|

市场调查报告书

商品编码

1773254

雾运算市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Fog Computing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

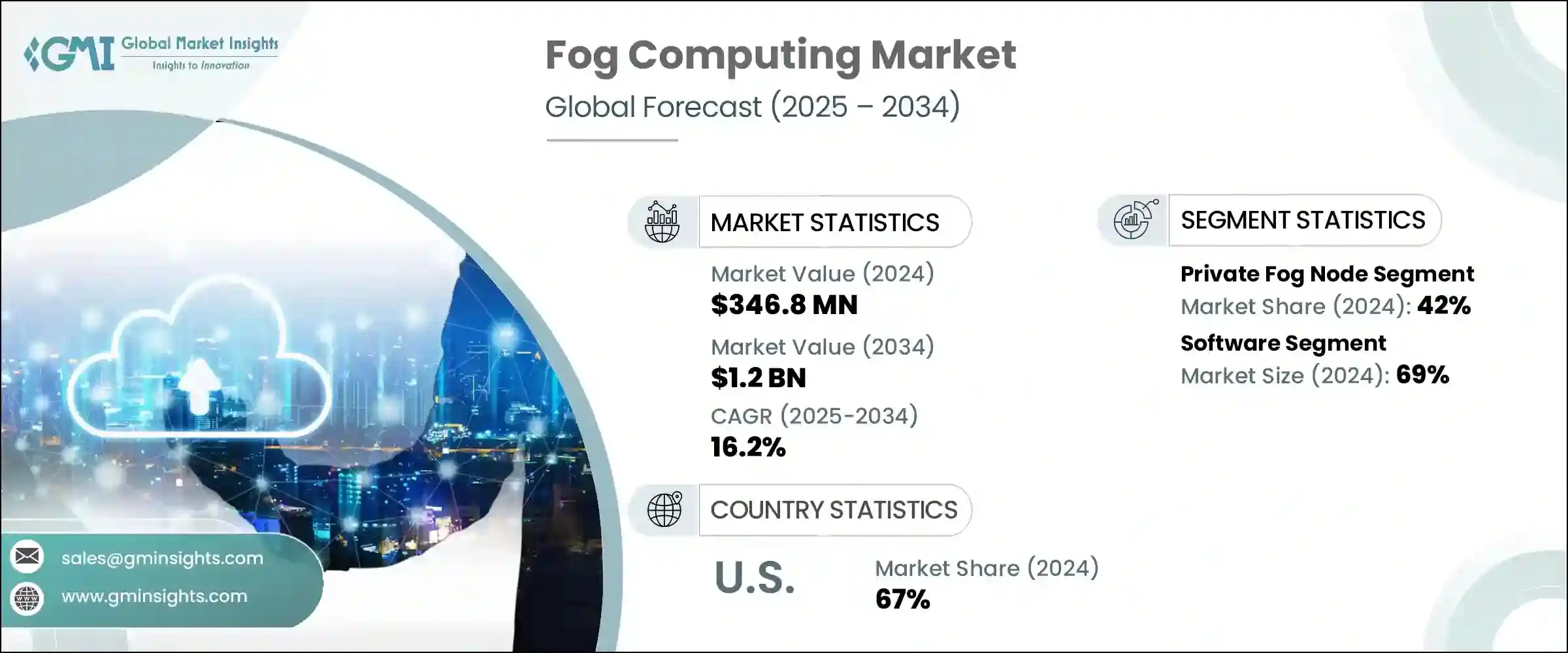

2024年,全球雾运算市场规模达3.468亿美元,预计到2034年将以16.2%的复合年增长率成长,达到12亿美元。电信、製造、智慧基础设施和医疗保健等行业对低延迟通讯、去中心化处理和即时分析的需求不断增长,推动了雾运算市场的快速扩张。随着企业持续向数位转型迈进,对靠近源头的高效能资料处理的需求也日益增长。雾运算发挥着至关重要的作用,它能够加快资料处理速度,减轻频宽压力,并透过本地运算资源增强决策能力。互联设备数量的不断增长以及对智慧化、可扩展解决方案的需求,使得雾运算成为现代边缘云端架构的核心组成部分。

雾运算支援本地储存、分析和操作,透过缩短资料传输距离,使其区别于传统的云端模型。随着越来越多的组织部署边缘系统,对能够在现场无延迟处理资料的灵活即时平台的需求正在加速成长。依赖时间敏感资料的行业,尤其是在隐私和速度至关重要的行业,正在迅速转向雾运算,将其作为可靠且安全的基础设施解决方案,连接本地营运和更广泛的云端系统。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3.468亿美元 |

| 预测值 | 12亿美元 |

| 复合年增长率 | 16.2% |

私有雾节点部署占42%的市场份额,预计到2034年将以17.2%的复合年增长率成长。这些本地化节点使企业能够更直接地控制基础设施,并提供量身定制的效能、安全性和合规性解决方案。管理关键营运或敏感资料的企业(包括医疗保健、国防和能源产业)继续青睐私有节点,因为它们能够独立、安全地处理机密工作负载,同时确保资料治理并降低延迟。

