|

市场调查报告书

商品编码

1773234

结节性痒疹治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Prurigo Nodularis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

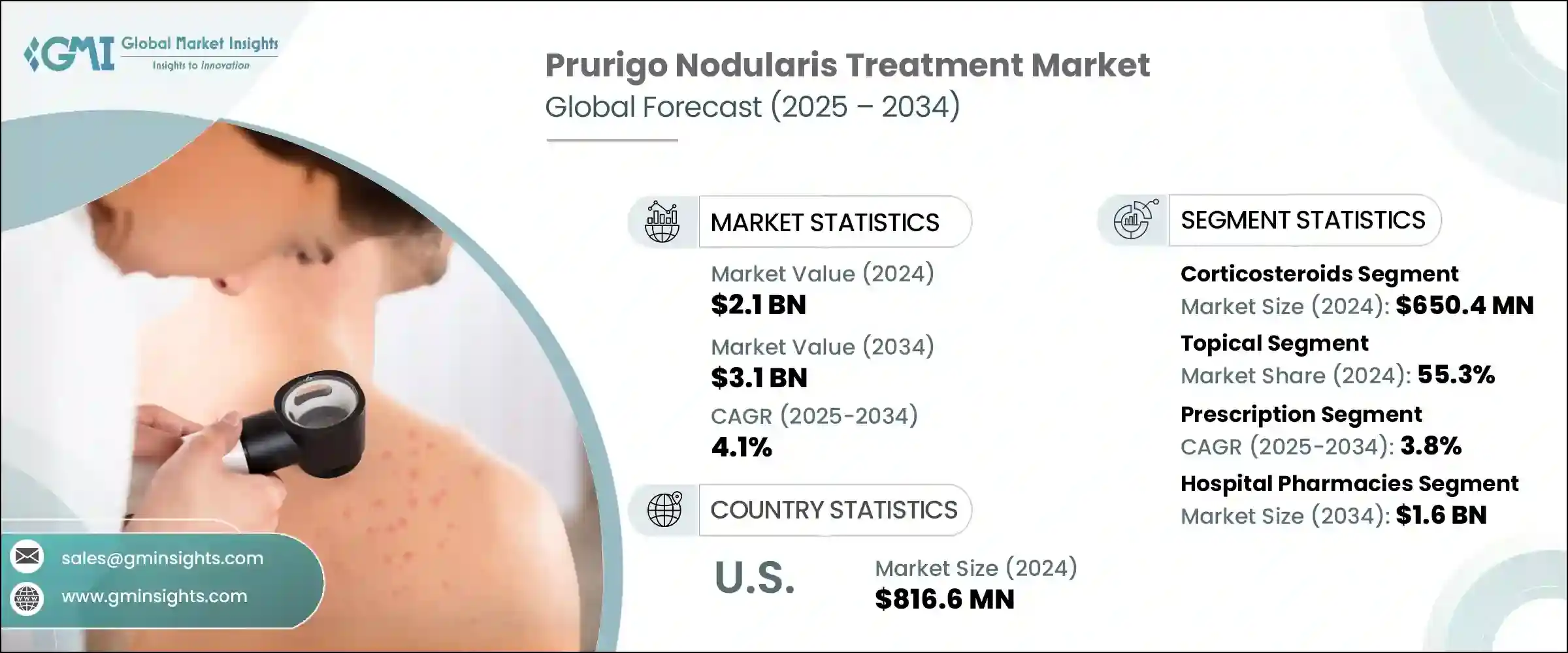

2024年,全球结节性痒疹治疗市场规模达21亿美元,预计2034年将以4.1%的复合年增长率成长,达到31亿美元。这种稳定成长源自于多种相互关联的因素。全球越来越多的人被诊断出患有结节性痒疹(PN),这是一种慢性剧烈搔痒的皮肤病,常发于20至60岁的成年人。 PN与潜在的全身性疾病(包括肝臟、肾臟和神经系统疾病)的关联日益密切,这进一步推动了对有效疗法的需求。

推动需求成长的另一个因素是疾病的致残性,它严重影响生活质量,并且通常需要长期治疗。随着认知度的提高,患者和医护人员都更倾向于寻求不仅针对症状,更能解决病因的医疗解决方案。近年来,製药公司加大了对旨在打破搔痒-抓挠循环并缓解慢性皮肤发炎的疗法研发的投资。针对肠外营养不良症(PN)潜在机制的创新生物製剂正在逐渐改变治疗格局,与传统疗法相比,它们能够提供更有针对性、更持久的疗效。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 21亿美元 |

| 预测值 | 31亿美元 |

| 复合年增长率 | 4.1% |

来自私人投资者和公共医疗计划的资金涌入,为未来的发展奠定了坚实的基础。这些资源推动了生物製剂疗法的上市和开发,这些疗法已在临床研究中显示出良好的疗效。新的标靶治疗方案的出现正在改变处方医生的行为,生物製剂逐渐成为治疗模式的首选。随着更多先进疗法获得监管部门批准并进入市场,这一趋势预计将进一步加速。

