 | 6.7% |

儘管可扩展性和适应当地农业条件仍面临诸多挑战,但将以饲料为基础的策略与更广泛的循环生物经济实践相结合,已被证明在扩大甲烷减排力度方面日益有效。透过将甲烷抑制剂和天然饲料添加剂与粪便厌氧消化器等系统相结合,农场可以创建闭环运营,同时应对肠道发酵和废物分解产生的排放。这种双重方法不仅可以提升整体环境效益,还能创造额外的价值流,例如再生能源和有机肥料。

反刍动物甲烷减量市场中的饲料添加剂部分在2024年创造了10亿美元的产值。这些饮食干预措施正成为甲烷减量工作的核心,尤其是在3-硝基氧丙醇(3-NOP)和溴仿基溶液等科学化合物持续证明其在降低肠道排放方面高效且不影响动物生产力的情况下。除合成抑制剂外,精油、植物萃取物和单宁等天然替代品也日益受到青睐,它们由于环保特性和影响瘤胃微生物群落的能力,正越来越多地被添加到饲料中。

2024年,牛市占比59.8%,预计到2034年将以7.1%的复合年增长率成长。这种主导地位源自于其庞大的全球族群数量和高甲烷排放量,尤其是在乳牛和肉牛。乳牛的饮食週期频繁,饲料利用率高,因此特别适合以饲料为基础的减排策略。同时,肉牛通常在粗放型牧场系统中饲养,透过优化放牧、调整饮食和旨在降低排放强度的基因选择,为减少甲烷排放提供了机会。

2024年,美国反刍动物甲烷减量市场产值达8.953亿美元。美国在甲烷减排领域的领先地位得益于联邦和州政府政策的不断完善、企业日益重视气候相关法规的实施以及减排饲料解决方案的快速创新。美国生产商,尤其是乳製品和牛肉生产商,正在迅速添加3-NOP、海藻基化合物和精油等添加剂,以符合自愿减碳倡议和第三方永续性标准。环境、社会和治理 (ESG) 框架下的认证推动进一步推动了这些添加剂的大规模应用。

该市场的领先公司包括赢创工业股份公司、帝斯曼芬美意公司、嘉吉公司、阿彻丹尼尔斯米德兰公司 (ADM) 和巴斯夫公司。为了巩固市场地位,顶级反刍动物甲烷减排公司正在实施多项倡议,并大力投资研发,以开发出功效更高、成本效益更高、区域适应性更强的下一代添加剂。

与饲料製造商、畜牧整合商和研究机构的合作有助于加速产品验证和规模化生产。企业也在全球范围内启动试点计画和饲养试验,以产生性能资料并获得监管部门的批准。与农业合作社和以气候为重点的倡议建立的战略伙伴关係,正在透过补贴和碳信用额度计划扩大饲料添加剂的可及性。此外,产品多样化方面的努力(例如将益生菌基质与甲烷抑制剂结合)正在帮助企业实现产品差异化,并满足畜牧生产中新兴的永续性标准。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- Pestel 分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利格局

- 贸易统计资料(HS 编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按产品,2021 年至 2034 年

- 主要趋势

- 饲料添加剂

- 甲烷抑制剂

- 3-硝基氧丙醇(3-nop)

