|

市场调查报告书

商品编码

1773249

离心鼓风机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Centrifugal Blower Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

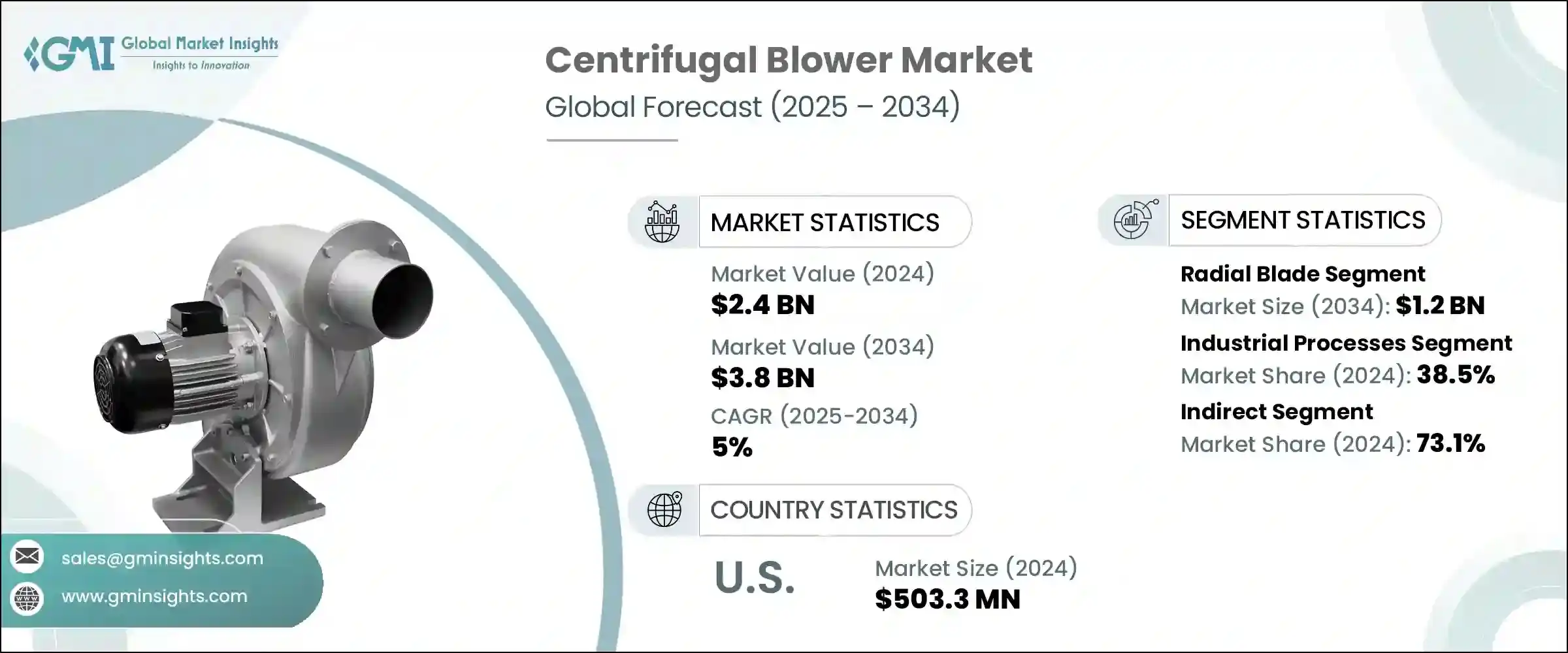

2024年,全球离心鼓风机市场规模达24亿美元,预计2034年将以5%的复合年增长率成长,达到38亿美元。该市场的成长轨迹与汽车、暖通空调、化学加工和发电等行业日益增长的需求密切相关。离心鼓风机是空气和气体输送系统的关键部件,包括通风、冷却和气动输送系统。

