|

市场调查报告书

商品编码

1773328

涵盖作物种子品种市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Cover Crop Seed Varieties Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

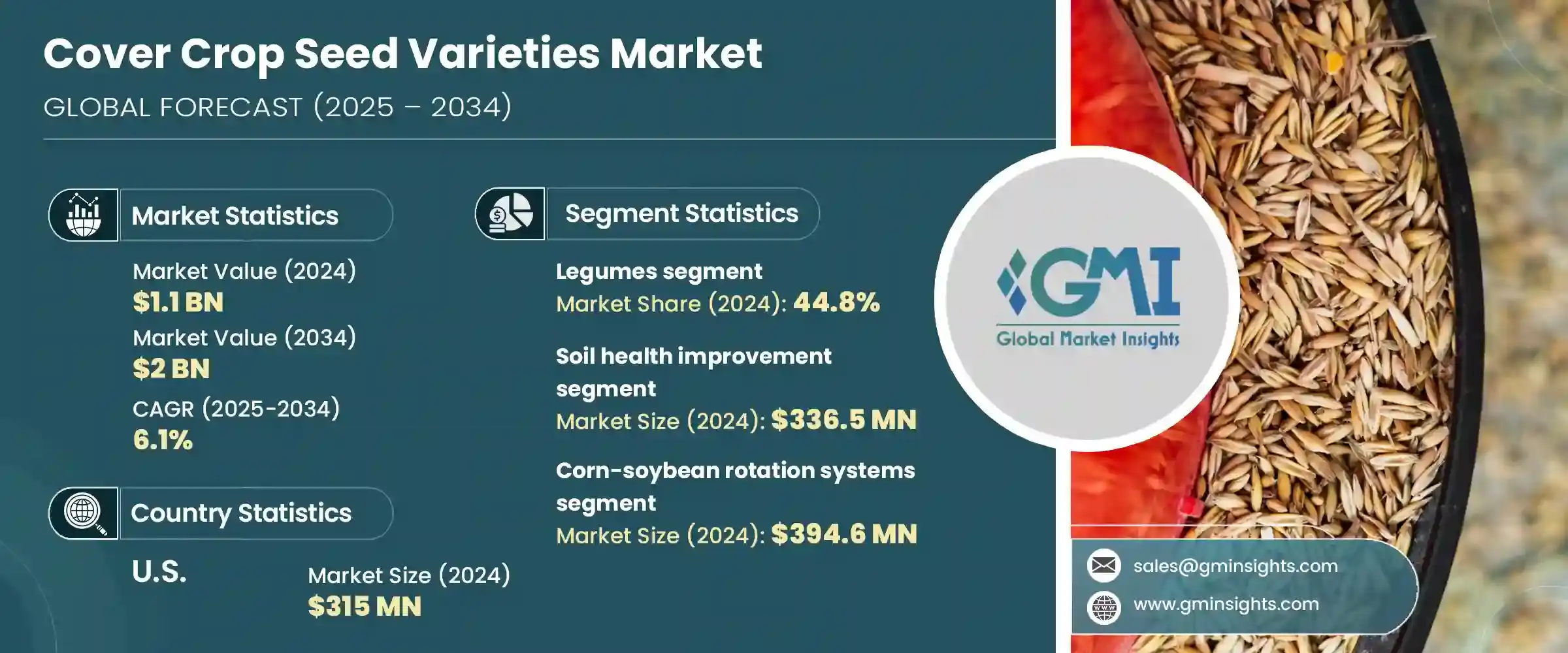

2024年,全球覆盖作物种子品种市场价值11亿美元,预计2034年将以6.1%的复合年增长率成长,达到20亿美元。这一稳步上升趋势主要得益于人们日益转向永续农业以及土壤管理实践日益重要的推动。随着现代农业的不断发展,覆盖作物种子正成为改善土壤整体结构、促进养分循环、以及最大程度减少传统耕作方式对环境造成破坏的重要工具。这些种子在提高土壤肥力、防止土壤侵蚀和自然控制杂草生长方面发挥关键作用——随着农民努力在生产力和环境责任之间取得平衡,这些因素的重要性日益凸显。

