|

市场调查报告书

商品编码

1773358

脱脂奶粉市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Skimmed Milk Powder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

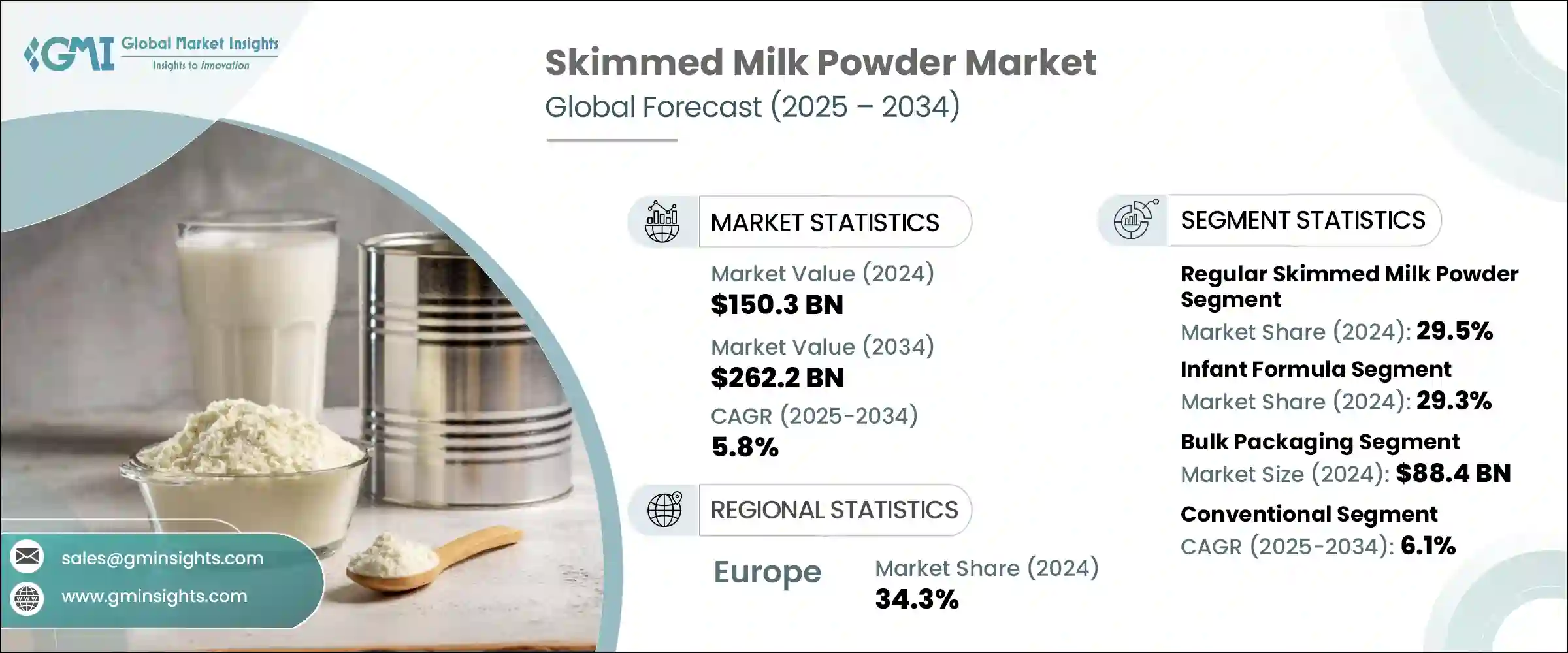

2024年,全球脱脂奶粉市场规模达1,503亿美元,预计到2034年将以5.8%的复合年增长率成长,达到2,622亿美元。人们对健康食品选择的意识不断增强,对优质乳蛋白的需求不断增长,以及婴儿营养、烘焙食品和糖果等行业需求的不断增长,这些因素持续推动着市场扩张。喷雾干燥製程的改进有助于提高产品品质和货架稳定性,为国际贸易创造了巨大的机会。儘管乳製品价格波动、政策变化和贸易动态影响了定价策略和生产计划,但长期市场前景仍然稳健。

