|

市场调查报告书

商品编码

1773266

医用 X 光市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Medical X-ray Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

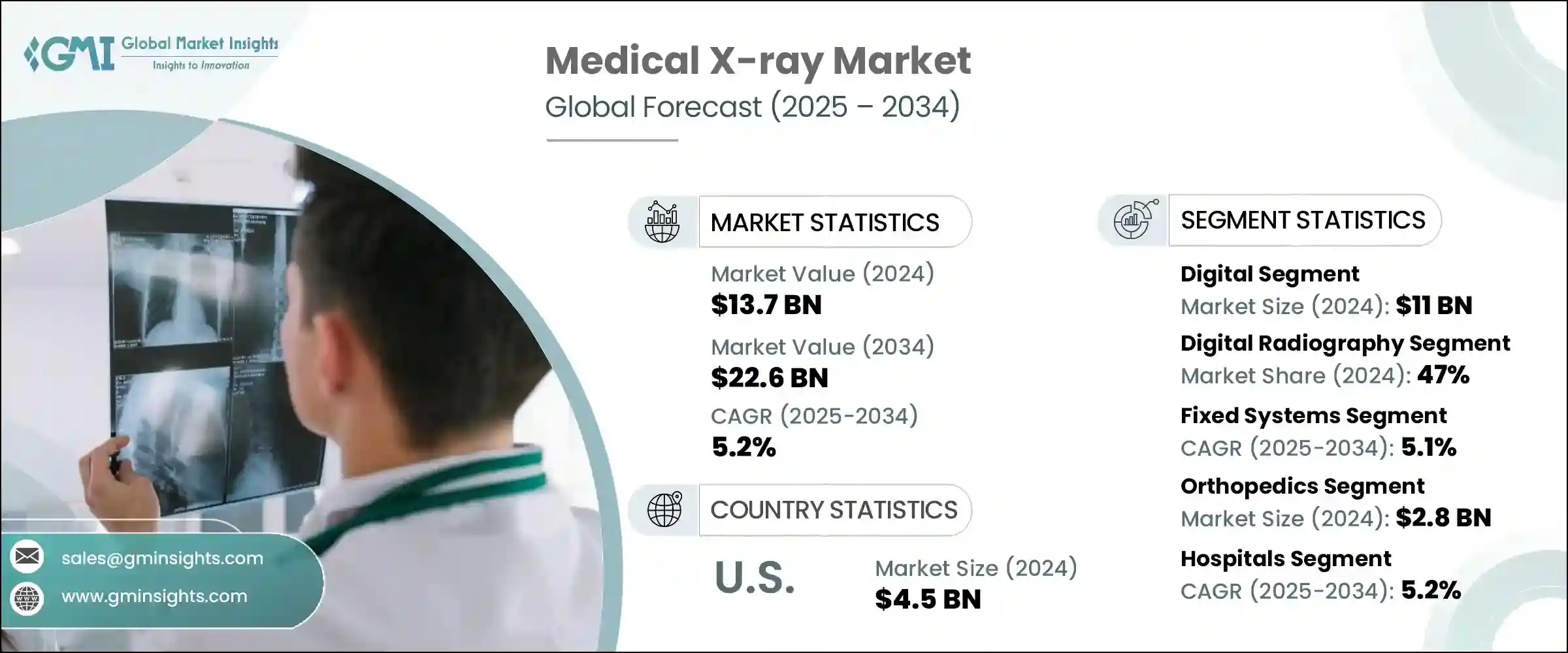

2024 年全球医用 X 光市场规模为 137 亿美元,预计到 2034 年将以 5.2% 的复合年增长率成长,达到 226 亿美元。对医疗 X 光设备的需求主要源自于癌症、心血管疾病、呼吸系统疾病、神经系统疾病和肌肉骨骼疾病等慢性疾病发生率的上升。随着越来越多的患者需要对这些疾病进行早期和准确的诊断,医用 X 光机已成为必不可少的诊断工具。 X 光影像有助于检测骨骼、器官和组织中的肿瘤、骨折和异常情况。全球人口的成长和老化也导致对诊断影像的需求增加,尤其是对老年患者与年龄相关的疾病的需求。这些因素共同推动了市场扩张。