农民正在将覆盖作物作为轮作系统和保护性耕作的有效组成部分。这些种子有助于保持土壤水分,提高有机质含量,并促进农田生物多样性。随着气候变迁成为持续挑战,新型种子技术正在透过开发抗旱抗病品种来应对这些问题,尤其是在干旱地区。此外,精准农业的进步使得覆盖作物的策略性部署成为可能,从而提高耕作效率和产量。对永续生产力的追求正鼓励人们采用覆盖作物种子作为可靠的解决方案,在保持产量的同时满足环境目标。因此,无论是小规模农民还是商业农民,都对覆盖作物市场越来越感兴趣,他们希望将环保方法融入自己的经营中。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 11亿美元 |

| 预测值 | 20亿美元 |

| 复合年增长率 | 6.1% |

2024年,豆类作物占据了全球作物市场的主导地位,占据了44.8%的全球收入份额,预计到2034年将以6%的复合年增长率增长。这些种子因其能够透过微生物活动自然固定大气中的氮,从而显着减少对合成肥料的依赖而受到青睐。豆类种子发芽迅速、适应各种气候条件以及改善土壤结构的能力,使其成为希望采用低影响农业系统的农民的实际选择。这些优势共同促进了产量的提高和土壤品质的改善,进一步巩固了该领域在市场上的主导地位。

黑麦、燕麦和大麦等禾本科植物也因其在地面覆盖、土壤稳定和杂草抑制方面的优势而占据了相当大的市场份额。虽然这些品种本身并非主要的氮素贡献者,但它们在生产生物质和保护土壤表面方面发挥关键作用。这些作物通常与豆科植物配合使用,以达到富集养分和控制侵蚀的目的。芸薹属植物,包括具有深根系统的品种,用于土壤鬆土和病虫害防治。然而,它们的市场份额仍然低于豆科植物和禾本科植物,主要是因为它们的效益更具针对性,并且取决于特定的土壤条件和病虫害动态。

从应用角度来看,土壤健康改良领域脱颖而出,成为产业领先领域,2024 年市场规模达 3.365 亿美元,预计到 2034 年复合年增长率将达到 6.2%。人们对再生农业的日益关注,促使农民越来越多地投资于能够增加有机质含量、促进微生物活性并增强土壤结构完整性的覆盖作物种子品种。由于这些作物能够固土并减少径流,它们有助于直接防止养分流失,并提高农田的长期生存力。此外,它们在固氮和固碳方面的天然作用有助于减少对化学投入的需求,同时带来增强生物多样性和改善水渗透等生态效益。

就最终用途而言,玉米-大豆轮作系统在2024年的价值为3.946亿美元,预计到2034年将以6.4%的复合年增长率达到最高。这些系统在大规模农业区广泛实施,因其在保持土壤肥力的同时打破病虫害循环的能力而备受青睐。覆盖作物越来越多地被纳入这些轮作中,以减少氮流失、防止水土流失和抑制杂草生长。覆盖作物与保护措施的兼容性,使其成为注重长期永续性和产量可靠性的生产者的首选。

从区域来看,美国在北美市场处于领先地位,2024 年的估值为 3.15 亿美元,预计到 2034 年将以 6.3% 的复合年增长率成长。美国的优势可以归因于其大规模的农业经营、早期采用永续农业实践,以及透过激励措施和监管框架促进环境管理的政策支持。生产者意识的提高以及消费者对永续来源食品需求的不断增长,也促进了全国覆盖作物种植的快速增长。

全球覆盖作物种子品种市场的领导公司包括拜耳作物科学、科迪华公司、先正达集团、KWS谷物公司和Green Cover Seed公司。这些公司不断扩大产品组合,并利用强大的分销网络来满足全球农民不断变化的需求,进一步塑造这一不断增长的市场的发展轨迹。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 更重视永续农业

- 政府激励措施和环境法规

- 有机和生态友善农业的需求不断增长

- 产业陷阱与挑战

- 种子采购的初始成本高

- 小农户意识有限

- 市场机会

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按作物类型

- 未来市场趋势

- 科技与创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计资料(HS 编码)(註:仅提供重点国家的贸易统计数据

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依作物类型,2021-2034

- 主要趋势

- 豆类

- 深红色的三叶草

- 红三叶草

- 毛苕子

- 奥地利冬豌豆

- 其他豆类品种

- 草类

- 黑麦

- 燕麦

- 冬小麦

- 大麦

- 小黑麦

- 一年生黑麦草

- 其他草种

- 芸薹属植物

- 白萝卜

- 芥菜品种

- 萝卜

- 其他芸薹属品种

- 其他覆盖作物

- 荞麦

- 向日葵

- 法塞莉亚

- 混合物种

第六章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 土壤健康改善

- 侵蚀控制和土壤保护

- 营养管理与固氮

- 杂草抑制和管理

- 碳封存和气候效益

- 牲畜饲料和放牧

- 增强生物多样性和创造栖息地

第七章:市场估计与预测:依最终用途系统,2021-2034

- 主要趋势

- 玉米-大豆轮作制度

- 棉花生产系统

- 蔬菜和特殊作物系统

- 有机农业经营

- 牲畜整合系统

- 保护储备计画申请

- 其他种植制度

第八章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- Bayer Crop Science

- Corteva Inc.

