|

市场调查报告书

商品编码

1773253

瓦楞包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Corrugated Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

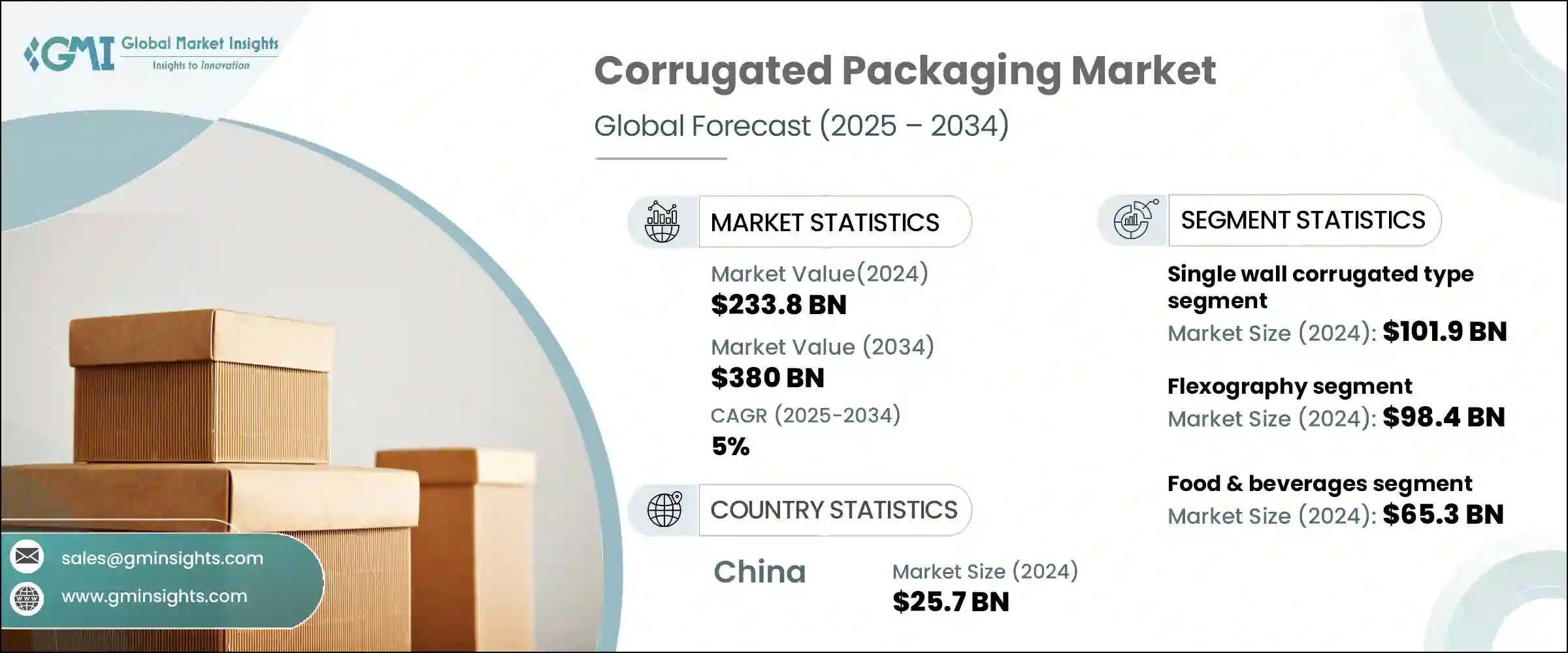

2024年,全球瓦楞包装市场规模达2,338亿美元,预计到2034年将以5%的复合年增长率成长,达到3,800亿美元。这一增长主要源于电子商务活动的蓬勃发展,以及对兼顾功能性和可持续性的现代包装解决方案的需求。该行业持续发展,采用可回收材料和环保实践,以减少其整体生态足迹。回收製程的进步、更坚固轻量化包装的开发以及再生材料的使用,正在重塑企业在数位时代的包装方式。随着全球零售业日益向线上转移,符合负责任消费概念的永续包装正变得不可或缺。

数位印刷包装在产品差异化和效率提升方面发挥关键作用。随着高解析度图形和按需生产技术的出现,营运成本得以精简,同时提升了消费者的吸引力。融合了二维码和感测器等元素的智慧包装也透过提高透明度、可追溯性和产品安全性而日益普及。随着电子商务的持续扩张,尤其是在数位优先的市场中,包装功能和创新的转变正变得越来越迅速,也越来越重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 2338亿美元 |

| 预测值 | 3800亿美元 |

| 复合年增长率 | 5% |

2024年,单壁瓦楞纸板市场价值达1,019亿美元,预计到2034年将以5.4%的复合年增长率成长。其吸引力在于轻质结构、柔韧性和价格实惠,使其成为消费性电子、零售、食品和饮料等行业的首选。单壁瓦楞纸板由两层衬板之间的单层瓦楞纸板製成,可提供经济高效的保护,并广泛应用于性能和价格同等重要的运输包装领域。

