|

市场调查报告书

商品编码

1773322

肽基奈米材料市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Peptide-Based Nanomaterials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

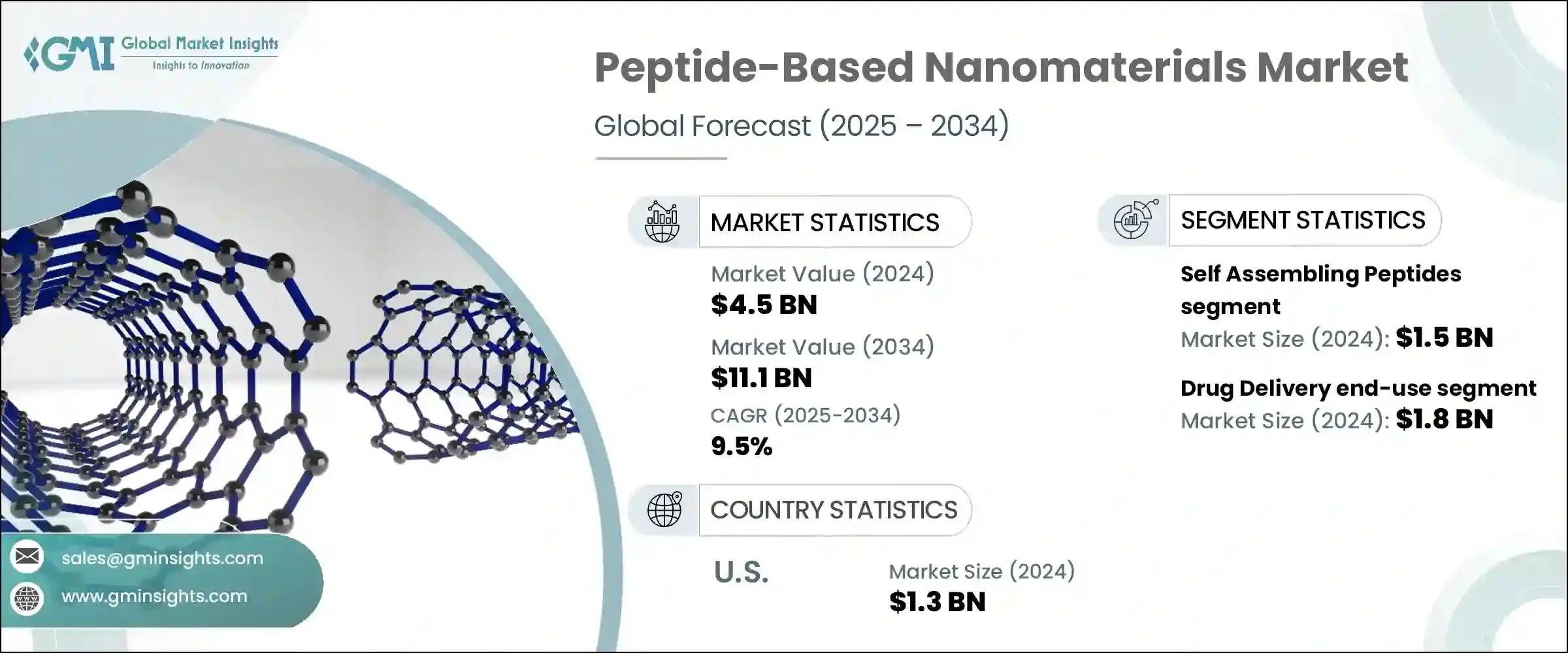

2024年,全球肽基奈米材料市场规模达45亿美元,预计到2034年将以9.5%的复合年增长率成长,达到111亿美元。随着医疗产业向精准医疗和标靶治疗转型,该市场发展势头强劲。肽基奈米材料因其在药物传输、成像、透皮治疗和组织工程方面的多功能特性而备受关注。它们能够作为生物相容性的药物载体,并支持先进的治疗平台,使其成为传统疗法的极具吸引力的替代方案。私人投资和政府资金的不断增加正在加速奈米医学的创新步伐。

全球医疗保健体係正在不断发展,重新重视先进的医疗工具、生物响应材料和奈米级疗法,这些疗法疗效更佳,副作用更少。对智慧药物系统(尤其是能够定位并最大程度减少对健康组织的暴露)的需求日益增长,极大地促进了这些技术的普及。此外,投资者和公共医疗机构对生物製药创新的兴趣日益浓厚,催生了专门的检测系统、智慧型药物配製方法和模组化奈米结构,旨在彻底改变疾病在分子层面的治疗方式。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 45亿美元 |

| 预测值 | 111亿美元 |

| 复合年增长率 | 9.5% |

自组装胜肽领域在2024年创造了15亿美元的市场规模,预计到2034年将以8.7%的复合年增长率成长。该领域的普及得益于对控释和定点递送系统日益增长的需求。目前有超过300种肽基载体处于临床前或临床阶段,标靶治疗(尤其是癌症和基因治疗)是关键的成长领域。研发人员正致力于开发生物相容性和可生物降解的胜肽奈米结构,以实现更安全的药物运输。创新如今正蔓延到诊断和分子影像等相关领域,这些领域正受到研究人员和监管机构的广泛关注。