- 溴仿化合物

- 其他化学抑制剂

- 天然化合物

- 精油

- 植物萃取物

- 海藻基添加剂

- 单宁

- 益生菌和益生元

- 减少甲烷的益生菌

- 益生元化合物

- 酵素

- 其他饲料添加剂

- 甲烷抑制剂

- 遗传和育种解决方案

- 低甲烷遗传学

- 选择性育种计划

- 基因组选择工具

- 管理实践

- 饮食调整

- 优质饲料

- 精料餵养

- 精密进料系统

- 放牧管理

- 畜群管理优化

- 饮食调整

- 生物技术解决方案

- 瘤胃微生物组改造

- 产甲烷菌抑制

- 疫苗研发

- 其他解决方案

- 替代蛋白质来源

- 甲烷捕获技术

- 碳封存方法

第六章:市场估计与预测:按反刍动物 2021 – 2034 年

- 主要趋势

- 牛

- 乳製品

- 牛肉

- 羊

- 山羊

- 水牛

- 其他反刍动物

- 鹿

- 羊驼和骆驼

- 其他物种

第七章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 商业牲畜经营

- 大型乳牛养殖场

- 大规模牛肉养殖

- 饲养场

- 中小型农场

- 家庭乳牛场

- 混合农业经营

- 专业畜牧农场

- 牧场系统

- 粗放放牧系统

- 轮牧系统

- 林草系统

- 研究与开发

- 学术研究机构

- 政府研究项目

- 私人研发设施

第八章:市场估计与预测:依最终用途 2021 – 2034

- 主要趋势

- 畜牧养殖户

- 酪农

- 牛肉生产商

- 绵羊和山羊养殖户

- 饲料生产商

- 商业饲料生产商

- 特种饲料公司

- 饲料添加剂生产者

- 食品和饮料公司

- 乳製品加工商

- 肉类加工商

- 食品服务公司

- 政府及科学研究机构

- 农业部门

- 环境机构

- 研究型大学

- 其他的

- 碳信用开发商

- 咨询服务

- 技术整合商

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- MEA 其余地区

第十章:公司简介

- Agolin SA

- Alltech Inc.

- Archer Daniels Midland Company (ADM)

- ArkeaBio

- BASF SE

- Blue Ocean Barns

- Cargill, Incorporated

- Chr. Hansen Holding A/S

- DSM-Firmenich

- Elanco Animal Health Incorporated

- Evonik Industries AG

- FutureFeed Pty Ltd

- Kemin Industries, Inc.

- Lallemand Inc.

- Mootral SA

- Novozymes A/S

- Rumin8

- Symbrosia Inc.

- Volta Greentech

- Zelp Ltd

The Global Ruminant Methane Reduction Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 5.2 billion by 2034. This growth reflects the increasing imperative to reduce methane emissions from cattle, sheep, and goats, which largely result from enteric fermentation. With global demand for animal-based proteins on the rise, tackling ruminant methane output is essential to meet climate targets, enhance production efficiency, and support sustainable farming practices.

Mitigation approaches include dietary additives, genetic selection, pasture management, and increased herd productivity. Feed additives such as 3-nitrooxypropanol (3-NOP) and seaweed-derived products have shown methane reductions of up to 80% without sacrificing animal performance. National and corporate climate programs are combining subsidies, carbon credit systems, and policy frameworks to drive adoption. While scalability and local adaptation challenges persist, coupling feed-based strategies with circular bioeconomy solutions, like manure digesters, is further enhancing methane mitigation efforts.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 6.7% |

While scalability and adaptation to local farming conditions continue to pose hurdles, the integration of feed-based strategies with broader circular bioeconomy practices is proving increasingly effective in amplifying methane reduction efforts. By aligning methane inhibitors and natural feed additives with systems such as manure anaerobic digesters, farms can create closed-loop operations that tackle emissions from both enteric fermentation and waste decomposition. This dual approach not only boosts overall environmental impact but also generates additional value streams, such as renewable energy and organic fertilizers.

The feed additives segment in the ruminant methane reduction market generated USD 1 billion in 2024. These dietary interventions are becoming central to methane mitigation efforts, especially as science-backed compounds like 3-Nitrooxypropanol (3-NOP) and bromoform-based solutions continue to demonstrate high efficacy in lowering enteric emissions without compromising animal productivity. Alongside synthetic inhibitors, there is rising momentum behind natural alternatives such as essential oils, plant-derived extracts, and tannins, which are being increasingly incorporated into feed due to their environmentally friendly profiles and ability to influence the microbial populations in the rumen.

The cattle segment held a 59.8% share in 2024 and is expected to grow at 7.1% CAGR through 2034. This dominance stems from their significant global population and high levels of methane production, particularly among dairy and beef cattle. Dairy cows, with their frequent dietary cycles and efficient feed utilization, are especially compatible with feed-based reduction strategies. Meanwhile, beef cattle, often raised in extensive pasture systems, present opportunities for methane reduction through grazing optimization, dietary tweaks, and genetic selection aimed at lowering emissions intensity.

U.S. Ruminant Methane Reduction Market generated USD 895.3 million in 2024. The country's leadership is backed by a combination of evolving federal and state policies, increasing adoption of climate-focused corporate mandates, and rapid innovation in emission-reducing feed solutions. American producers, particularly in the dairy and beef sectors, are rapidly incorporating additives like 3-NOP, seaweed-based compounds, and essential oils to align with voluntary carbon reduction initiatives and third-party sustainability standards. The push for certification under environmental, social, and governance (ESG) frameworks further motivates the large-scale deployment of these additives.

Leading companies in this market include Evonik Industries AG, DSM Firmenich, Cargill Incorporated, Archer Daniels Midland Company (ADM), and BASF SE. To strengthen their market position, top ruminant methane reduction companies are implementing multiple initiatives They are investing heavily in R& D to develop next-gen additives with enhanced efficacy, cost-effectiveness, and regional adaptability.

