|

市场调查报告书

商品编码

1773255

电动车绝缘市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Electric Vehicle Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

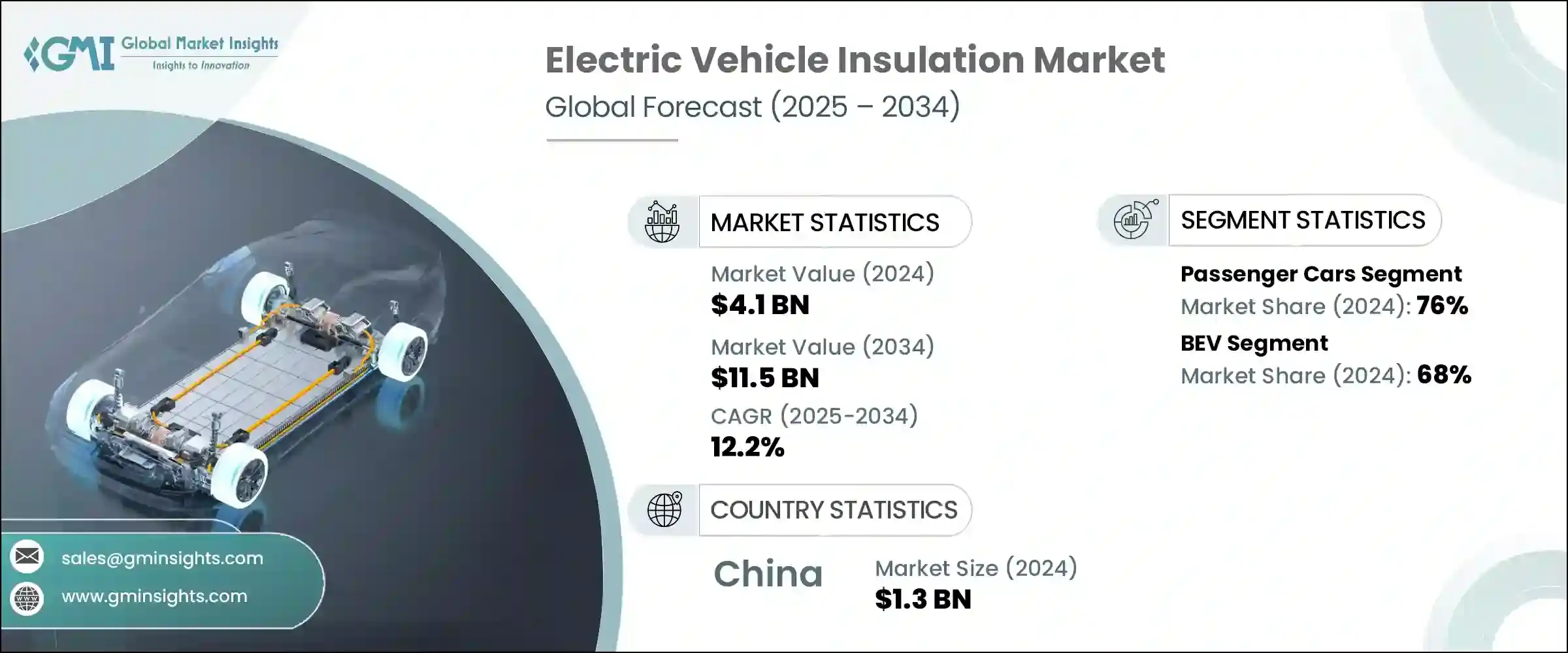

2024年,全球电动车绝缘材料市场规模达41亿美元,预计2034年将以12.2%的复合年增长率成长,达到115亿美元。电动车的普及以及全球充电网路的建设,正在显着影响先进绝缘材料的需求。随着电动车日益成为主流,绝缘材料在汽车中发挥着比传统汽车更为重要的作用——它对于热量管理、确保电气完整性以及创造更安静的座舱环境至关重要。电动传动系统日益复杂且紧凑,不仅要求材料能够耐高温,还要求其能够在高压环境下保持电气隔离。从控制电池温度到屏蔽电子元件,绝缘材料对于提高车辆效率、可靠性和长期安全性至关重要。