竞争格局相对有限,为新製造商进入和扩大规模提供了大量尚未开发的潜力。新兴市场正在稳步养成富含蛋白质的饮食习惯,这进一步支持了长期成长。市场参与者也不断发展,采用更清洁的加工技术和注重环保的生产方式,以满足全球永续发展的期望。即使在供应挑战和价格不确定性的背景下,全球对乳製品功能性成分日益增长的需求确保了脱脂奶粉将继续在乳製品行业的发展中发挥至关重要的作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1503亿美元 |

| 预测值 | 2622亿美元 |

| 复合年增长率 | 5.8% |

2024年,普通脱脂奶粉市场占了29.5%的市场份额,市场规模达444亿美元。其强劲的市场地位源自于其价格实惠和用途广泛,对工业和消费领域都极具吸引力。即溶奶粉旨在快速溶解,是家庭常用的奶粉。高热量和中热量奶粉因其加工耐受性而非常适合工业食品行业;低热量奶粉则吸引了那些寻求加工程度较低、更天然的奶粉的消费者。

散装包装占据市场主导地位,占58.8%,2024年市场规模达884亿美元。这种偏好源于其成本效益、更便捷的物流和更少的材料浪费,这些都与大规模用户的需求相契合。零售包装持续专注于消费者的便利性,提供可重复密封和品牌化包装等功能,以提升货架吸引力。在这两个领域,品牌越来越多地采用环保包装设计,以应对日益增长的环境问题和监管压力。

2024年,欧洲脱脂奶粉市场占有34.3%的份额。该地区的主导地位得益于其成熟的乳製品行业、强大的出口基础设施和先进的加工能力。欧洲生产商受益于严格的品质标准、广泛的研发投入以及支持全球稳定供应的有利贸易协定。该地区在烘焙、婴儿配方奶粉和糖果应用方面也表现出强劲的需求,进一步刺激了国内消费。此外,永续乳牛养殖实践的广泛采用和喷雾干燥技术的进步有助于提高生产效率和产品一致性。

主要的产业领导者包括菲仕兰康柏尼、达能集团、爱氏晨曦、雀巢和恆天然合作集团。脱脂奶粉产业的领先公司正致力于扩大全球分销网络,利用特定地区的饮食趋势,并建立策略联盟以提高供应链效率。对最先进的喷雾干燥设备和自动化加工生产线的投资可以提高产品的一致性和产量。许多公司瞄准高成长地区,推出针对特定族群的强化或加值乳製品。永续性是一个中心主题,各大品牌纷纷采用更环保的能源和可回收包装。透过符合全球营养标准并维持严格的品质控制,这些公司正在确保多元化消费者群体的长期信任和品牌忠诚度。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 普通脱脂奶粉

- 即溶脱脂奶粉

- 高温脱脂奶粉

- 中火脱脂奶粉

- 低热脱脂奶粉

- 有机脱脂奶粉

- 强化脱脂奶粉

- 维生素强化

- 矿物质强化

- 富含蛋白质

第六章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 婴儿配方奶粉

- 烘焙和糖果

- 麵包和烘焙食品

- 蛋糕和糕点

- 糖果产品

- 其他烘焙应用

- 乳製品

- 復原乳

- 优格和发酵产品

- 乳酪生产

- 冰淇淋和冷冻甜点

- 加工食品

- 即食食品

- 汤和酱汁

- 肉製品

- 其他加工食品

- 饮料

- 蛋白质饮料

- 营养饮料

- 咖啡和茶增白剂

- 其他饮料应用

- 营养补充品

- 蛋白质补充剂

- 运动营养

- 临床营养

- 动物饲料

- 其他的

- 化妆品和个人护理

- 製药应用

- 工业应用

第七章:市场估计与预测:依包装类型,2021 - 2034 年

- 主要趋势

- 散装包装

- 25公斤袋

- 50公斤袋

- 大袋(500-1000公斤)

- 其他散装包装

- 零售包装

- 小袋装(100g-500g)

- 中包装(1kg-5kg)