这些鼓风机的普及率激增,很大程度归功于提升能源效率、减少环境影响和延长使用寿命的创新技术。采用智慧技术设计的先进鼓风机型号的推出,正在支持现代製造业,尤其是那些与工业4.0相契合的製造业,这些製造业强调自动化、生产力和数据驱动的效率。随着各行各业积极寻求降低能源消耗和碳足迹的解决方案,节能鼓风机已成为营运策略的核心。这些鼓风机不仅支持工业永续发展目标,还有助于降低能源密集产业的公用事业费用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 24亿美元 |

| 预测值 | 38亿美元 |

| 复合年增长率 | 5% |

在采矿和发电等行业,离心式鼓风机的角色不仅限于气流控制,还包括关键的安全功能。它们有助于在危险的工作环境中维持洁净的空气区域,并确保敏感设备的平稳运作。随着监管压力的不断增加以及人们对工作场所安全和环境标准的认识不断提高,对可靠耐用鼓风机的需求正在加速增长。随着企业努力满足合规要求并加强风险缓解策略,离心式鼓风机正越来越多地被整合到核心营运中。

食品饮料产业是离心式鼓风机应用的另一个关键驱动因素。这些系统支持高水准的卫生条件,这在食品加工环境中至关重要。随着全球对包装和加工食品的需求持续增长,生产线对空气过滤和气味控制系统的需求也日益增长。离心式鼓风机提供精确的气流控制,使其成为食品製造所需的无尘室环境和空气净化系统的理想选择。食品生产领域自动化和可编程系统的持续扩展也推动了先进鼓风机配置市场的发展。

按类型划分,径向叶片离心式鼓风机在2024年占据市场主导地位,估值达7.885亿美元,预计到2034年将达到12亿美元。该细分市场凭藉其高效的气流性能、跨行业的适应性以及持续优化能耗的设计改进,仍然是首选。随着各行各业对兼具营运效能与节能效果的解决方案的需求日益增长,径向叶片配置在各个应用领域持续受到青睐。

在应用方面,工业流程中使用的离心式鼓风机在2024年占了全球约38.5%的市场份额,预计2025年至2034年的复合年增长率将达到5.4%。这些鼓风机对空气燃烧、物料处理和排气系统等多项关键功能至关重要。它们能够承受恶劣环境并维持稳定的性能,使其成为製造、炼油和重工业运作中不可或缺的一部分。人们越来越重视提高流程效率和减少停机时间,这使得离心式鼓风机在工业系统中得到更广泛的应用。

纵观分销格局,间接销售通路在2024年占据主导地位,份额接近73.1%。经销商在市场扩张中发挥关键作用,帮助製造商接触更广泛的客户群,并加快产品在各地区的供应速度。这些中间商通常提供售后支援、技术支援和产品服务,从而提升客户满意度并促进回头客。製造商与分销伙伴之间的策略合作持续塑造市场格局,增强了该领域间接销售的实力。

从地区来看,美国在2024年的市值达到5.033亿美元,预计预测期内的复合年增长率为4.5%。美国完善的工业生态系统,涵盖製造业、石化产业和暖通空调产业,为离心鼓风机的需求提供了坚实的基础。成熟的物流基础设施和广泛的分销渠道网络确保了先进的鼓风机系统在全国范围内随时可用,从而支持国内消费的稳步增长。

离心鼓风机市场汇集了许多全球知名製造商和区域性供应商。该领域的主要参与者包括Airmake Cooling Systems、Aerotech Equipment、Alfotech Fans、Atlas Copco、Atlantic Blowers LLC、Chuan-Fan Electric Co., Ltd.、Colfax Corporation、CLEANTEK、Elektror Airsystems、HIS Blower、Illinois Blower Company、山东华东鼓风机有限公司、The Spencer Turbine Company、Trimech India 和 Vishwakarma Air Systems。竞争格局仍然较为分散,这有利于持续创新和製定具有竞争力的定价策略。虽然由于技术要求和资本投入存在一些进入壁垒,但市场环境仍然有利于新进入者和专注于定製或区域特定解决方案的利基市场参与者。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 监理框架

- 标准和认证

- 环境法规

- 进出口法规

- 贸易统计数据

- 主要进口国

- 主要出口国

- 波特五力分析

- PESTEL分析

- 消费者行为分析

- 购买模式

- 偏好分析

- 消费者行为的区域差异

- 电子商务对购买决策的影响

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 径向叶片

- 前弯

- 向后弯曲

- 混流

- 轴流

- 多级

- 其他的

第六章:市场估计与预测:按驱动机制,2021 - 2034 年

- 主要趋势

- 直接驱动

- 皮带传动

第七章:市场估计与预测:按压力,2021 - 2034 年

- 主要趋势

- 高的

- 中等的

- 低的

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 暖通空调系统

- 工业製程

- 发电

- 製药

- 食品加工

- 矿业

- 农业

- 其他的

第九章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 直销

- 间接销售

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 马来西亚

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第 11 章:公司简介

- Aerotech Equipments and Projects Pvt. Ltd

- Airmake Cooling Systems

- Alfotech Fans

- Atlantic Blowers LLC

- Atlas Copco

- Chuan-Fan Electric Co., Ltd.

