|

市场调查报告书

商品编码

1773250

网路流量分析市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Network Traffic Analytics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

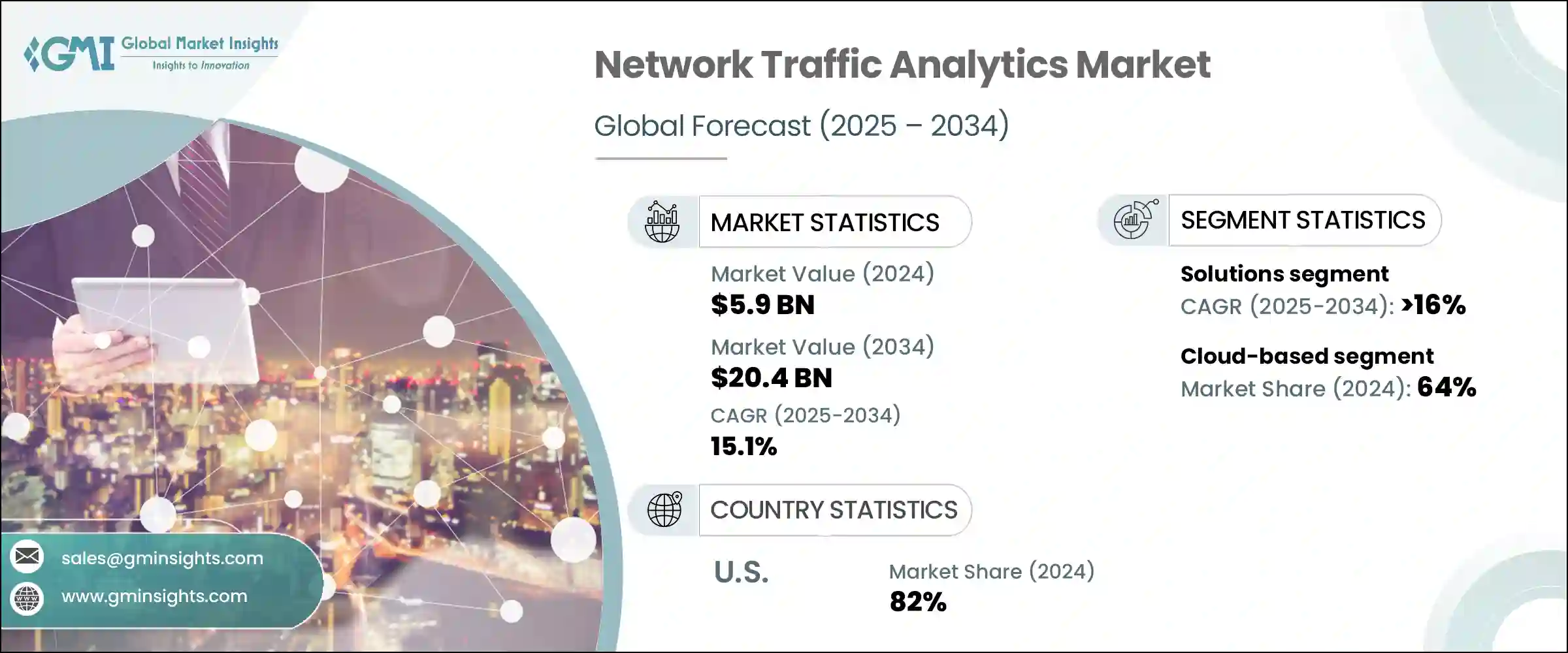

2024年,全球网路流量分析市场规模达59亿美元,预计2034年将以15.1%的复合年增长率成长,达到204亿美元。这一增长源于对复杂数位网路中即时营运情报、安全性和可视性日益增长的需求。随着企业纷纷采用混合云端环境并应对不断演变的网路威胁,理解和管理资料流变得至关重要。随着远端办公、物联网设备和基于人工智慧的应用激增,可扩展的分析平台变得至关重要。这些解决方案能够提供网路效能、威胁侦测和合规性的可行洞察,使企业能够保持安全、高效且不间断的连线。