此外,医用X光在诊断各种慢性病和其他医疗问题方面发挥着至关重要的作用。它们能够提供人体内部结构(例如骨骼、器官和软组织)的高解析度影像,这对于识别骨折、肿瘤、感染以及各器官的异常至关重要。这些详细的影像有助于医生评估损伤或疾病的严重程度,监测正在进行的治疗,并在必要时规划手术干预。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 137亿美元 |

| 预测值 | 226亿美元 |

| 复合年增长率 | 5.2% |

此外,X光技术在早期诊断中不可或缺,它使医疗保健提供者能够在问题发展成更严重的健康风险之前发现它们。 X光技术的非侵入性特性和提供精确结果的能力使其成为准确诊断和有效治疗计划不可或缺的工具。随着数位X光系统的进步,影像清晰度和诊断能力不断提高,使医生更容易做出明智的病患照护决策。

受数位系统技术创新的推动,数位X射线领域在2024年创造了110亿美元的市场规模。数位X光设备提供卓越的成像能力,解析度高、对比度更高,这对于精准诊断至关重要。其快速撷取和处理影像的能力显着缩短了患者的等待时间。此外,人工智慧成像解决方案等技术进步正在提高诊断效率和结果的一致性。这些特性促进了数位X射线技术在医疗机构中的广泛应用。在放射影像学方面,数位系统日益普及,这主要得益于其与现代IT基础设施的集成,从而改善了资料管理和可访问性。

预计到2034年,医院产业的复合年增长率将达到5.2%。无论是在发展中地区或已开发地区,医院数量的成长都受到人口成长、慢性病盛行率上升以及医学影像技术的进步等因素的推动。这些因素共同推动了新建医院和现有医疗机构对先进医用X光系统的需求。此外,中东、非洲和亚太等地区医疗基础设施的不断扩张,也加速了先进医用X光技术在医院环境中的应用。

2024年,欧洲医用X射线市场规模达38亿美元。这一增长主要得益于慢性病发病率的上升以及该地区各国政府持续改善医疗基础设施的努力。此外,X射线技术的进步,尤其是数位和便携式系统的进步,将进一步推动欧洲市场的成长。该地区主要市场参与者的存在也增强了欧洲的竞争优势。在该地区营运的公司正在积极投资创新解决方案,并不断升级其产品,从而促进市场的整体扩张。

全球医用X射线市场的主要参与者包括爱克发-吉华集团、艾伦格斯医疗系统、佳能、锐珂医疗、登士柏西诺德、富士软片控股公司、通用电气医疗科技、豪洛捷、荷兰皇家飞利浦、柯尼卡美能达、Midmark、东软医疗系统、普朗医疗设备、三星皇家飞利浦、柯尼卡美能达、Midmark、东软医疗系统、普朗医疗设备、三星、三星医疗公司、三星西门)众多电子公司。为了巩固其在竞争激烈的医用X射线市场中的地位,各公司正专注于多项策略倡议。他们大力投资研发,旨在为市场带来先进的影像解决方案,例如具有人工智慧功能的数位X射线系统,可提高诊断的准确性。

此外,各公司正优先考虑将其产品与IT基础设施集成,以实现更好的资料存取、储存和管理。许多公司也正在开发便携式和无线X射线系统,为医疗保健提供者提供更大的灵活性和便利性。透过数位射线成像解决方案降低成本,无需传统的胶片冲洗,是吸引註重成本的机构的另一项策略。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 已开发国家诊断影像技术的进步