Collaborations with feed manufacturers, livestock integrators, and research institutions help accelerate product validation and scale-up. Firms are also launching pilot programs and feeding trials globally to generate performance data and regulatory approvals. Strategic partnerships with agricultural cooperatives and climate-focused initiatives are expanding access to feed additives through subsidies and carbon-credit programs. Additionally, efforts in product diversification-such as combining probiotic matrices with methane inhibitors-are helping companies differentiate offerings and meet emerging sustainability standards in livestock production.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Ruminant

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 TAM analysis, 2025-2034

- 2.4 Cxo perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Feed additives

- 5.2.1 Methane inhibitors

- 5.2.1.1 3-nitrooxypropanol (3-nop)

- 5.2.1.2 Bromoform compounds

- 5.2.1.3 Other chemical inhibitors

- 5.2.2 Natural compounds

- 5.2.2.1 Essential oils

- 5.2.2.2 Plant extracts

- 5.2.2.3 Seaweed-based additives

- 5.2.2.4 Tannins

- 5.2.3 Probiotics & prebiotics

- 5.2.3.1 Methane-reducing probiotics

- 5.2.3.2 Prebiotic compounds

- 5.2.4 Enzymes

- 5.2.5 Other feed additives

- 5.2.1 Methane inhibitors

- 5.3 Genetic & breeding solutions

- 5.3.1 Low-methane genetics

- 5.3.2 Selective breeding programs

- 5.3.3 Genomic selection tools

- 5.4 Management practices

- 5.4.1 Dietary modifications

- 5.4.1.1 High-quality forages

- 5.4.1.2 Concentrate feeding

- 5.4.1.3 Precision feeding systems

- 5.4.2 Grazing management

- 5.4.3 Herd management optimization

- 5.4.1 Dietary modifications

- 5.5 Biotechnology solutions

- 5.5.1 Rumen microbiome modification

- 5.5.2 Methanogen inhibition

- 5.5.3 Vaccine development

- 5.6 Other solutions

- 5.6.1 Alternative protein sources

- 5.6.2 Methane capture technologies

- 5.6.3 Carbon sequestration methods

Chapter 6 Market Estimates and Forecast, By Ruminant 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cattle

- 6.2.1 Dairy

- 6.2.2 Beef

- 6.3 Sheep

- 6.4 Goats

- 6.5 Buffalo

- 6.6 Other ruminants

- 6.6.1 Deer

- 6.6.2 Alpacas & llamas

- 6.6.3 Other species

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Commercial livestock operations

- 7.2.1 Large-scale dairy farms

- 7.2.2 Large-scale beef operations

- 7.2.3 Feedlots

- 7.3 Small & medium farms

- 7.3.1 Family dairy farms

- 7.3.2 Mixed farming operations

- 7.3.3 Specialty livestock farms

- 7.4 Pasture-based systems

- 7.4.1 Extensive grazing systems

- 7.4.2 Rotational grazing systems

- 7.4.3 Silvopastoral systems

- 7.5 Research & development

- 7.5.1 Academic research institutions

- 7.5.2 Government research programs

- 7.5.3 Private R&D facilities

Chapter 8 Market Estimates and Forecast, By End Use 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Livestock farmers

- 8.2.1 Dairy farmers

- 8.2.2 Beef producers

- 8.2.3 Sheep & goat farmers

- 8.3 Feed manufacturers

- 8.3.1 Commercial feed producers

- 8.3.2 Specialty feed companies

- 8.3.3 Feed additive manufacturers

- 8.4 Food & beverage companies

- 8.4.1 Dairy processors

- 8.4.2 Meat processors

- 8.4.3 Food service companies

- 8.5 Government & research institutions

- 8.5.1 Agricultural departments

- 8.5.2 Environmental agencies

- 8.5.3 Research universities

- 8.6 Others

- 8.6.1 Carbon credit developers

- 8.6.2 Consulting services

- 8.6.3 Technology integrators

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Agolin SA

- 10.2 Alltech Inc.

- 10.3 Archer Daniels Midland Company (ADM)

- 10.4 ArkeaBio

- 10.5 BASF SE

- 10.6 Blue Ocean Barns

- 10.7 Cargill, Incorporated

- 10.8 Chr. Hansen Holding A/S

- 10.9 DSM-Firmenich

- 10.10 Elanco Animal Health Incorporated

- 10.11 Evonik Industries AG

- 10.12 FutureFeed Pty Ltd

- 10.13 Kemin Industries, Inc.

- 10.14 Lallemand Inc.

- 10.15 Mootral SA

- 10.16 Novozymes A/S

- 10.17 Rumin8

- 10.18 Symbrosia Inc.

- 10.19 Volta Greentech

- 10.20 Zelp Ltd