|

市场调查报告书

商品编码

1773331

工业炉市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Industrial Furnaces Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

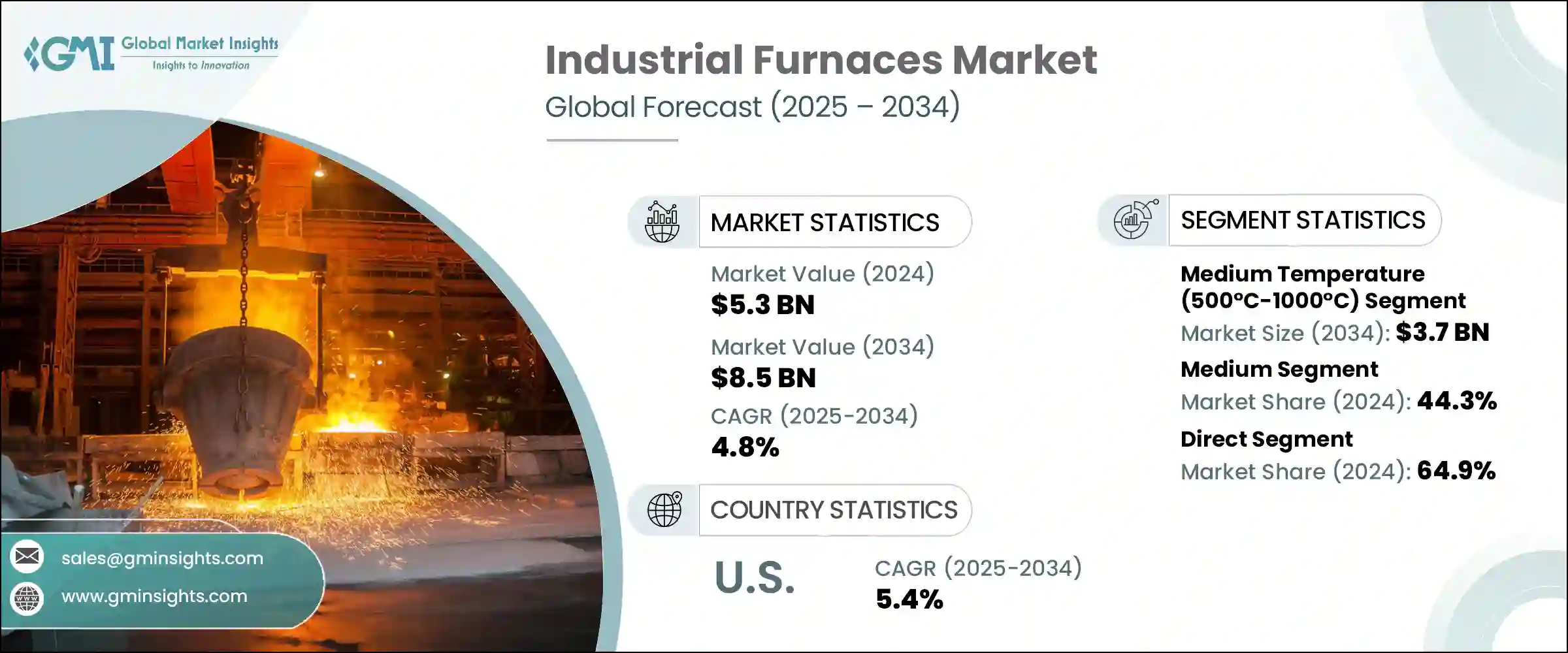

2024 年全球工业炉市场规模为 53 亿美元,预计到 2034 年将以 4.8% 的复合年增长率成长,达到 85 亿美元。金属和钢铁业是这一成长的关键贡献者,因为工业炉对于熔炼、退火和回火等高温製程至关重要,而这些製程是金属成型和处理所必需的。基础设施、汽车生产和工业发展的需求不断增长,尤其是在中国、印度和美国等地区,这推动了对更有效率、更耐用的熔炉的需求。与传统高炉相比,电弧炉 (EAF) 的排放量更低、能源效率更高,其应用日益广泛是另一个重要趋势。电弧炉目前约占全球钢铁产量的 30%,进一步增加了全球对先进熔炉技术的需求。

除了日益重视脱碳之外,各行各业也越来越多地转向替代加热技术,例如氢焰和电弧,以减少碳足迹。这些替代方案被视为转型为更永续的製造流程的关键解决方案。例如,氢焰是一种清洁的燃烧方式,仅排放水蒸气,使其成为减少高温製程排放的理想选择。电弧炉 (EAF) 在钢铁生产中已经非常普及,其与传统炉技术相比,其减少碳排放的能力也正在受到人们的探索。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 53亿美元 |

| 预测值 | 85亿美元 |

| 复合年增长率 | 4.8% |

工业炉市场的中温部分在2024年创收22亿美元,预计2034年将达到37亿美元。中温炉工作温度在500°C至1000°C之间,由于其多功能性和处理各种热处理製程的能力,在全球市场仍占据主导地位。由于其能够加工金属和合金,中温炉广泛应用于汽车、航太和电子製造等产业。