- CLEANTEK

- Colfax Corporation

- Elektror Airsystems

- EVG Engicon Airtech Pvt. Ltd.

- HIS Blower

- Illinois Blower Inc.

- Kaeser kompressoren

- Shandong Huadong Blower Co., Ltd.

- The New York Blower Company

- The Spencer Turbine Company

- Trimech India

- Vishwakarma Air Systems

The Global Centrifugal Blower Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 3.8 billion by 2034. The market's growth trajectory is closely tied to rising demand from industries such as automotive, HVAC, chemical processing, and power generation. Centrifugal blowers are key components in systems that move air and gas, including ventilation, cooling, and pneumatic conveying systems.

The surge in the adoption of these blowers is largely attributed to innovations that enhance energy efficiency, reduce environmental impact, and extend operational life. The introduction of advanced blower models designed with smart technologies is supporting modern manufacturing initiatives, particularly those aligned with Industry 4.0, which emphasize automation, productivity, and data-driven efficiency. With industries actively seeking solutions to reduce their energy consumption and carbon footprint, energy-efficient blowers have become central to operational strategies. These blowers not only support industrial sustainability goals but also help lower utility expenses in energy-intensive sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 5% |

In sectors like mining and power generation, the role of centrifugal blowers extends beyond airflow control to include critical safety functions. They help maintain clean air zones in hazardous work environments and ensure the smooth operation of sensitive equipment. With increasing regulatory pressures and rising awareness about workplace safety and environmental standards, the demand for reliable and durable blowers is accelerating. Centrifugal blowers are being increasingly integrated into core operations as companies strive to meet compliance requirements and enhance risk mitigation strategies.

The food and beverage sector is another key contributor to centrifugal blower adoption. These systems support high levels of sanitation and hygiene, which are crucial in food processing environments. As global demand for packaged and processed foods continues to rise, the need for air filtration and odor control systems within processing lines is growing. Centrifugal blowers offer precise airflow control, making them ideal for supporting cleanroom environments and air purification systems required in food manufacturing. The continued expansion of automation and programmable systems within food production is also boosting the market for advanced blower configurations.

By type, radial blade centrifugal blowers dominated the market in 2024 with a valuation of USD 788.5 million and are estimated to reach USD 1.2 billion by 2034. This segment remains the top choice due to its effective airflow performance, adaptability across various sectors, and ongoing improvements in design that optimize energy consumption. As industries increasingly demand solutions that combine operational performance with energy savings, the radial blade configuration continues to gain traction across applications.

In terms of application, centrifugal blowers used in industrial processes accounted for approximately 38.5% of the global market share in 2024 and are projected to register a CAGR of 5.4% from 2025 to 2034. These blowers are vital to several key functions, such as air combustion, material handling, and exhaust systems. Their ability to withstand harsh environments and deliver consistent performance makes them indispensable in manufacturing, refining, and heavy industrial operations. The growing emphasis on improving process efficiency and reducing downtime has led to the wider adoption of centrifugal blowers in industrial systems.

Looking at the distribution landscape, the indirect sales channel held a dominant share of nearly 73.1% in 2024. Distributors play a pivotal role in market expansion, offering manufacturers access to a wider customer base and enabling faster product availability across regions. These intermediaries often provide post-sale support, technical assistance, and product servicing, which enhances customer satisfaction and fosters repeat business. Strategic collaborations between manufacturers and distribution partners continue to shape the market, reinforcing the strength of indirect sales in this sector.

Regionally, the United States recorded a market value of USD 503.3 million in 2024 and is expected to grow at a CAGR of 4.5% over the forecast period. The country's well-established industrial ecosystem, which includes manufacturing, petrochemical, and HVAC sectors, provides a solid foundation for centrifugal blower demand. Access to a mature logistics infrastructure and a broad network of distribution channels ensures that advanced blower systems are readily available nationwide, supporting a steady uptick in domestic consumption.