2024年,软体领域占了69%的份额。随着业界从一项小众技术发展成为边缘智慧的关键驱动力,强大的雾运算软体变得至关重要。企业越来越依赖编排工具、分析平台和虚拟化技术,这些技术能够跨复杂的边缘生态系统实现无缝管理和部署。这些平台支援跨分散式基础架构的一致性能,从而简化了依赖边缘环境快速、准确洞察的企业的营运。

美国雾运算市场占67%的市场份额,2024年市场规模达1.142亿美元。强大的数位基础设施、快速发展的创新生态系统以及日益增长的企业在地化处理需求,使美国成为该领域的领导者。雾运算如今已成为即时资料至关重要的产业营运策略中不可或缺的一部分,透过提升效率和增强即时回应能力,为企业带来竞争优势。

雾运算市场的主要公司包括施耐德、ARM Holdings、FogHorn、思科、英特尔、富士通、通用电气、微软、IBM 和戴尔。雾运算领域的公司正在利用关键策略来巩固其市场地位。与边缘设备製造商和云端服务供应商的策略合作正在帮助供应商扩大其覆盖范围,并实现跨平台的无缝整合。

企业正在大力投资研发,以开发适用于分散式环境的先进编排软体、安全协议和人工智慧自动化。针对特定行业用例(尤其是在能源、医疗保健和製造业)的雾气解决方案客製化也日益兴起。许多企业正在向混合云端-雾模型转型,以满足日益增长的性能和合规性需求。此外,与政府和智慧城市开发商的合作也正在释放新的部署机会。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 物联网设备的扩展

- 对即时资料处理和分析的需求不断增长

- 需要低延迟处理

- 5G网路的兴起

- 工业4.0的采用

- 产业陷阱与挑战

- 缺乏标准化

- 初始成本高

- 市场机会

- 物联网和边缘设备集成

- 智慧能源和公用事业

- 成长动力

- 成长潜力分析

- 监管格局

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利分析

- 成本細項分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 闸道

- 路由器和交换机

- IP摄影机

- 感应器

- 微资料感测器

- 软体

- 雾运算平台

- 客製化应用软体

第六章:市场估计与预测:依部署模型,2021 - 2034 年

- 主要趋势

- B 私有雾节点

- 社群雾节点

- 公共雾节点

- 混合雾节点

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 安全

- 智慧能源

- 智慧製造

- 交通与物流

- 互联健康

- 楼宇和家居自动化

- 其他的

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

第九章:公司简介

- ADLINK

- Amazon Web Services

- ARM Holdings

- Cisco Systems

- Cradlepoint

- Dell

- FogHorn

- Fujitsu

- GE

- Hitachi

- Huawei

- IBM

- Intel

- MachineShop

- Microsoft

- Nebbiolo

- SAP

- Schneider

- Toshiba

- Zebra

The Global Fog Computing Market was valued at USD 346.8 million in 2024 and is estimated to grow at a CAGR of 16.2% to reach USD 1.2 billion by 2034. This rapid expansion is being fueled by rising demand for low-latency communication, decentralized processing, and real-time analytics across industries such as telecom, manufacturing, smart infrastructure, and healthcare. As organizations continue to shift toward digital transformation, the need for efficient data handling closer to the source is growing. Fog computing plays a critical role by enabling faster data processing, reducing pressure on bandwidth, and enhancing decision-making through local computing resources. The increasing number of connected devices and the push for intelligent, scalable solutions are making fog computing a core component of modern edge-cloud architectures.

Fog computing enables local storage, analysis, and action, distinguishing itself from traditional cloud models by reducing the distance data must travel. As more organizations deploy edge systems, demand for flexible, real-time platforms that process data on-site without delays is accelerating. Industries relying on time-sensitive data, particularly where privacy and speed are key, are rapidly turning to fog computing as a dependable and secure infrastructure solution that bridges local operations and broader cloud systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $346.8 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 16.2% |

Private fog node deployments segment 42% share and is projected to grow at a CAGR of 17.2% through 2034. These localized nodes give enterprises more direct control over infrastructure, offering tailored performance, security, and compliance solutions. Businesses managing critical operations or sensitive data, including those in healthcare, defense, and energy, continue to favor private nodes for their ability to handle confidential workloads independently and securely while ensuring data governance and reducing latency.