- 全球慢性病盛行率不断上升

- 诊断成像程序的数量不断增加

- 医疗 X 光检查的报销情况

- 产业陷阱与挑战

- 高辐射暴露的风险

- 安装医学影像设备的成本高昂

- 市场机会

- 越来越多地使用低剂量X射线技术来最大限度地减少辐射暴露,同时保持高影像品质。

- 对人工智慧整合 X 光系统的需求不断增加,以增强影像解释能力并减少诊断错误。

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 数位的

- 模拟

第六章:市场估计与预测:按技术,2021 - 2034 年

- 主要趋势

- 底片放射照相术

- 电脑放射成像

- 数位射线照相术

第七章:市场估计与预测:按便携性,2021 - 2034

- 主要趋势

- 固定係统

- 便携式系统

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 牙科

- 口内成像

- 口外成像

- 兽医

- 肿瘤学

- 骨科

- 心臟病学

- 神经病学

- 其他兽医应用

- 乳房X光检查

- 胸部

- 心血管

- 骨科

- 其他应用

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 诊断中心

- 其他最终用途

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 越南

- 韩国

- 泰国

- 大洋洲

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 埃及

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Agfa-Gevaert Group

- Allengers Medical Systems

- Canon

- Carestream Health

- Dentsply Sirona

- Fujifilm Holdings Corporation

- GE HealthCare Technologies

- Hologic

- Koninklijke Philips NV

- Konica Minolta

- Midmark

- Neusoft Medical Systems

- Perlong Medical Equipment

- Samsung Electronics

- Shimadzu

- Siemens Healthineers

- Trivitron Healthcare

The Global Medical X-ray Market was valued at USD 13.7 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 22.6 billion by 2034. The demand for medical X-ray devices is primarily driven by the rising prevalence of chronic diseases, including cancer, cardiovascular issues, respiratory conditions, neurological disorders, and musculoskeletal problems. As more patients require early and precise diagnoses for these conditions, medical X-ray machines have become an essential diagnostic tool. X-ray imaging helps detect tumors, fractures, and abnormalities in bones, organs, and tissues. The growing and aging global population is also contributing to the rise in the need for diagnostic imaging, particularly for age-related conditions in elderly patients. These factors combine to fuel the market's expansion.

Additionally, medical X-rays play a vital role in diagnosing a wide range of chronic conditions and other medical issues. They provide high-resolution images of the body's internal structures, such as bones, organs, and soft tissues, which are essential for identifying fractures, tumors, infections, and abnormalities in various organs. These detailed images help physicians assess the severity of injuries or diseases, monitor ongoing treatments, and plan surgical interventions if necessary.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.7 Billion |

| Forecast Value | $22.6 Billion |

| CAGR | 5.2% |

Furthermore, X-ray technology is indispensable in early detection, allowing healthcare providers to identify problems before they develop into more serious health risks. Its non-invasive nature and ability to deliver precise results make it an indispensable tool for accurate diagnosis and effective treatment planning. With advancements in digital X-ray systems, image clarity, and diagnostic capabilities continue to improve, making it easier for doctors to make informed decisions about patient care.

The digital X-ray segment generated USD 11 billion in 2024 driven by technological innovations in digital systems. Digital X-ray devices offer superior imaging capabilities with high resolution and better contrast, critical for accurate diagnoses. Their ability to quickly capture and process images significantly reduces patient waiting times. Furthermore, advancements like AI-powered imaging solutions are increasing the efficiency and consistency of diagnostic results. These features contribute to the widespread adoption of digital X-ray technology across healthcare facilities. In terms of radiography, digital systems have become increasingly popular, mainly due to their integration with modern IT infrastructure, which improves data management and accessibility.

The hospital segment is expected to grow at a CAGR of 5.2% through 2034. The growth in the number of hospitals, both in developing and developed regions, is being driven by factors such as population growth, the increasing prevalence of chronic diseases, and advancements in medical imaging technologies. These factors are collectively fueling the demand for state-of-the-art medical X-ray systems, both in newly built hospitals and within existing healthcare facilities. Additionally, the expanding healthcare infrastructure in regions like the Middle East, Africa, and Asia Pacific is accelerating the adoption of advanced medical X-ray technologies in hospital settings.

Europe Medical X-ray market was valued at USD 3.8 billion in 2024. This growth can be attributed to the rising incidence of chronic diseases and the ongoing efforts by governments in the region to improve healthcare infrastructure. Additionally, advancements in X-ray technology, particularly in digital and portable systems, will further drive market growth in Europe. The presence of major market players in the region also strengthens Europe's competitive edge. Companies operating in the region are actively investing in innovative solutions and continuously upgrading their offerings, contributing to the overall expansion of the market.

The key players in the Global Medical X-ray market include a diverse range of companies such as Agfa-Gevaert Group, Allengers Medical Systems, Canon, Carestream Health, Dentsply Sirona, Fujifilm Holdings Corporation, GE Healthcare Technologies, Hologic, Koninklijke Philips N.V., Konica Minolta, Midmark, Neusoft Medical Systems, Perlong Medical Equipment, Samsung Electronics, Shimadzu, Siemens Healthineers, and Trivitron Healthcare. To solidify their position in the competitive medical X-ray market, companies are focusing on several strategic initiatives. They are heavily investing in research and development to bring advanced imaging solutions to the market, such as digital X-ray systems with AI capabilities that enhance diagnostic accuracy.