中容量炉市场在2024年占据44.3%的市场份额,预计到2034年将以4.4%的复合年增长率成长。这类炉尤其适用于需要频繁温度循环和中等吞吐量的中型工业应用。机械製造、汽车零件生产和铸造厂等行业依靠中温炉进行持续的品质控制并满足生产要求。

2024年,美国工业炉市场规模达7亿美元,预计2034年将以5.4%的复合年增长率维持强劲成长。凭藉先进的製造能力和节能炉技术的日益普及,美国将继续引领北美工业炉市场。金属加工厂、航太工厂和汽车产业正在推动对新型高效工业炉的需求,因为这些产业致力于减少排放并提高生产力。北美,尤其是美国、加拿大和墨西哥,凭藉其成熟的製造业基础和对永续生产实践的重视,在全球市场占有重要份额。

工业炉市场的主要参与者包括 Harper International、SECO/WARWICK SA、Tenova SpA、Despatch Industries、Carbolite Gero、Lindberg/MPH、Gasbarre Thermal Processing Systems、Nabertherm GmbH、Inductotherm Group、Sur Combustion, Inc.、ABB、Ipsen Corporation、ABductotherm Group、Sur Combustion, Inc.、ABB、Ipsen ABL、VelUm.工业炉市场的公司正在采取多项关键策略来巩固其市场地位。其中一项主要策略是专注于技术创新,例如开发更节能、更永续的炉子。

企业正在大力投资研发,以提高电弧炉 (EAF) 的性能,并探索氢焰等替代方案,以实现脱碳目标。此外,这些企业正致力于透过与汽车、航太和金属加工等关键产业的製造商建立策略合作伙伴关係和协作,扩大其全球影响力。另一项策略是提供客製化解决方案,以满足不同行业的特定需求,增强其市场吸引力并确保长期的客户关係。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 监理框架

- 标准和认证

- 环境法规

- 进出口法规

- 贸易统计(HS 代码 - 8417)

- 主要进口国

- 主要出口国

- 波特五力分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依熔炉类型,2021-2034

- 主要趋势

- 电炉

- 瓦斯炉

- 燃油炉

- 煤炭炉

- 感应炉

- 电弧炉

- 其他的

第六章:市场估计与预测:依温度,2021-2034 年

- 主要趋势

- 低温(500°C以下)

- 中温(500℃-1000℃)

- 高温(1000°C以上)

第七章:市场估计与预测:依产能,2021-2034

- 主要趋势

- 小的

- 中等的

- 大的

第八章:市场估计与预测:依最终用途,2021-2034

- 主要趋势

- 汽车

- 航太

- 有色金属

- 化工和石化

- 石油和天然气

- 食品和饮料

- 其他的

第九章:市场估计与预测:按配销通路,2021-2034

- 主要趋势

- 直接的

- 间接

第十章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 阿联酋

- 沙乌地阿拉伯

第 11 章:公司简介

- ABB

- ANDRITZ AG

- Carbolite Gero

- Despatch Industries

- Gasbarre Thermal Processing Systems

- Harper International

- Inductotherm Group

- Ipsen International GmbH

- Lindberg/MPH

- Nabertherm GmbH

- Nutec Bickley

- SECO/WARWICK SA

- Surface Combustion, Inc.

- Tenova SpA

- Wisconsin Oven Corporation

The Global Industrial Furnaces Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 8.5 billion by 2034. The metal and steel industries are key contributors to this growth, as industrial furnaces are essential for high-temperature processes such as melting, annealing, and tempering, which are required for shaping and treating metals. Rising demand for infrastructure, automotive production, and industrial development, particularly in regions like China, India, and the U.S., is driving the need for more efficient and durable furnaces. The increasing adoption of electric arc furnaces (EAFs), which offer lower emissions and higher energy efficiency compared to traditional blast furnaces, is another important trend. EAFs now account for approximately 30% of global steel production, further increasing the demand for advanced furnace technologies worldwide.

In addition to the rising focus on decarbonization, industries are increasingly turning to alternative heating technologies like hydrogen flames and electric arcs to reduce their carbon footprint. These alternatives are seen as key solutions in the transition to more sustainable manufacturing processes. Hydrogen flames, for example, offer a clean burning option that emits only water vapor, making them an attractive choice for reducing emissions in high-temperature processes. Electric arc furnaces (EAFs), already popular in steel production, are also being explored for their ability to reduce carbon emissions compared to traditional furnace technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $8.5 Billion |

| CAGR | 4.8% |

The medium-temperature segment of the industrial furnaces market generated USD 2.2 billion in 2024 and is expected to reach USD 3.7 billion by 2034. Medium-temperature furnaces, which operate between 500°C and 1000°C, remain a dominant segment in the global market due to their versatility and ability to handle various heat-treatment processes. These furnaces are widely used across industries, from automotive and aerospace to electronics manufacturing, due to their ability to process metals and alloys.