透过持续分析资料包和串流资料,网路流量分析工具可以帮助 IT 团队快速侦测异常,确保合规性,并优化资料路由,从而防止拥塞或中断。对于适应现代数位化环境的企业而言,它们已成为不可或缺的工具。随着企业规模的扩大和数位化环境的多样化,这些工具能够深入了解网路行为,从而实现主动威胁侦测和快速事件回应。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 59亿美元 |

| 预测值 | 204亿美元 |

| 复合年增长率 | 15.1% |

随着云端服务、虚拟化基础架构和行动优先员工队伍的日益普及,维护无缝且安全的网路效能变得比以往任何时候都更加复杂。网路流量分析解决方案使企业能够监控即时流量模式,确定关键任务应用程式的优先级,并在可疑活动升级之前将其隔离。这些解决方案能够将原始网路资料转化为可操作的情报,从而使 IT 团队能够更敏捷地运营,改进服务交付,并增强整体网路安全韧性。

2024年,解决方案细分市场占据了68%的市场份额,预计到2034年将成长16%。这种主导地位凸显了先进的软体平台对现代网路管理的重要性。企业正在投资先进的工具,提供合规性报告、行为分析和加密流量视觉化功能。从定期批量分析到持续即时串流的转变标誌着现代网路分析的转型。

2024年,基于云端的细分市场占据64%的份额,预计复合年增长率为16%。云端平台能够快速处理大量网路流量,消除前期硬体投资,并灵活应对不断变化的工作负载,同时还能在全球站点提供集中式洞察。这些优势使云端部署成为寻求敏捷、可扩展分析的企业的首选。

美国网路流量分析市场占了82%的市场份额,2024年市场规模达到17亿美元。这一领先地位体现了美国先进的IT基础设施以及对下一代网路安全解决方案的早期采用。金融、医疗保健、製造业和政府等产业越来越依赖分析工具来监控加密流量、实施人工智慧驱动的威胁侦测,并在分散的云端环境中保持法规遵循。

引领该市场的全球公司包括思科系统、Cloudflare、博通、Zoho、IBM Corporation、Arista Networks、NEC Corporation、SolarWinds Worldwide、Fortra 和 Progress Software。主要参与者正在透过创新、策略合作伙伴关係和垂直扩展来巩固其市场地位。他们正在大力投资人工智慧和机器学习增强技术,以改善异常检测、预测性威胁预防和加密流量分析。

平台与云端原生环境、端点安全和 SIEM 系统的整合是实现统一安全和效能管理的策略重点。企业也在扩展託管服务和订阅模式,以提供满足企业需求的可扩展产品。与云端服务供应商和电信营运商结盟可以实现更广泛的部署和市场覆盖范围。此外,供应商强调以合规性为重点的分析,以因应日益增长的监管要求。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 网路安全威胁不断上升