热管理是电动车工程的核心重点,尤其是在製造商追求更高电池容量和更快充电週期的当下。为了满足这些需求,市场对兼具高耐热性和轻量化设计的材料表现出浓厚的兴趣。由于电动传动系统的工作电压通常高达 800V,绝缘材料不仅必须能够承受极端的温度梯度,还必须在重复的热循环下保持稳定的性能。随着越来越多的汽车製造商竞相提升续航里程、耐用性和驾驶体验,绝缘材料的设计不再仅仅作为一道屏障,而成为整合在电池模组、电动马达和电力电子设备中的性能赋能器。新型电动车平台的开发越来越注重在紧凑设计与有效的热量和噪音控制之间取得平衡,这使得绝缘材料成为车辆安全和性能标准的核心。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 41亿美元 |

| 预测值 | 115亿美元 |

| 复合年增长率 | 12.2% |

在动力系统方面,纯电动车 (BEV) 在 2024 年占据市场主导地位,约占全球市场份额的 68%。预计该细分市场在 2025 年至 2034 年期间的复合年增长率将超过 13.1%。 BEV 完全依赖电力驱动,这加剧了对所有高压和热敏感部件进行全面绝缘的需求。由于 BEV 包含大型电池组,并在运行和充电过程中产生大量热量,因此对能够保持稳定温度并防止能量损失的材料的需求持续增长。 BEV 中的绝缘材料还可以隔离电场并减少电磁干扰,从而进一步提高电气系统的效率和安全性。随着原始设备製造商 (OEM) 探索更紧凑、更高能量密度的电池配置,绝缘解决方案也正在优化,以实现紧密整合、轻量化和高性能。

按产品类别划分,隔热材料在2024年占据主导地位,预计在整个预测期内仍将保持领先地位。隔热材料对于电动车至关重要,能够有效管理关键系统的温度均匀性。过热风险和能源效率低下会危及车辆安全和电池寿命,因此高性能隔热材料被广泛采用。这些材料如今已成为保护电池免受热量积聚、保持电力电子设备最佳性能以及在极端运行条件下保障乘客安全的关键。随着电动车技术的成熟,隔热材料必须跟上快速充电系统和日益紧凑的电池组件不断增长的散热需求。

从区域来看,2024年中国约占亚太地区电动车绝缘市场的68.3%,贡献了约13亿美元的收入。中国仍然处于全球电动车生产的前沿,拥有高度发展的本地供应链和对电动车技术的积极投资。其製造规模加上强劲的国内需求,使中国成为推动绝缘材料创新和大规模部署的主导力量。在区域製造商专注于扩大产能和提升产品性能的同时,全球公司也在该地区投资,以支持本地和出口市场。随着车辆架构的演变和性能标准的日益严格,预计各类电动车对专用绝缘材料的需求将大幅成长。

随着车辆架构的不断变化以及人们对能源效率和乘客舒适度日益增长的期望,电动车绝缘市场正在迅速转型。随着电动车日益复杂,绝缘系统不仅要保护零件,还必须主动管理热量、降低噪音,并在紧凑的动力总成环境中隔离电流。绝缘材料已成为支援下一代电动车功能的关键,包括高压传动系统、模组化电池系统和安静的座舱体验。目前,轻量、高耐用性的材料正在开发中,以改善能源利用并延长续航里程。这些解决方案旨在无缝整合到电动车的结构设计中,帮助汽车製造商满足性能、安全性和监管目标。随着全球电动车的加速发展,绝缘材料将继续成为永续高效车辆系统的关键推动因素。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 电动车产量不断成长

- 扩大电动车充电基础设施

- 材料技术的进步

- 政府激励措施和投资不断增加

- 产业陷阱与挑战

- 复杂的客製化需求

- 来自整合热管理解决方案的竞争

- 市场机会

- 关注电池安全及防火

- 轻质材料需求不断成长

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品

- 生产统计

- 生产中心

- 消费中心

- 汇出和汇入

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 轿车

- 掀背车

- 越野车

- 商用车

- 轻型

- 中型

- 重负

- 两轮车

第六章:市场估计与预测:以推进方式,2021 - 2034 年

- 主要趋势

- 纯电动车

- 插电式混合动力

- 油电混合车

- 燃料电池电动车

第七章:市场估计与预测:依产品,2021 - 2034 年

- 主要趋势

- 隔热

- 隔音

- 电绝缘

- 杂交种

第八章:市场估计与预测:按材料,2021 - 2034 年

- 主要趋势

- 热介面

- 泡沫塑胶

- 陶瓷材料

- 玻璃棉/玻璃纤维

- 硅和橡胶基

- 其他的

第九章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 电池组和外壳

- 电动机

- 电力电子

- 客舱

- 引擎盖下/热管理系统

- 充电埠和系统

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧人

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- 3M

- Aerofoam (Hira Industries)