Additionally, companies are prioritizing the integration of their products with IT infrastructure, allowing for better data accessibility, storage, and management. Many players are also developing portable and wireless X-ray systems to offer greater flexibility and convenience to healthcare providers. Cost reduction through digital radiography solutions, which eliminate the need for traditional film processing, is another strategy being employed to appeal to cost-conscious institutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Market scope and definitions

- 1.3 Research design

- 1.3.1 Research approach

- 1.3.2 Data collection methods

- 1.4 Data mining sources

- 1.4.1 Global

- 1.4.2 Regional/Country

- 1.5 Base estimates and calculations

- 1.5.1 Base year calculation

- 1.5.2 Key trends for market estimation

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Portability

- 2.2.5 Application

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements in diagnostic imaging in developed countries

- 3.2.1.2 Rising prevalence of chronic diseases worldwide

- 3.2.1.3 Growing number of diagnostic imaging procedures

- 3.2.1.4 Presence of reimbursement for medical x-ray procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of high radiation exposure

- 3.2.2.2 High cost associated with installation of medical imaging modalities

- 3.2.3 Market opportunities

- 3.2.3.1 Growing use of low-dose X-ray technologies to minimize radiation exposure while maintaining high image quality.

- 3.2.3.2 Increasing demand for AI-integrated X-ray systems to enhance image interpretation and reduce diagnostic errors.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Digital

- 5.3 Analog

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Film-based radiography

- 6.3 Computed radiography

- 6.4 Digital radiography

Chapter 7 Market Estimates and Forecast, By Portability, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Fixed systems

- 7.3 Portable systems

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Dental

- 8.2.1 Intraoral imaging

- 8.2.2 Extraoral imaging

- 8.3 Veterinary

- 8.3.1 Oncology

- 8.3.2 Orthopedics

- 8.3.3 Cardiology

- 8.3.4 Neurology

- 8.3.5 Other veterinary applications

- 8.4 Mammography

- 8.5 Chest

- 8.6 Cardiovascular

- 8.7 Orthopedics

- 8.8 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Diagnostic centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Vietnam

- 10.4.5 South Korea

- 10.4.6 Thailand

- 10.4.7 Oceania

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Egypt

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Agfa-Gevaert Group

- 11.2 Allengers Medical Systems

- 11.3 Canon

- 11.4 Carestream Health

- 11.5 Dentsply Sirona

- 11.6 Fujifilm Holdings Corporation

- 11.7 GE HealthCare Technologies

- 11.8 Hologic

- 11.9 Koninklijke Philips N.V.

- 11.10 Konica Minolta

- 11.11 Midmark

- 11.12 Neusoft Medical Systems

- 11.13 Perlong Medical Equipment

- 11.14 Samsung Electronics

- 11.15 Shimadzu

- 11.16 Siemens Healthineers

- 11.17 Trivitron Healthcare

2026年全球X射线系统市场报告2026年全球医用行动X光设备市场报告2026年全球诊断X光系统市场报告

2026年全球X射线系统市场报告2026年全球医用行动X光设备市场报告2026年全球诊断X光系统市场报告 X射线系统市场分析及预测(至2035年):依类型、产品类型、技术、应用、组件、最终用户、服务、安装类型、模式及功能划分

X射线系统市场分析及预测(至2035年):依类型、产品类型、技术、应用、组件、最终用户、服务、安装类型、模式及功能划分 负像仪市场 - 全球产业规模、份额、趋势、机会及预测(按型号、光源、应用、最终用户、地区和竞争格局划分),2021-2031年

负像仪市场 - 全球产业规模、份额、趋势、机会及预测(按型号、光源、应用、最终用户、地区和竞争格局划分),2021-2031年 ≥5MHU CT 管路市场依产品类型、材料、自动化程度、最终用途及通路划分,全球预测,2026-2032 年携带式数位微欧姆表市场:按技术、类型、应用和分销管道划分,全球预测(2026-2032年)

≥5MHU CT 管路市场依产品类型、材料、自动化程度、最终用途及通路划分,全球预测,2026-2032 年携带式数位微欧姆表市场:按技术、类型、应用和分销管道划分,全球预测(2026-2032年) 医用X射线市场规模、份额和成长分析(按类型、技术、行动装置、应用、最终用途和地区划分)-2026-2033年产业预测

医用X射线市场规模、份额和成长分析(按类型、技术、行动装置、应用、最终用途和地区划分)-2026-2033年产业预测 X光市场按模式、产品类型、技术、应用、最终用户和地区划分医用X射线产生器市场按类型、频率类型、技术、应用和最终用户划分-2025-2032年全球预测

X光市场按模式、产品类型、技术、应用、最终用户和地区划分医用X射线产生器市场按类型、频率类型、技术、应用和最终用户划分-2025-2032年全球预测