The centrifugal blower market features a mix of prominent global manufacturers and region-focused suppliers. Key players in the space include Airmake Cooling Systems, Aerotech Equipment, Alfotech Fans, Atlas Copco, Atlantic Blowers LLC, Chuan-Fan Electric Co., Ltd., Colfax Corporation, CLEANTEK, Elektror Airsystems, HIS Blower, Illinois Blower Inc., EVG Engicon Airtech Pvt. Ltd., Kaeser Kompressoren, The New York Blower Company, Shandong Huadong Blower Co., Ltd., The Spencer Turbine Company, Trimech India, and Vishwakarma Air Systems. The competitive landscape remains moderately fragmented, which encourages ongoing innovation and competitive pricing strategies. While some entry barriers exist due to technical requirements and capital investments, the environment remains conducive for new entrants and niche players focusing on custom or region-specific solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Driving mechanism

- 2.2.4 Pressure

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Radial blade

- 5.3 Forward-curved

- 5.4 Backwards curved

- 5.5 Mixed flow

- 5.6 Axial flow

- 5.7 Multi-stage

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Drive Mechanism, 2021 - 2034, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Direct drive

- 6.3 Belt drive

Chapter 7 Market Estimates & Forecast, By Pressure, 2021 - 2034, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 High

- 7.3 Medium

- 7.4 Low

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 HVAC

- 8.3 Industrial processes

- 8.4 Power generation

- 8.5 Pharmaceutical

- 8.6 Food processing

- 8.7 Mining

- 8.8 Agriculture

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Aerotech Equipments and Projects Pvt. Ltd

- 11.2 Airmake Cooling Systems

- 11.3 Alfotech Fans

- 11.4 Atlantic Blowers LLC

- 11.5 Atlas Copco

- 11.6 Chuan-Fan Electric Co., Ltd.

- 11.7 CLEANTEK

- 11.8 Colfax Corporation

- 11.9 Elektror Airsystems

- 11.10 EVG Engicon Airtech Pvt. Ltd.

- 11.11 HIS Blower

- 11.12 Illinois Blower Inc.

- 11.13 Kaeser kompressoren

- 11.14 Shandong Huadong Blower Co., Ltd.

- 11.15 The New York Blower Company

- 11.16 The Spencer Turbine Company

- 11.17 Trimech India

- 11.18 Vishwakarma Air Systems

超高压离心风机市场:全球预测(2026-2032 年),按风机类型、压力范围、驱动系统、材质、最终用户和销售管道

超高压离心风机市场:全球预测(2026-2032 年),按风机类型、压力范围、驱动系统、材质、最终用户和销售管道 离心式鼓风机市场规模、份额和成长分析(按类型、驱动机构、压力、应用、分销管道和地区划分)—2026-2033年产业预测

离心式鼓风机市场规模、份额和成长分析(按类型、驱动机构、压力、应用、分销管道和地区划分)—2026-2033年产业预测 离心式呼吸器供气设备:全球市场份额和排名、总收入和需求预测(2025-2031 年)离心鼓风机市场(依产品类型、叶轮设计、压力范围、安装、材料、额定功率和最终用途)-2025-2030 年全球预测

离心式呼吸器供气设备:全球市场份额和排名、总收入和需求预测(2025-2031 年)离心鼓风机市场(依产品类型、叶轮设计、压力范围、安装、材料、额定功率和最终用途)-2025-2030 年全球预测 离心鼓风机市场规模、份额、趋势分析报告:按最终用途、压力、地区、细分市场预测,2025-2030 年

离心鼓风机市场规模、份额、趋势分析报告:按最终用途、压力、地区、细分市场预测,2025-2030 年 2025-2033 年按压力(高压、中压、低压)、最终用户(水泥厂、钢厂、采矿、发电站、化工、纸浆和造纸等)和地区分類的离心鼓风机市场报告

2025-2033 年按压力(高压、中压、低压)、最终用户(水泥厂、钢厂、采矿、发电站、化工、纸浆和造纸等)和地区分類的离心鼓风机市场报告