- 罐头和罐子

- 其他零售包装

第八章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- B2B(企业对企业)

- 食品製造商

- 婴儿配方奶粉製造商

- 麵包店和糖果店

- 餐饮业

- 其他B2B频道

- B2C(企业对消费者)

- 超市和大卖场

- 便利商店

- 网路零售

- 专卖店

- 其他B2C频道

第九章:市场估计与预测:依性质,2021 - 2034 年

- 主要趋势

- 传统的

- 有机的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第 11 章:公司简介

- Fonterra Co-operative Group Limited

- Nestle SA

- Danone SA

- Arla Foods amba

- FrieslandCampina

- Lactalis Group

- Dairy Farmers of America (DFA)

- Saputo Inc.

- Glanbia plc

- Sodiaal Union

- Hochdorf Swiss Nutrition Ltd.

- Euroserum

- Dairygold Co-operative Society Limited

- Interfood Holding BV

- Synlait Milk Limited

- Westland Milk Products

- Murray Goulburn Co-operative

- Amul (Gujarat Cooperative Milk Marketing Federation)

- Yili Group

- Mengniu Dairy Company

The Global Skimmed Milk Powder Market was valued at USD 150.3 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 262.2 billion by 2034. The rising awareness around healthier food choices, the push for high-quality dairy proteins, and increasing demand in sectors like infant nutrition, baked goods, and confectionery continue to drive market expansion. Improvements in spray-drying processes have helped enhance product quality and shelf stability, creating strong opportunities for international trade. Although dairy price fluctuations, policy shifts, and trade dynamics have impacted pricing strategies and production planning, the long-term market outlook remains solid.

The competitive landscape is relatively limited, offering plenty of untapped potential for new manufacturers to enter and scale. Emerging markets are steadily adopting protein-rich dietary habits, which further support long-term growth. Market players are also evolving with cleaner processing technologies and environmentally conscious manufacturing to meet global sustainability expectations. Even amid supply challenges and pricing uncertainties, the rising global appetite for dairy-based functional ingredients ensures that skimmed milk powder will continue to play a vital role in the evolution of the dairy sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $150.3 Billion |

| Forecast Value | $262.2 Billion |

| CAGR | 5.8% |

The regular skimmed milk powder segment held a significant 29.5% share in 2024, with a market size of USD 44.4 billion. Its strong position stems from affordability and versatility, which appeal to both industrial and consumer applications. Instant variants are designed for fast solubility and are favored in household use. High-heat and medium-heat varieties serve the industrial food sector well, thanks to their processing tolerance, low-heat versions attract consumers looking for less processed options with more natural qualities.

Bulk packaging segment dominated the market with a 58.8% share and USD 88.4 billion in 2024. This preference is driven by its cost-efficiency, better-handling logistics, and reduced material waste, which align well with the needs of large-scale users. Retail packages continue to focus on consumer convenience, offering features like resealability and branded formats to boost shelf appeal. Across both segments, brands are increasingly adopting eco-conscious packaging designs that align with rising environmental concerns and regulatory pressures.

Europe Skimmed Milk Powder Market held a 34.3% share in 2024. The region's dominance is driven by its well-established dairy industry, strong export infrastructure, and advanced processing capabilities. European producers benefit from robust quality standards, extensive R&D investments, and favorable trade agreements that support consistent global supply. The region also exhibits strong demand across bakery, infant formula, and confectionery applications, further fueling domestic consumption. Moreover, the widespread adoption of sustainable dairy farming practices and technological advancements in spray drying contribute to production efficiency and product consistency.