在印刷领域,柔版印刷市场在2024年的估值为984亿美元,预计在预测期内将以5.2%的复合年增长率成长。这种以高速生产和成本效益着称的印刷技术,仍然是大规模包装应用的首选。它与环保油墨的兼容性增强了其在绿色包装策略中的作用。柔版印刷支援快干工艺,并在各种材料上表现良好,这进一步增强了其在生产美观、可持续的包装解决方案方面的实用性。

2024年,中国瓦楞包装市场规模达257亿美元,预计到2034年将以5.6%的复合年增长率成长。中国市场占据主导地位,得益于其庞大的电商生态系统和先进的製造能力。持续的包装研发投入,以及向环保材料和更智慧设计的明显转变,使中国成为亚太地区的驱动力。製造商正透过提供更永续和视觉吸引力的解决方案,来适应不断变化的消费者行为和监管标准。

瓦楞包装市场的知名公司包括 Danhil、Rengo、Evergreen Packaging、Montebello Container、Cascades、Smurfit Kappa Group、Mondi Group、Georgia-Pacific、Packaging Corporation of America、CESCO、Sultana Packaging、DS Smith、Lee & Man Paper Manufacturing Corporation of America、CESCO、Sultana Packaging、DS Smith、Lee & Man Paper Manufacturing、WestnationalRock 和国际纸业 (International Papernational)。瓦楞包装领域的领先公司正在透过多项重点策略巩固其市场地位。主要措施包括扩大产能以满足日益增长的电商需求,以及投资可持续材料开发以满足更严格的环境法规。许多公司正在整合数位印刷和自动化技术,以缩短週转时间并提高设计灵活性。他们还利用与物流和零售公司的策略合作伙伴关係来改善服务交付并优化供应链。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品

- 监管格局

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- MEA

- 拉丁美洲

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依墙体类型,2021-2034

- 主要趋势

- 单壁瓦楞

- 双壁瓦楞

- 三壁瓦楞

第六章:市场估计与预测:按箱体类型,2021-2034 年

- 主要趋势

- 开槽盒

- 望远镜盒

- 硬质(幸福)盒子

- 自立箱

- 其他(内部形式、模切)

第七章:市场估计与预测:按类型,2021-2034

- 主要趋势

- A型长笛

- B型长笛

- C型长笛

- E型槽纹

- F型槽

第八章:市场估计与预测:依印刷技术,2021-2034 年

- 主要趋势

- 光刻

- 柔版印刷

- 数位印刷

- 其他(轮转凹版印刷等)

第九章:市场估计与预测:依最终用途,2021-2034

- 主要趋势

- 食品和饮料

- 个人护理和家庭护理

- 医疗的

- 家用电器和电子产品

- 农业

- 工业的

- 化学品和塑料

- 纸张和纸箱

- 其他的

第 10 章:市场估计与预测:按配销通路,2021-2034 年

- 主要趋势

- 直销

- 间接销售

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- Cascades

- CESCO

- Danhil of Mexico

- DS Smith

- Evergreen Packaging

- Georgia-Pacific

- International Paper

- Lee & Man Paper Manufacturing

- Mondi Group

- Montebello Container

- Packaging Corporation of America

- Rengo

- Smurfit Kappa Group

- Sultana Packaging

- WestRock

The Global Corrugated Packaging Market was valued at USD 233.8 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 380 billion by 2034. Much of this growth stems from rising e-commerce activity and the demand for modern packaging solutions that emphasize both functionality and sustainability. The sector continues to evolve by embracing recyclable materials and environmentally friendly practices that reduce its overall ecological footprint. Advancements in recycling processes, the development of stronger lightweight packaging, and the use of reclaimed materials are reshaping how businesses approach packaging in the digital age. With global retail increasingly shifting online, sustainable packaging that aligns with responsible consumption is becoming indispensable.

Digitally printed packaging is playing a key role in product differentiation and efficiency. With technologies enabling high-resolution graphics and on-demand production, operational costs are streamlined while enhancing consumer appeal. Smart packaging, incorporating elements like QR codes and sensors, is also gaining ground by improving transparency, traceability, and product safety. As e-commerce continues expanding-particularly in digital-first markets-the shift in packaging functionality and innovation is becoming more rapid and essential.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $233.8 Billion |

| Forecast Value | $380 Billion |

| CAGR | 5% |

The single-wall corrugated board segment was valued at USD 101.9 billion in 2024 and is forecasted to grow at 5.4% CAGR through 2034. Its appeal lies in its lightweight structure, flexibility, and affordability, making it a preferred option across sectors like consumer electronics, retail, food, and beverage. Made with a single fluted layer between two liners, it delivers cost-efficient protection and is widely used in transit packaging where performance and price matter equally.

In terms of printing, the flexography segment was valued at USD 98.4 billion in 2024 and is expected to grow at a 5.2% CAGR through the forecast period. This printing technique, known for high-speed production and cost efficiency, remains the go-to option for large-scale packaging applications. Its compatibility with eco-conscious inks enhances its role in green packaging strategies. Flexography supports fast-drying processes and performs well on varied materials, reinforcing its utility in producing visually appealing, sustainable packaging solutions.