The medium-capacity segment accounted for a 44.3% share in 2024 and is expected to grow at a CAGR of 4.4% through 2034. These furnaces are particularly favored for mid-sized industrial applications that require frequent temperature cycling and moderate throughput. Industries such as machinery manufacturing, auto parts production, and foundries rely on medium-temperature furnaces for consistent quality control and fulfilling production requirements.

United States Industrial Furnaces Market was valued at USD 700 million in 2024, with projections showing strong growth at a CAGR of 5.4% through 2034. The U.S. continues to lead the North American industrial furnaces market due to its advanced manufacturing capabilities and the increasing adoption of energy-efficient furnace technologies. Metal processing plants, aerospace workshops, and the automotive industry are driving demand for new, high-efficiency industrial furnaces, as these sectors work to reduce emissions and improve productivity. North America, particularly the U.S., Canada, and Mexico, holds a significant share of the global market due to the region's mature manufacturing base and focus on sustainable production practices.

Key players in the Industrial Furnaces Market include Harper International, SECO/WARWICK S.A., Tenova S.p.A., Despatch Industries, Carbolite Gero, Lindberg/MPH, Gasbarre Thermal Processing Systems, Nabertherm GmbH, Inductotherm Group, Surface Combustion, Inc., ABB, Ipsen International GmbH, Wisconsin Oven Corporation, Nutec Bickley, and ANDRITZ AG. Companies in the industrial furnaces market are adopting several key strategies to strengthen their position. One of the main approaches is focusing on technological innovation, such as the development of more energy-efficient and sustainable furnaces.

Companies are investing heavily in research and development to improve the performance of electric arc furnaces (EAFs) and explore alternatives like hydrogen flames to meet decarbonization targets. Additionally, these companies are working on expanding their global footprint through strategic partnerships and collaborations with manufacturers in key industries, such as automotive, aerospace, and metal processing. Another strategy is offering customized solutions to meet the specific needs of various industries, enhancing their market appeal and ensuring long-term customer relationships.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Furnace type

- 2.2.3 Temperature

- 2.2.4 Capacity

- 2.2.5 End use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics (HS code- 8417)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Furnace Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Electric furnaces

- 5.3 Gas furnaces

- 5.4 Oil furnaces

- 5.5 Coal furnaces

- 5.6 Induction furnaces

- 5.7 Arc furnaces

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Temperature, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low temperature (Below 500°C)

- 6.3 Medium temperature (500°C - 1000°C)

- 6.4 High temperature (Above 1000°C)

Chapter 7 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Small

- 7.3 Medium

- 7.4 Large

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace

- 8.4 Non-Ferrous metals

- 8.5 Chemical and petrochemical

- 8.6 Oil and gas

- 8.7 Food and beverage

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 UAE

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 ANDRITZ AG

- 11.3 Carbolite Gero

- 11.4 Despatch Industries

- 11.5 Gasbarre Thermal Processing Systems

- 11.6 Harper International

- 11.7 Inductotherm Group

- 11.8 Ipsen International GmbH

- 11.9 Lindberg/MPH

- 11.10 Nabertherm GmbH

- 11.11 Nutec Bickley

- 11.12 SECO/WARWICK S.A.

- 11.13 Surface Combustion, Inc.

- 11.14 Tenova S.p.A.

- 11.15 Wisconsin Oven Corporation

工业炉市场规模、份额和成长分析(按布局、操作方法、应用、结构、最终用户和地区划分)-2026-2033年产业预测

工业炉市场规模、份额和成长分析(按布局、操作方法、应用、结构、最终用户和地区划分)-2026-2033年产业预测 工业炉和烘箱市场(按炉型、加热方式、燃料类型、应用、温度范围、最终用户产业、控制系统和安装类型划分)-2025-2032年全球预测

工业炉和烘箱市场(按炉型、加热方式、燃料类型、应用、温度范围、最终用户产业、控制系统和安装类型划分)-2025-2032年全球预测 工业炉市场报告(按炉型、布置、最终用途和地区)2025-2033

工业炉市场报告(按炉型、布置、最终用途和地区)2025-2033 工业炉市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032)

工业炉市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032) 工业炉市场规模、份额、趋势分析报告:按产品、运转率利用率、最终用途、地区和细分市场预测,2025-2030 年

工业炉市场规模、份额、趋势分析报告:按产品、运转率利用率、最终用途、地区和细分市场预测,2025-2030 年 工业炉市场:成长、未来展望、竞争分析,2025-2033 年

工业炉市场:成长、未来展望、竞争分析,2025-2033 年 电动式工业炉的全球市场:洞察与预测(~2030年)

电动式工业炉的全球市场:洞察与预测(~2030年) 全球工业炉市场

全球工业炉市场