- Syngenta Group

- KWS Cereals

- Green Cover Seed

- Kings AgriSeeds

- GO Seed

- Troy Cover Seed

- GS3 Quality Seed

- Walnut Creek Seeds

- Stokes Seeds

- CoverCress Inc

- Benson Hill

- Cibus

The Global Cover Crop Seed Varieties Market was valued at USD 1.1 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 2 billion by 2034. This steady upward trend is largely fueled by the increasing shift toward sustainable agriculture and the growing importance of soil management practices. As modern farming continues to evolve, cover crop seeds are becoming vital tools in improving overall soil structure, supporting nutrient cycling, and minimizing environmental damage caused by traditional farming methods. These seeds play a pivotal role in enhancing soil fertility, preventing erosion, and naturally managing weed growth-factors that are gaining relevance as farmers strive to balance productivity with environmental responsibility.

Farmers are turning to cover crops as an effective part of crop rotation systems and conservation tillage. These seeds help retain moisture in the soil, improve organic content, and foster biodiversity on farmlands. With climate variability becoming a persistent challenge, newer seed technologies are addressing these concerns by developing drought- and disease-resistant varieties, particularly for regions with arid conditions. Additionally, advancements in precision agriculture are enabling more strategic deployment of cover crops to improve farming efficiency and outcomes. The push toward sustainable productivity is encouraging the adoption of cover crop seeds as a reliable solution to meet environmental targets while maintaining output. As a result, the market is seeing growing interest from both small-scale and commercial farmers who want to integrate eco-friendly methods into their operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $2 Billion |

| CAGR | 6.1% |

In 2024, legumes dominated the market by crop type, securing 44.8% of the global revenue share, and are anticipated to grow at a CAGR of 6% through 2034. These seeds are favored for their ability to naturally fix atmospheric nitrogen through microbial activity, significantly reducing the reliance on synthetic fertilizers. Their fast germination, adaptability across diverse climates, and ability to improve soil structure make them a practical choice for farmers aiming to adopt low-impact agricultural systems. These benefits collectively contribute to improved yields and enhanced soil quality, further strengthening the segment's stronghold in the market.

Grasses, such as rye, oats, and barley, also hold a significant portion of the market due to their performance in ground coverage, soil stabilization, and weed suppression. Although these varieties are not major nitrogen contributors on their own, they play a key role in producing biomass and protecting the soil surface. These crops are commonly used in tandem with legumes to achieve both nutrient enrichment and erosion control. Brassicas, which include species with deep-rooting systems, are used for soil decompaction and pest management. However, their share remains lower than legumes and grasses, mainly because their benefits are more specialized and dependent on specific soil conditions and pest dynamics.

By application, soil health improvement stood out as the leading segment with a market size of USD 336.5 million in 2024 and is poised to grow at a CAGR of 6.2% by 2034. The rising focus on regenerative agriculture has led farmers to increasingly invest in cover crop seed varieties that can boost organic matter, promote microbial activity, and enhance the structural integrity of soil. As these crops hold the soil in place and reduce runoff, they contribute directly to preventing nutrient loss and enhancing the long-term viability of farmland. Moreover, their natural role in nitrogen fixation and carbon sequestration helps reduce the need for chemical inputs while offering ecological benefits such as biodiversity enhancement and improved water infiltration.

In terms of end use, corn-soybean rotation systems accounted for USD 394.6 million in 2024 and are forecasted to grow at the highest rate of 6.4% CAGR through 2034. These systems are widely practiced in large-scale agricultural regions and have gained traction for their ability to maintain soil fertility while breaking pest and disease cycles. Cover crops are increasingly being integrated into these rotations to reduce nitrogen loss, prevent erosion, and suppress weed populations. The compatibility of cover crops with conservation efforts makes this segment a preferred choice for producers focusing on long-term sustainability and yield reliability.

Regionally, the United States led the North American market, with a valuation of USD 315 million in 2024, expected to grow at a CAGR of 6.3% through 2034. The country's dominance can be attributed to its large-scale farming operations, early adoption of sustainable agricultural practices, and policy support through incentives and regulatory frameworks that promote environmental stewardship. Increasing awareness among producers and growing consumer demand for sustainably sourced food has also contributed to the rapid growth of cover crop adoption across the country.