- Armacell International

- Autoneum

- BASF SE

- Covestro AG

- DuPont

- Flex

- ITW Formex

- Johns Manville (Berkshire Hathaway)

- L&L Products

- Morgan Advanced Materials

- Parker Hannifin

- Polymer Technologies

- Rogers Corporation

- Saint-Gobain

- Toray Industries

- UBE Corporation

- Unifrax (Alkegen)

- Zotefoams

The Global Electric Vehicle Insulation Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 12.2% to reach USD 11.5 billion by 2034. The increasing shift toward electric mobility and the global ramp-up of charging networks are significantly influencing the demand for advanced insulation materials. As EVs become more mainstream, insulation is playing a far more central role than in traditional vehicles-it is now critical to managing heat, ensuring electrical integrity, and supporting quieter cabin environments. The growing complexity and compactness of electric drivetrains require materials that not only resist high heat but also maintain electrical separation in high-voltage environments. From controlling battery temperatures to shielding electronic components, insulation is becoming essential in enhancing vehicle efficiency, reliability, and long-term safety.

Thermal management is a core priority in EV engineering, especially as manufacturers push for higher battery capacities and faster charging cycles. To meet these demands, the market is seeing strong interest in materials that offer both high thermal resistance and lightweight design. With electric drivetrains often operating at voltages up to 800V, insulation must not only withstand extreme thermal gradients but also maintain stable performance under repeated thermal cycling. As more automakers compete to improve range, durability, and driver experience, insulation is being engineered not just as a barrier but as a performance enabler integrated across battery modules, electric motors, and power electronics. The development of new EV platforms is increasingly focused on balancing compact design with effective heat and noise control, which places insulation at the center of vehicle safety and performance standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 12.2% |

In terms of propulsion, Battery Electric Vehicles (BEVs) led the market in 2024, accounting for approximately 68% of the global share. This segment is projected to expand at a CAGR of more than 13.1% from 2025 to 2034. BEVs rely entirely on electric power, which intensifies the need for comprehensive insulation across all high-voltage and thermally sensitive components. Since BEVs contain large battery packs and generate considerable heat during operation and charging, the demand for materials capable of maintaining stable temperatures and preventing energy loss continues to grow. Insulation in BEVs also serves to isolate electric fields and reduce electromagnetic interference, which further improves the efficiency and safety of electric systems. As OEMs explore more compact and high-energy-density battery configurations, insulation solutions are being optimized for tight integration, minimal weight, and high performance.

By product, the thermal insulation segment held the dominant share in 2024 and is expected to maintain its lead through the forecast period. Thermal insulation is essential in EVs to manage temperature uniformity across critical systems. Overheating risks and energy inefficiencies can compromise both vehicle safety and battery life, which has led to widespread adoption of high-performance thermal barriers. These materials are now fundamental to shielding batteries from heat buildup, preserving optimal performance of power electronics, and maintaining passenger safety under extreme operating conditions. As EV technology matures, thermal insulation must keep pace with rising thermal demands from fast-charging systems and increasingly compact battery assemblies.

Regionally, China represented about 68.3% of the Asia-Pacific EV insulation market in 2024, contributing approximately USD 1.3 billion in revenue. The country remains at the forefront of global EV production, with a highly developed local supply chain and aggressive investment in EV technologies. Its scale of manufacturing, combined with strong domestic demand, has made China a dominant force in driving innovation and mass deployment of insulation materials. While regional manufacturers are focused on expanding capacity and improving product performance, global companies are also investing in the region to support both local and export markets. As vehicle architectures evolve and performance standards grow more stringent, the demand for specialized insulation materials across all types of electric vehicles is expected to rise significantly.