- 物联网和互联设备的快速成长

- 采用云端服务

- 5G网路的扩展

- 产业陷阱与挑战

- 实施成本高

- 可扩展性和整合挑战

- 市场机会

- 增加行业特定定制

- 与 SOAR 和 SIEM 工具集成

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 成本細項分析

- 软体开发和授权成本

- 部署和整合成本

- 维护和支援成本

- 网路安全与合规成本

- 培训和变更管理成本

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 用例

- 最佳情况

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 解决方案

- 网路效能监控

- 网路安全监控

- 网路行为分析

- 网路流量可视化

- 服务

- 专业的

- 咨询

- 部署与集成

- 支援与维护

- 託管

- 专业的

第六章:市场估计与预测:依部署模式,2021 - 2034 年

- 主要趋势

- 本地

- 基于云端

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 安全和威胁侦测

- 入侵侦测与预防

- 进阶持续性威胁 (APT) 侦测

- 内部威胁侦测

- 效能监控和优化

- 网路容量规划

- 异常检测

- 合规与审计

第八章:市场估计与预测:依企业规模,2021 - 2034 年

- 主要趋势

- 中小企业

- 大型企业

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 金融服务业

- IT和电信

- 政府和国防

- 卫生保健

- 零售与电子商务

- 製造业

- 能源和公用事业

- 教育

- 其他的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧人

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Arista Networks

- Broadcom

- Cisco Systems

- Cloudflare

- Dynatrace

- ExtraHop Networks

- Fortinet

- Fortra

- IBM Corporation

- Juniper Networks

- NEC Corporation

- NetScout Systems

- NTT

- Palo Alto Networks

- Progress Software Corporation

- Riverbed Technology

- SolarWinds Worldwide

- Splunk

- Viavi Solutions

- Zoho Corporation

The Global Network Traffic Analytics Market was valued at USD 5.9 billion in 2024 and is estimated to grow at a CAGR of 15.1% to reach USD 20.4 billion by 2034. This growth is driven by increasing demand for real-time operational intelligence, security, and visibility in complex digital networks. As organizations embrace hybrid cloud environments and contend with evolving cyber threats, understanding and managing data flow has become critical. With the surge in remote work, IoT devices, and AI-based applications, scalable analytics platforms have become essential. These solutions offer actionable insights into network performance, threat detection, and compliance, empowering businesses to maintain secure, efficient, and uninterrupted connectivity.

By continually analyzing packet and flow data, network traffic analytics tools help IT teams quickly detect anomalies, ensure compliance, and optimize data routes to prevent congestion or outages. They have become indispensable for enterprises adapting to modern digital landscapes. As organizations scale and diversify their digital environments, these tools offer deep visibility into network behavior, enabling proactive threat detection and swift incident response.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.9 Billion |

| Forecast Value | $20.4 Billion |

| CAGR | 15.1% |

With the rising adoption of cloud services, virtualized infrastructure, and mobile-first workforces, maintaining seamless and secure network performance is more complex than ever. Network traffic analytics solutions empower businesses to monitor real-time traffic patterns, prioritize mission-critical applications, and isolate suspicious activities before they escalate. Their ability to turn raw network data into actionable intelligence allows IT teams to operate with greater agility, improve service delivery, and enhance overall cybersecurity resilience.

In 2024, the solutions segment held 68% share and is expected to grow at 16% through 2034. This dominance underscores how vital sophisticated software platforms are to modern network management. Companies are investing in advanced tools offering compliance reporting, behavioral analysis, and visibility into encrypted traffic. The shift from periodic batch analytics to continuous real-time streaming marks modern network analytics' transformation.

The cloud-based segment held a 64% share in 2024 and is projected to grow at a CAGR of 16%. Cloud platforms enable rapid processing of massive network volumes, eliminate upfront hardware investments, and offer flexibility to handle fluctuating workloads-all while providing centralized insight across global sites. These benefits make cloud deployment the preferred choice for businesses seeking agile, scalable analytics.

United States Network Traffic Analytics Market held an 82% share and generated USD 1.7 billion in 2024. This leadership reflects the country's advanced IT infrastructure and early adoption of next-gen network security solutions. Industries such as finance, healthcare, manufacturing, and government are increasingly relying on analytics tools to monitor encrypted traffic, implement AI-driven threat detection, and maintain regulatory compliance across dispersed cloud environments.

Global companies leading this market include Cisco Systems, Cloudflare, Broadcom, Zoho, IBM Corporation, Arista Networks, NEC Corporation, SolarWinds Worldwide, Fortra, and Progress Software. Key players are strengthening their market position through innovation, strategic partnerships, and vertical expansion. They are investing heavily in AI and machine learning enhancements to improve anomaly detection, predictive threat prevention, and encrypted traffic analysis.