2024年,药物递送应用领域的市场价值达18亿美元,占39.3%,预计到2034年,复合年增长率将达到6.1%。製药和生物科技产业是主要的终端用户,它们在开发安全、个人化的递送平台方面投入了大量资金。约60%的生物技术公司已在早期研究阶段采用了基于胜肽的系统。除製药业外,由于监管方面的利好,医疗设备製造商和研究机构对胜肽的接受度也在不断提高。化妆品和食品产业也在探索生物活性胜肽,这为新进者的市场扩张创造了机会。

美国肽基奈米材料市场在2024年创收13亿美元,预计复合年增长率为9.1%,到2034年将达到29.3%。凭藉着雄厚的研发投入和完善的生物製药生态系统,美国在肽基奈米材料开发领域处于领先地位。超过35%的奈米医学相关专利来自美国,显示其研发强度高、技术实力强。美国国内製造业发展强劲,并有FDA批准的临床试验和强有力的个人化医疗措施作为后盾,减少了对进口解决方案的依赖。

影响肽基奈米材料市场的关键参与者包括 Genscript Biotech Corporation、PolyPeptide Group、Anika Therapeutics, Inc.、PeptiDream Inc. 和 Bachem Holding AG。为了保持竞争力,肽基奈米材料市场的公司优先投资可扩展的研发,并注重治疗的多功能性和法规遵循。与製药公司、学术机构和临床研究组织的策略合作有助于加速产品开发流程。许多公司也利用先进的胜肽合成技术来提高生产能力,以满足日益增长的全球需求。随着各公司加强其新型奈米材料的专利组合,智慧财产权保护成为关注的重点。此外,市场参与者正在将其应用范围从药物传输扩展到诊断、再生医学和药妆品领域。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计资料(HS 编码)(註:仅提供主要国家的贸易统计数据

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依类型,2021-2034

- 主要趋势

- 自组装胜肽

- 胜肽两亲物

- 胜肽聚合物偶联物

- 胜肽奈米颗粒混合物

- 环肽奈米结构

- 其他的

第六章:市场估计与预测:依奈米结构形态,2021-2034

- 主要趋势

- 奈米纤维和奈米管

- 奈米球和囊泡

- 水凝胶和支架

- 奈米粒子

- 二维奈米片和薄膜

- 其他的

第七章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 药物输送

- 标靶癌症治疗

- 基因和核酸递送

- 其他药物传输应用

- 组织工程与再生医学

- 生物感测与诊断

- 抗菌应用

- 生物影像与治疗诊断学

- 其他应用

第八章:市场估计与预测:按最终用途产业,2021-2034 年

- 主要趋势

- 製药和生物技术

- 医疗保健和医疗器械

- 研究与学术机构

- 化妆品和个人护理

- 食品与农业

- 其他的

第九章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Ferring Pharmaceuticals

- 3D Matrix Medical Technology

- Nanovesicular (NVS) Technologies

- CellMark Medical

- Nanomatrix Therapeutics

- Anika Therapeutics, Inc.

- Nanoviricides, Inc.

- Peptron, Inc.

- Ambiopharm, Inc.

- Bachem Holding AG

- PolyPeptide Group

- Nanosphere Health Sciences, Inc.

- Peptide Solutions, LLC

- PeptiDream Inc.

- Genscript Biotech Corporation

- Peptisyntha (Solvay Group)

- Pepscan

- Nanopartz Inc.

- CPC Scientific Inc.

- Advanced Peptides

The Global Peptide-Based Nanomaterials Market was valued at USD 4.5 billion in 2024 and is estimated to grow at a CAGR of 9.5% to reach USD 11.1 billion by 2034. This market is gaining momentum as the medical industry shifts towards precision medicine and targeted therapy. Peptide-based nanomaterials are gaining attention due to their multifunctional capabilities in drug delivery, imaging, transdermal therapeutics, and tissue engineering. Their ability to act as biocompatible drug carriers and support advanced treatment platforms has made them an attractive alternative to traditional therapies. Increasing private investments and government funding are accelerating the pace of innovation in nanomedicine.

Healthcare systems globally are evolving with a renewed emphasis on advanced medical tools, biologically responsive materials, and nanoscale therapeutics that offer improved efficacy with fewer side effects. The rising demand for smart drug systems, particularly those that can localize and minimize exposure to healthy tissue, is contributing significantly to the adoption of these technologies. In addition, increased interest from investors and public healthcare agencies in biopharmaceutical innovation is giving rise to specialized detection systems, intelligent drug formulation methods, and modular nanostructures aimed at revolutionizing how diseases are treated at the molecular level.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.5 billion |

| Forecast Value | $11.1 billion |

| CAGR | 9.5% |

The self-assembling peptides segment generated USD 1.5 billion in 2024 and is forecast to grow at a CAGR of 8.7% through 2034. The popularity of this segment is driven by the growing demand for controlled-release and site-specific delivery systems. With more than 300 peptide-based carriers in either preclinical or clinical stages, targeted therapeutics-especially for cancer and gene therapy-are key growth areas. Developers are focusing on formulating peptide nanostructures that are biocompatible and biodegradable, allowing for safer drug transport. Innovations are now spilling over into adjacent fields such as diagnostics and molecular imaging, which are seeing interest from both researchers and regulatory stakeholders.