结节性痒疹治疗市场涵盖多种旨在控制发炎、搔痒和皮肤病变的药物,包括皮质类固醇、抗组织胺、润肤剂、辣椒素乳膏和生物製剂。其中,皮质类固醇在2024年占据全球市场首位,价值达6.504亿美元。其广泛应用可归因于其强大的抗发炎作用、价格实惠且易于取得。皮质类固醇通常用作第一线治疗药物,用于短期发作和轻度至中度肠外营养不良的长期管理。皮质类固醇有处方药和非处方药两种形式,这增加了其吸引力,使其成为门诊护理和自我管理的首选药物。

2024年,局部治疗占了55.3%的市场份额,凸显了其在局部症状管理中的作用。这些疗法的优点在于能够直接针对受影响的皮肤区域进行标靶给药,从而最大限度地减少全身暴露和副作用。润肤剂、皮质类固醇乳膏和辣椒素类製剂等产品是常用产品,因其使用方便且价格相对较低而备受青睐。这些产品在医疗保健机构和零售药局均易于获取,这巩固了它们持续的主导地位。

处方药类别有望实现显着成长,预计预测期内复合年增长率将达到 3.8%。这一细分市场的成长动力源自于医生监督治疗方案的转变,以及免疫抑制剂、钙调磷酸酶抑制剂和生物製剂等高效能药物的日益普及。随着越来越多的患者就诊于肠外营养 (PN) 的严重症状,对处方药的需求也不断增长。生物製剂尤其助长了这一势头,因为它们能够提供长期控制,并且专为需要持续医疗监督的复杂病例而设计。

医院药局在2024年占据领先地位,预计到2034年将达到16亿美元。这些机构在生物製剂和注射用皮质类固醇等特殊疗法的配药方面发挥着至关重要的作用,尤其对于接受持续治疗或治疗严重肠外营养不良(PN)的患者而言。它们通常采用集中采购系统,从而简化高价药物的取得。此外,它们与皮肤科和免疫科的整合确保了适当的治疗监测和剂量依从性,使其成为晚期肠外营养治疗的关键配销通路。

2024年,北美以41.3%的市占率领先全球市场,其中美国就占据了8.166亿美元的市场。该地区的成长得益于其发达的医疗保健体系、较高的诊断率以及尖端治疗手段的可及性。随着越来越多的患者在临床环境中接受评估,以及相关意识提升措施的推进,对先进疗法的需求持续成长。

竞争格局正在改变。虽然抗组织胺和皮质类固醇等传统疗法依然占据主导地位,但生物製剂的进入已开始重塑治疗模式。製药巨头和生技公司都专注于开发针对特定疾病的疗法,推动了治疗向长期、系统性治疗的转变,而这种治疗不仅限于缓解症状。因此,在监管框架和商业基础设施完善的地区,市场竞争正在加剧。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 结节性痒疹盛行率不断上升

- 药物创新和批准不断增加

- 提高对疾病的认识和皮肤科咨询的可近性

- 产业陷阱与挑战

- 生物疗法成本高昂

- 与某些药物相关的副作用

- 市场机会

- 以患者为中心的数位健康解决方案的采用率不断提高

- 新型生物製剂的开发

- 成长动力

- 成长潜力分析

- 监管格局

- 未来市场趋势

- 管道分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 年至 2034 年

- 主要趋势

- 皮质类固醇

- 抗组织胺药

- 润肤剂

- 辣椒素乳膏

- 生物製剂

- 钙调神经磷酸酶抑制剂

- 免疫抑制剂

- 其他产品类型

第六章:市场估计与预测:依管理路线,2021 年至 2034 年

- 主要趋势

- 外用

- 口服

- 注射剂

第七章:市场估计与预测:依药物类型,2021 年至 2034 年

- 主要趋势

- 处方

- 场外交易

第八章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 网路药局

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Bayer

- Galderma

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Pfizer

- Rugby Pharma

- Sanofi

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- Trevi Therapeutics

- VYNE Therapeutics

The Global Prurigo Nodularis Treatment Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 4.1% to reach USD 3.1 billion by 2034. This steady growth stems from various interrelated factors. A rising number of individuals across the globe are being diagnosed with prurigo nodularis (PN), a chronic and intensely itchy skin condition that often develops in adults between the ages of 20 and 60. PN has been increasingly associated with underlying systemic disorders, including liver, kidney, and neurological conditions, which has further driven the need for effective therapies.