Key industry leaders include FrieslandCampina, Danone S.A., Arla Foods amba, Nestle S.A., and Fonterra Co-operative Group Limited. Leading companies in the skimmed milk powder industry are focusing on expanding global distribution networks, leveraging region-specific dietary trends, and forming strategic alliances to enhance supply chain efficiency. Investments in state-of-the-art spray drying facilities and automated processing lines allow for better consistency and increased output. Many firms are targeting high-growth regions by launching fortified or value-added dairy variants tailored for specific demographics. Sustainability is a central theme, with brands adopting greener energy sources and recyclable packaging. By aligning with global nutrition standards and maintaining strict quality control, these companies are ensuring long-term trust and brand loyalty across diversified consumer bases.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Thousand Liters)

- 5.1 Key trends

- 5.2 Regular skimmed milk powder

- 5.3 Instant skimmed milk powder

- 5.4 High heat skimmed milk powder

- 5.5 Medium heat skimmed milk powder

- 5.6 Low heat skimmed milk powder

- 5.7 Organic skimmed milk powder

- 5.8 Fortified skimmed milk powder

- 5.8.1 Vitamin fortified

- 5.8.2 Mineral fortified

- 5.8.3 Protein enriched

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Liters)

- 6.1 Key trends

- 6.2 Infant formula

- 6.3 Bakery & confectionery

- 6.3.1 Bread & baked goods

- 6.3.2 Cakes & Pastries

- 6.3.3 Confectionery products

- 6.3.4 Other bakery applications

- 6.4 Dairy products

- 6.4.1 Reconstituted milk

- 6.4.2 Yogurt & fermented products

- 6.4.3 Cheese production

- 6.4.4 Ice cream & frozen desserts

- 6.5 Processed foods

- 6.5.1 Ready-to-Eat meals

- 6.5.2 Soups & sauces

- 6.5.3 Meat products

- 6.5.4 Other processed foods

- 6.6 Beverages

- 6.6.1 Protein drinks

- 6.6.2 Nutritional beverages

- 6.6.3 Coffee & tea whiteners

- 6.6.4 Other beverage applications

- 6.7 Nutritional supplements

- 6.7.1 Protein supplements

- 6.7.2 Sports nutrition

- 6.7.3 Clinical nutrition

- 6.8 Animal feed

- 6.9 Others

- 6.9.1 Cosmetics & personal care

- 6.9.2 Pharmaceutical applications

- 6.9.3 Industrial applications

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Billion) (Thousand Liters)

- 7.1 Key trends

- 7.2 Bulk packaging

- 7.2.1 25 kg bags

- 7.2.2 50 kg bags

- 7.2.3 Big bags (500-1000 kg)

- 7.2.4 Other bulk packaging

- 7.3 Retail packaging

- 7.3.1 Small pouches (100g-500g)

- 7.3.2 Medium packs (1kg-5kg)

- 7.3.3 Cans & tins

- 7.3.4 Other retail packaging

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Liters)

- 8.1 Key trends

- 8.2 B2B (Business-to-Business)

- 8.2.1 Food manufacturers

- 8.2.2 Infant formula manufacturers

- 8.2.3 Bakeries & confectioneries

- 8.2.4 Foodservice industry

- 8.2.5 Other B2B channels

- 8.3 B2C (Business-to-Consumer)

- 8.3.1 Supermarkets & hypermarkets

- 8.3.2 Convenience stores

- 8.3.3 Online retail

- 8.3.4 Specialty stores

- 8.3.5 Other B2C channels

Chapter 9 Market Estimates and Forecast, By Nature, 2021 - 2034 (USD Billion) (Thousand Liters)

- 9.1 Key trends

- 9.2 Conventional

- 9.3 Organic

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Liters)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Fonterra Co-operative Group Limited

- 11.2 Nestle S.A.

- 11.3 Danone S.A.

- 11.4 Arla Foods amba

- 11.5 FrieslandCampina

- 11.6 Lactalis Group

- 11.7 Dairy Farmers of America (DFA)

- 11.8 Saputo Inc.

- 11.9 Glanbia plc

- 11.10 Sodiaal Union

- 11.11 Hochdorf Swiss Nutrition Ltd.

- 11.12 Euroserum

- 11.13 Dairygold Co-operative Society Limited

- 11.14 Interfood Holding B.V.

- 11.15 Synlait Milk Limited

- 11.16 Westland Milk Products

- 11.17 Murray Goulburn Co-operative

- 11.18 Amul (Gujarat Cooperative Milk Marketing Federation)

- 11.19 Yili Group

- 11.20 Mengniu Dairy Company