The electric vehicle insulation market is transforming rapidly in response to shifting vehicle architectures and rising expectations for energy efficiency and passenger comfort. As EVs grow more complex, insulation systems must do more than just protect components-they must actively manage heat, reduce noise, and isolate electrical currents within tightly packed powertrain environments. Insulation has become instrumental in supporting next-generation EV features, including high-voltage drivetrains, modular battery systems, and quiet cabin experiences. Lightweight, high-durability materials are now being developed to improve energy use and extend driving range. These solutions are designed for seamless integration into the structural design of EVs, helping automakers meet performance, safety, and regulatory targets. With electric mobility accelerating worldwide, insulation will continue to be a key enabler of sustainable and efficient vehicle systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Product

- 2.2.5 Material

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising electric vehicle production

- 3.2.1.2 Expansion of EV charging infrastructure

- 3.2.1.3 Advancements in material technology

- 3.2.1.4 Rising government incentives and investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex customization needs

- 3.2.2.2 Competition from integrated thermal management solutions

- 3.2.3 Market opportunities

- 3.2.3.1 Focus on battery safety and fire protection

- 3.2.3.2 Rising demand for light weight materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

- 5.4 Two-wheelers

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 BEV

- 6.3 PHEV

- 6.4 HEV

- 6.5 FCEV

Chapter 7 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Thermal insulation

- 7.3 Acoustic insulation

- 7.4 Electric insulation

- 7.5 Hybrid

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Thermal interface

- 8.3 Foamed plastics

- 8.4 Ceramic materials

- 8.5 Glass wool/Fiberglass

- 8.6 Silicon and Rubber-based

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Battery pack and housing

- 9.3 Electric motor

- 9.4 Power electronics

- 9.5 Passenger cabin

- 9.6 Under the hood/thermal management system

- 9.7 Charging port & system

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3M

- 11.2 Aerofoam (Hira Industries)

- 11.3 Armacell International

- 11.4 Autoneum

- 11.5 BASF SE

- 11.6 Covestro AG

- 11.7 DuPont

- 11.8 Flex

- 11.9 ITW Formex

- 11.10 Johns Manville (Berkshire Hathaway)

- 11.11 L&L Products

- 11.12 Morgan Advanced Materials

- 11.13 Parker Hannifin

- 11.14 Polymer Technologies

- 11.15 Rogers Corporation

- 11.16 Saint-Gobain

- 11.17 Toray Industries

- 11.18 UBE Corporation

- 11.19 Unifrax (Alkegen)

- 11.20 Zotefoams

全球电动汽车绝缘材料市场规模、份额、趋势和成长分析报告(2026-2034年)

全球电动汽车绝缘材料市场规模、份额、趋势和成长分析报告(2026-2034年) 引擎室隔热垫市场按材料、厚度、车辆类型和分销管道划分,全球预测(2026-2032年)汽车声学密封市场材料类型、产品形式、车辆类型和安装类型划分,全球预测(2026-2032年)汽车门板隔音材料市场:依材料类型、材料技术、车辆类型、厚度和应用划分-全球预测,2026-2032年

引擎室隔热垫市场按材料、厚度、车辆类型和分销管道划分,全球预测(2026-2032年)汽车声学密封市场材料类型、产品形式、车辆类型和安装类型划分,全球预测(2026-2032年)汽车门板隔音材料市场:依材料类型、材料技术、车辆类型、厚度和应用划分-全球预测,2026-2032年 汽车隔热材料市场规模、份额和成长分析(按材料类型、车辆类型、应用、零件、分销管道和地区划分)-2026-2033年产业预测

汽车隔热材料市场规模、份额和成长分析(按材料类型、车辆类型、应用、零件、分销管道和地区划分)-2026-2033年产业预测 2025年全球汽车隔音部件市场报告

2025年全球汽车隔音部件市场报告 电动汽车绝缘市场:2024-2031年全球产业分析、规模、占有率、成长、趋势、预测

电动汽车绝缘市场:2024-2031年全球产业分析、规模、占有率、成长、趋势、预测 全球电动车绝缘市场规模研究,按应用、按推进类型、按车辆类型、按材料类型、按绝缘类型和 2022-2032 年区域预测

全球电动车绝缘市场规模研究,按应用、按推进类型、按车辆类型、按材料类型、按绝缘类型和 2022-2032 年区域预测