Leading companies in the global cover crop seed varieties market include Bayer Crop Science, Corteva Inc., Syngenta Group, KWS Cereals, and Green Cover Seed. These players continue to expand their product portfolios and leverage strong distribution networks to meet the evolving needs of farmers worldwide, further shaping the trajectory of this growing market.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Crop type

- 2.2.3 Application

- 2.2.4 End use system

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing focus on sustainable agriculture

- 3.2.1.2 Government incentives and environmental regulations

- 3.2.1.3 Rising demand for organic and eco-friendly farming

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial costs for seed procurement

- 3.2.2.2 Limited awareness among smallholder farmers

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By crop type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only )

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Crop Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trend

- 5.2 Legumes

- 5.2.1 Crimson clover

- 5.2.2 Red clover

- 5.2.3 Hairy vetch

- 5.2.4 Austrian winter pea

- 5.2.5 Other legume varieties

- 5.3 Grasses

- 5.3.1 Cereal rye

- 5.3.2 Oats

- 5.3.3 Winter wheat

- 5.3.4 Barley

- 5.3.5 Triticale

- 5.3.6 Annual ryegrass

- 5.3.7 Other grass varieties

- 5.4 Brassicas

- 5.4.1 Daikon radish

- 5.4.2 Mustard varieties

- 5.4.3 Turnips

- 5.4.4 Other brassica varieties

- 5.5 Other cover crops

- 5.5.1 Buckwheat

- 5.5.2 Sunflower

- 5.5.3 Phacelia

- 5.5.4 Mixed species blends

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Thousand Litres)

- 6.1 Key trend

- 6.2 Soil health improvement

- 6.3 Erosion control and soil conservation

- 6.4 Nutrient management and nitrogen fixation

- 6.5 Weed suppression and management

- 6.6 Carbon sequestration and climate benefits

- 6.7 Livestock forage and grazing

- 6.8 Biodiversity enhancement and habitat creation

Chapter 7 Market Estimates & Forecast, By End Use System, 2021-2034 (USD Billion) (Thousand Litres)

- 7.1 Key trends

- 7.2 Corn-soybean rotation systems

- 7.3 Cotton production systems

- 7.4 Vegetable and specialty crop systems

- 7.5 Organic farming operations

- 7.6 Livestock integration systems

- 7.7 Conservation reserve program applications

- 7.8 Other cropping systems

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Litres)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Bayer Crop Science

- 9.2 Corteva Inc.

- 9.3 Syngenta Group

- 9.4 KWS Cereals

- 9.5 Green Cover Seed

- 9.6 Kings AgriSeeds

- 9.7 GO Seed

- 9.8 Troy Cover Seed

- 9.9 GS3 Quality Seed

- 9.10 Walnut Creek Seeds

- 9.11 Stokes Seeds

- 9.12 CoverCress Inc

- 9.13 Benson Hill

- 9.14 Cibus

2034年全球抗旱种子市场预测-按作物类型、性状类型、技术、种子类型、通路、应用、最终用户和地区分類的分析全球包衣作物种子市场预测(至2034年):按种子类型、品种、农业系统、作物整合、应用、最终用户、分销管道和地区分類的分析

2034年全球抗旱种子市场预测-按作物类型、性状类型、技术、种子类型、通路、应用、最终用户和地区分類的分析全球包衣作物种子市场预测(至2034年):按种子类型、品种、农业系统、作物整合、应用、最终用户、分销管道和地区分類的分析 涵盖作物种子混合物市场分析及预测(至2035年):按类型、产品类型、应用、最终用户、技术、实施类型、服务、组件和材料类型

涵盖作物种子混合物市场分析及预测(至2035年):按类型、产品类型、应用、最终用户、技术、实施类型、服务、组件和材料类型 涵盖作物市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年全球耐盐作物市场:预测(至2032年)-按作物类型、性状类型、种子类型、技术、应用和地区进行分析2032 年涵盖作物市场预测:按类型、农场类型、功能、时间段、应用、最终用户和地区进行的全球分析

涵盖作物市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年全球耐盐作物市场:预测(至2032年)-按作物类型、性状类型、种子类型、技术、应用和地区进行分析2032 年涵盖作物市场预测:按类型、农场类型、功能、时间段、应用、最终用户和地区进行的全球分析 抗旱种子品种市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

抗旱种子品种市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球覆盖作物种子混合物市场

全球覆盖作物种子混合物市场 欧洲涵盖作物种子市场规模及预测 2021-2031、区域份额、趋势和成长机会分析报告范围:按品种和国家涵盖作物种子混合物市场、机会、成长动力、产业趋势分析与预测,2024-2032 年

欧洲涵盖作物种子市场规模及预测 2021-2031、区域份额、趋势和成长机会分析报告范围:按品种和国家涵盖作物种子混合物市场、机会、成长动力、产业趋势分析与预测,2024-2032 年