China Corrugated Packaging Market generated USD 25.7 billion in 2024 and is projected to grow at a CAGR of 5.6% through 2034. The country's dominance is fueled by its massive e-commerce ecosystem and advanced manufacturing capabilities. Continued investment in packaging R&D and a clear shift toward eco-friendly materials and smarter designs position China as a driving force in the Asia-Pacific region. Manufacturers are now aligning with shifting consumer behavior and regulatory standards by offering more sustainable and visually engaging solutions.

Notable companies in the Corrugated Packaging Market include Danhil, Rengo, Evergreen Packaging, Montebello Container, Cascades, Smurfit Kappa Group, Mondi Group, Georgia-Pacific, Packaging Corporation of America, CESCO, Sultana Packaging, DS Smith, Lee & Man Paper Manufacturing, WestRock, and International Paper. Leading companies in the corrugated packaging space are reinforcing their market presence through several focused strategies. Key initiatives include expanding production capacity to meet growing e-commerce demands and investing in sustainable material development to meet stricter environmental regulations. Many firms are integrating digital printing and automation technologies to reduce turnaround time and improve design flexibility. Strategic partnerships with logistics and retail companies are also being leveraged to improve service delivery and optimize supply chains.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Wall type

- 2.2.3 Boxes styles

- 2.2.4 Flutes

- 2.2.5 Printing technology

- 2.2.6 End Use

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Wall Type, 2021-2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Single wall corrugated

- 5.3 Double wall corrugated

- 5.4 Triple-wall corrugated

Chapter 6 Market Estimates & Forecast, By Boxes Style, 2021-2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Slotted boxes

- 6.3 Telescope boxes

- 6.4 Rigid (bliss) boxes

- 6.5 Self-erecting boxes

- 6.6 Others (interior forms, die cut)

Chapter 7 Market Estimates & Forecast, By Flutes, 2021-2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Type A flute

- 7.3 Type B flute

- 7.4 Type C flute

- 7.5 Type E flute

- 7.6 Type F flute

Chapter 8 Market Estimates & Forecast, By Printing Technology, 2021-2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Lithography

- 8.3 Flexography

- 8.4 Digital printing

- 8.5 Others (rotogravure, etc.)

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 ($Bn, Units)

- 9.1 Key Trends

- 9.2 Food & beverages

- 9.3 Personal care & home care

- 9.4 Medical

- 9.5 Home appliances & electronics

- 9.6 Agriculture

- 9.7 Industrial

- 9.8 Chemical & plastics

- 9.9 Paper & Carton

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Cascades

- 12.2 CESCO

- 12.3 Danhil of Mexico

- 12.4 DS Smith

- 12.5 Evergreen Packaging

- 12.6 Georgia-Pacific

- 12.7 International Paper

- 12.8 Lee & Man Paper Manufacturing

- 12.9 Mondi Group

- 12.10 Montebello Container

- 12.11 Packaging Corporation of America

- 12.12 Rengo

- 12.13 Smurfit Kappa Group

- 12.14 Sultana Packaging

- 12.15 WestRock

东南亚瓦楞纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

东南亚瓦楞纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 单层纸匣全球市场规模、份额、趋势和成长分析报告(2026-2034年)

单层纸匣全球市场规模、份额、趋势和成长分析报告(2026-2034年) 日本纸盒包装市场规模、份额、趋势及预测(按材料类型、产品类型、最终用户和地区划分,2026-2034年)

日本纸盒包装市场规模、份额、趋势及预测(按材料类型、产品类型、最终用户和地区划分,2026-2034年) 2026年全球瓦楞纸包装市场报告中东和非洲瓦楞纸包装市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)北美瓦楞纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

2026年全球瓦楞纸包装市场报告中东和非洲瓦楞纸包装市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)北美瓦楞纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 瓦楞纸包装市场规模、份额和成长分析:按壁型、箱型、瓦楞数、印刷技术、最终用户、通路和地区划分-2026-2033年产业预测

瓦楞纸包装市场规模、份额和成长分析:按壁型、箱型、瓦楞数、印刷技术、最终用户、通路和地区划分-2026-2033年产业预测 快速折迭门市场按类型、操作方式、最终用途领域和区域划分

快速折迭门市场按类型、操作方式、最终用途领域和区域划分 瓦楞包装市场-全球产业规模、份额、趋势、机会和预测,按产品类型、包装类型、最终用途、地区和竞争细分,2020-2030 年预测

瓦楞包装市场-全球产业规模、份额、趋势、机会和预测,按产品类型、包装类型、最终用途、地区和竞争细分,2020-2030 年预测 瓦楞纸包装软体市场按功能、平台、用户规模和应用划分 - 全球预测 2025-2032

瓦楞纸包装软体市场按功能、平台、用户规模和应用划分 - 全球预测 2025-2032