In 2024, the drug delivery application segment held a market value of USD 1.8 billion, representing a 39.3% share and growing at a CAGR of 6.1% through 2034. The pharmaceutical and biotech sectors are the major end-users, heavily investing in developing safe, personalized delivery platforms. Around 60% of biotechnology firms have already incorporated peptide-based systems during early research phases. Beyond pharma, uptake is also growing among healthcare equipment manufacturers and research institutes due to favorable regulatory developments. The cosmetics and food industries are also exploring bioactive peptides, creating opportunities for market expansion among newer entrants.

United States Peptide-Based Nanomaterials Market generated USD 1.3 billion in 2024 and is projected to grow at a CAGR of 9.1%, accounting for 29.3% by 2034. With significant R&D expenditure and a well-established biopharma ecosystem, the US stands as a leader in peptide-based nanomaterials development. More than 35% of nanomedicine-related patents originate from the US, indicating high research intensity and technological capability. Domestic manufacturing is robust, backed by FDA-approved clinical trials and strong initiatives around personalized medicine, reducing reliance on imported solutions.

Key players shaping the Peptide-Based Nanomaterials Market include Genscript Biotech Corporation, PolyPeptide Group, Anika Therapeutics, Inc., PeptiDream Inc., and Bachem Holding AG. To maintain competitiveness, companies in the peptide-based nanomaterials market are prioritizing investments in scalable R&D, focusing on therapeutic versatility and regulatory compliance. Strategic collaborations with pharmaceutical firms, academic institutions, and clinical research organizations help accelerate product development pipelines. Many are also enhancing their production capabilities with advanced peptide synthesis technologies to meet rising global demand. Intellectual property protection is a key focus, as companies strengthen their patent portfolios for novel nanomaterials. Further, market players are expanding their application reach beyond drug delivery into diagnostics, regenerative medicine, and cosmeceuticals.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO Perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Self assembling peptides

- 5.3 Peptide amphiphiles

- 5.4 Peptide polymer conjugates

- 5.5 Peptide nanoparticle hybrids

- 5.6 Cyclic peptide nanostructures

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Nanostructure Morphology, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Nanofibers & nanotubes

- 6.3 Nanospheres & vesicles

- 6.4 Hydrogels & scaffolds

- 6.5 Nanoparticles

- 6.6 2d nanosheets & films

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Drug delivery

- 7.2.1 targeted cancer therapeutics

- 7.2.2 gene & nucleic acid delivery

- 7.2.3 other drug delivery applications

- 7.3 Tissue engineering & regenerative medicine

- 7.4 Biosensing & diagnostics

- 7.5 Antimicrobial applications

- 7.6 Bioimaging & theranostics

- 7.7 Other applications

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Pharmaceutical & biotechnology

- 8.3 Healthcare & medical devices

- 8.4 Research & academic institutions

- 8.5 Cosmetics & personal care

- 8.6 Food & agriculture

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Ferring Pharmaceuticals

- 10.2 3D Matrix Medical Technology

- 10.3 Nanovesicular (NVS) Technologies

- 10.4 CellMark Medical

- 10.5 Nanomatrix Therapeutics

- 10.6 Anika Therapeutics, Inc.

- 10.7 Nanoviricides, Inc.

- 10.8 Peptron, Inc.

- 10.9 Ambiopharm, Inc.

- 10.10 Bachem Holding AG

- 10.11 PolyPeptide Group

- 10.12 Nanosphere Health Sciences, Inc.

- 10.13 Peptide Solutions, LLC

- 10.14 PeptiDream Inc.

- 10.15 Genscript Biotech Corporation

- 10.16 Peptisyntha (Solvay Group)

- 10.17 Pepscan

- 10.18 Nanopartz Inc.

- 10.19 CPC Scientific Inc.

- 10.20 Advanced Peptides

全球陶瓷帷幕墙市场:依安装方式、应用、产品类型及地区划分-市场规模、产业趋势、机会分析及2026-2035年预测

全球陶瓷帷幕墙市场:依安装方式、应用、产品类型及地区划分-市场规模、产业趋势、机会分析及2026-2035年预测 全球生物发光建筑外观市场分析与预测(至2033年):类型、产品、服务、技术、应用、材料类型、流程、最终用户、功能、安装类型

全球生物发光建筑外观市场分析与预测(至2033年):类型、产品、服务、技术、应用、材料类型、流程、最终用户、功能、安装类型