What's also driving the demand is the debilitating nature of the disease, which severely affects the quality of life and often demands long-term treatment. As awareness grows, both patients and medical professionals are more inclined to pursue medical solutions that target not only the symptoms but also the root causes of the condition. In recent years, pharmaceutical companies have ramped up investments in the research and development of therapies that aim to break the itch-scratch cycle and mitigate chronic skin inflammation. Innovative biologics targeting the underlying mechanisms of PN are gradually changing the landscape of care, offering more targeted and durable outcomes compared to traditional therapies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 4.1% |

The influx of funding from private investors and public healthcare initiatives has provided a solid foundation for future advancements. These resources are enabling the launch and development of biologic-based treatments that have demonstrated promising results in clinical studies. The availability of new targeted options is shifting prescriber behavior, with biologics gradually becoming a preferred choice in the treatment paradigm. This trend is expected to further accelerate as more advanced therapies gain regulatory approval and enter the market.

The market for prurigo nodularis treatment includes a wide range of medications aimed at managing inflammation, itch, and skin lesions. These include corticosteroids, antihistamines, emollients, capsaicin creams, and biologics. Among these, corticosteroids led the global market in 2024, with a value of USD 650.4 million. Their widespread use can be attributed to their strong anti-inflammatory effects, affordability, and accessibility. Often used as first-line therapy, corticosteroids are prescribed for both short-term flare-ups and long-term management of mild to moderate PN. Their availability in both prescription and over-the-counter formats adds to their appeal, making them a go-to option for outpatient care and self-management.

Topical treatments accounted for 55.3% of the market share in 2024, highlighting their role in localized symptom management. These therapies offer the advantage of targeted application directly to affected skin areas, minimizing systemic exposure and adverse effects. Products such as emollients, corticosteroid creams, and capsaicin-based formulations are commonly used and are favored for their ease of use and relatively low cost. Their accessibility through both healthcare providers and retail pharmacies reinforces their continued dominance.

The prescription drug category is poised for notable growth, expected to expand at a CAGR of 3.8% over the forecast period. This segment is being driven by a shift toward physician-supervised treatment plans and the increasing use of high-efficacy drugs like immunosuppressants, calcineurin inhibitors, and biologics. As more patients seek medical consultation for PN's severe symptoms, the demand for prescription-only therapies is rising. Biologic agents in particular are contributing to this momentum, as they offer long-term control and are specifically designed for complex cases requiring consistent medical oversight.

Hospital pharmacies held a leading position in 2024 and are projected to reach USD 1.6 billion by 2034. These facilities play a crucial role in dispensing specialized therapies such as biologics and injectable corticosteroids, particularly for patients undergoing continuous treatment or managing severe PN. They often operate under centralized procurement systems that allow for streamlined access to high-cost medications. Moreover, their integration with dermatology and immunology departments ensures proper treatment monitoring and dosage adherence, making them a key distribution channel for advanced PN care.

North America led the global market with a 41.3% share in 2024, with the United States alone accounting for USD 816.6 million. Growth in this region is supported by a well-developed healthcare system, high diagnosis rates, and access to cutting-edge treatments. The demand for advanced therapies continues to grow as more patients are evaluated in clinical settings and awareness initiatives gain traction.

The competitive landscape is transforming. While traditional therapies such as antihistamines and corticosteroids continue to have a presence, the entry of biologics has begun to reshape treatment dynamics. Pharmaceutical leaders and biotech firms alike are focused on the development of disease-specific therapies, creating a shift toward long-term, systemic treatments that go beyond symptom relief. As a result, market competition is intensifying in regions with strong regulatory frameworks and commercial infrastructures.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Route of administration

- 2.2.4 Medication type

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of prurigo nodularis

- 3.2.1.2 Growing innovation and approval of medications

- 3.2.1.3 Rising awareness of disease and accessibility to dermatology consultation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of biologic therapies

- 3.2.2.2 Side effects associated with certain drugs

- 3.2.3 Market opportunities

- 3.2.3.1 Increased adoption of patient-centric digital health solutions

- 3.2.3.2 Development of novel biologics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Pipeline analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Corticosteroids

- 5.3 Antihistamines

- 5.4 Emollients

- 5.5 Capsaicin cream

- 5.6 Biologics

- 5.7 Calcineurin inhibitors

- 5.8 Immunosuppressants

- 5.9 Other product types

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Topical

- 6.3 Oral

- 6.4 Injectable

Chapter 7 Market Estimates and Forecast, By Medication Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Prescription

- 7.3 OTC

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bayer

- 10.2 Galderma

- 10.3 GlaxoSmithKline

- 10.4 Johnson & Johnson

- 10.5 Merck

- 10.6 Pfizer

- 10.7 Rugby Pharma

- 10.8 Sanofi

- 10.9 Takeda Pharmaceuticals

- 10.10 Teva Pharmaceutical Industries

- 10.11 Trevi Therapeutics

- 10.12 VYNE Therapeutics