The software segment held a 69% share in 2024. As industry evolves from a niche technology to a key driver of edge intelligence, robust fog computing software becomes essential. Companies increasingly rely on orchestration tools, analytics platforms, and virtualization technologies that allow seamless management and deployment across complex edge ecosystems. These platforms support consistent performance across distributed infrastructures, streamlining operations for enterprises that rely on fast, accurate insights from their edge environments.

United States Fog Computing Market held a 67% share and generated USD 114.2 million in 2024. Strong digital infrastructure, a fast-moving innovation ecosystem, and growing enterprise demand for localized processing have positioned the country as a frontrunner in this space. Fog computing is now integral to operational strategies in sectors where real-time data is vital, offering a competitive advantage through improved efficiency and immediate response capabilities.

Major companies in the Fog Computing Market include Schneider, ARM Holdings, FogHorn, Cisco, Intel, Fujitsu, GE, Microsoft, IBM, and Dell. Companies in the fog computing sector are leveraging key strategies to enhance their market foothold. Strategic collaborations with edge device manufacturers and cloud service providers are helping vendors extend their reach and enable seamless integration across platforms.

Firms are heavily investing in R&D to develop advanced orchestration software, security protocols, and AI-powered automation for distributed environments. Customization of fog solutions for industry-specific use cases, especially in energy, healthcare, and manufacturing, is also on the rise. Many businesses are transitioning toward hybrid cloud-fog models to meet growing performance and compliance demands. Additionally, partnerships with governments and smart city developers are unlocking new deployment opportunities.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of IoT devices

- 3.2.1.2 Growing demand for real-time data processing and analytics

- 3.2.1.3 Need for low-latency processing

- 3.2.1.4 Rise of 5G networks

- 3.2.1.5 Industry 4.0 adoption

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Lack of standardization

- 3.2.2.2 High initial costs

- 3.2.3 Market opportunities

- 3.2.3.1 IoT and edge device integration

- 3.2.3.2 Smart energy and utilities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Gateways

- 5.2.2 Routers & switches

- 5.2.3 IP video cameras

- 5.2.4 Sensors

- 5.2.5 Micro data sensors

- 5.3 Software

- 5.3.1 Fog computing platform

- 5.3.2 Customized application software

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 B Private fog node

- 6.3 Community fog node

- 6.4 Public fog node

- 6.5 Hybrid fog node

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Security

- 7.3 Intelligent energy

- 7.4 Smart manufacturing

- 7.5 Traffic & logistics

- 7.6 Connected health

- 7.7 Building & home automation

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 ADLINK

- 9.2 Amazon Web Services

- 9.3 ARM Holdings

- 9.4 Cisco Systems

- 9.5 Cradlepoint

- 9.6 Dell

- 9.7 FogHorn

- 9.8 Fujitsu

- 9.9 GE

- 9.10 Hitachi

- 9.11 Huawei

- 9.12 IBM

- 9.13 Intel

- 9.14 MachineShop

- 9.15 Microsoft

- 9.16 Nebbiolo

- 9.17 SAP

- 9.18 Schneider

- 9.19 Toshiba

- 9.20 Zebra

2026年全球雾计算市场报告

2026年全球雾计算市场报告 雾运算市场 - 全球产业规模、份额、趋势、机会及预测(按组件、部署模式、应用、地区和竞争格局划分,2021-2031年)

雾运算市场 - 全球产业规模、份额、趋势、机会及预测(按组件、部署模式、应用、地区和竞争格局划分,2021-2031年) 雾运算市场规模、份额、趋势及预测(按组件、部署模型、应用和地区),2025 年至 2033 年

雾运算市场规模、份额、趋势及预测(按组件、部署模型、应用和地区),2025 年至 2033 年 雾运算市场:2025-2029 年全球市场

雾运算市场:2025-2029 年全球市场 雾计算市场规模、份额、成长分析,按类型、应用、地区 - 产业预测,2024-2031 年

雾计算市场规模、份额、成长分析,按类型、应用、地区 - 产业预测,2024-2031 年 全球雾计算市场规模、份额和趋势分析报告(按组件、按应用、按地区、展望和预测,2024-2031)

全球雾计算市场规模、份额和趋势分析报告(按组件、按应用、按地区、展望和预测,2024-2031) 雾计算市场规模、份额、趋势分析报告:按组件、按应用、按地区、细分市场预测,2024-2030 年

雾计算市场规模、份额、趋势分析报告:按组件、按应用、按地区、细分市场预测,2024-2030 年 2024 年至 2031 年雾计算市场规模(按类型、应用和地区划分)

2024 年至 2031 年雾计算市场规模(按类型、应用和地区划分)