Platform integration with cloud-native environments, endpoint security, and SIEM systems is a strategic focus to offer unified security and performance management. Companies are also expanding managed services and subscription models to provide scalable offerings that match enterprise needs. Forming alliances with cloud providers and telecom operators allows wider deployment and market reach. Additionally, vendors emphasize compliance-focused analytics to address rising regulatory demands.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Mode

- 2.2.4 Application

- 2.2.5 Enterprise Size

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising cybersecurity threats

- 3.2.1.2 Rapid growth in IoT and connected devices

- 3.2.1.3 Adoption of cloud services

- 3.2.1.4 Expansion of 5G networks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation costs

- 3.2.2.2 Scalability and integration challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing industry-specific customization

- 3.2.3.2 Integration with SOAR and SIEM tools

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solutions

- 5.2.1 Network performance monitoring

- 5.2.2 Network security monitoring

- 5.2.3 Network behavior analytics

- 5.2.4 Network traffic visualization

- 5.3 Services

- 5.3.1 Professional

- 5.3.1.1 Consulting

- 5.3.1.2 Deployment & integration

- 5.3.1.3 Support & maintenance

- 5.3.2 Managed

- 5.3.1 Professional

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud-based

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Security and threat detection

- 7.2.1 Intrusion detection and prevention

- 7.2.2 Advanced Persistent Threat (APT) detection

- 7.2.3 Insider threat detection

- 7.3 Performance monitoring and optimization

- 7.4 Network capacity planning

- 7.5 Anomaly detection

- 7.6 Compliance and audit

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 IT and telecom

- 9.4 Government and defense

- 9.5 Healthcare

- 9.6 Retail and e-commerce

- 9.7 Manufacturing

- 9.8 Energy and utilities

- 9.9 Education

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Arista Networks

- 11.2 Broadcom

- 11.3 Cisco Systems

- 11.4 Cloudflare

- 11.5 Dynatrace

- 11.6 ExtraHop Networks

- 11.7 Fortinet

- 11.8 Fortra

- 11.9 IBM Corporation

- 11.10 Juniper Networks

- 11.11 NEC Corporation

- 11.12 NetScout Systems

- 11.13 NTT

- 11.14 Palo Alto Networks

- 11.15 Progress Software Corporation

- 11.16 Riverbed Technology

- 11.17 SolarWinds Worldwide

- 11.18 Splunk

- 11.19 Viavi Solutions

- 11.20 Zoho Corporation

2026年全球网路流量分析市场报告2026年全球网路流量分析解决方案市场报告

2026年全球网路流量分析市场报告2026年全球网路流量分析解决方案市场报告 2026-2030年全球组织网路分析工具市场

2026-2030年全球组织网路分析工具市场 网路流量分析解决方案市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程、部署类型和最终用户划分

网路流量分析解决方案市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程、部署类型和最终用户划分 网路流量分析解决方案市场 - 全球产业规模、份额、趋势、机会、预测:按部署类型、用户类型、最终用户、地区和竞争对手划分,2021-2031 年

网路流量分析解决方案市场 - 全球产业规模、份额、趋势、机会、预测:按部署类型、用户类型、最终用户、地区和竞争对手划分,2021-2031 年 网路流量分析市场规模、份额和成长分析(按组件、部署类型、组织规模、最终用户产业和地区划分)-2026-2033年产业预测网路流量分析市场 - 全球产业规模、份额、趋势、机会和预测,按组件、部署模式、组织规模、最终用户、地区和竞争格局细分,2020-2030 年预测

网路流量分析市场规模、份额和成长分析(按组件、部署类型、组织规模、最终用户产业和地区划分)-2026-2033年产业预测网路流量分析市场 - 全球产业规模、份额、趋势、机会和预测,按组件、部署模式、组织规模、最终用户、地区和竞争格局细分,2020-2030 年预测 网路流量分析:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

网路流量分析:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 网路流量分析市场规模、份额、趋势分析报告:按组件、部署、组织规模、行业垂直、地区和细分市场进行预测,2025 年至 2030 年

网路流量分析市场规模、份额、趋势分析报告:按组件、部署、组织规模、行业垂直、地区和细分市场进行预测,2025 年至 2030 年 网路流量分析全球市场规模、份额、趋势分析报告(按组件、按部署类型、按最终用户、按组织规模、按地区、展望和预测,2024-2031 年)

网路流量分析全球市场规模、份额、趋势分析报告(按组件、按部署类型、按最终用户、按组织规模、按地区、展望和预测,2024-2031 年)