|

市场调查报告书

商品编码

1773380

空心砖市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Hollow Bricks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

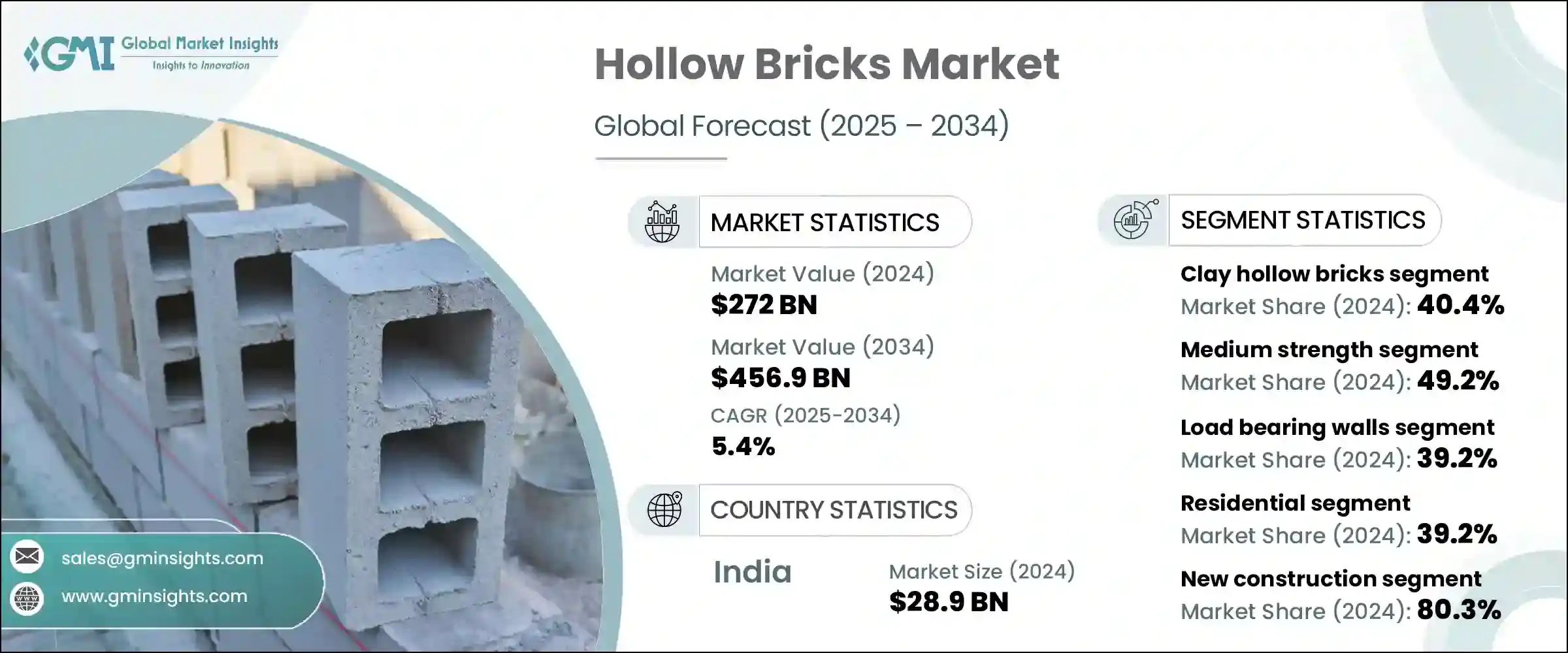

2024年,全球空心砖市场规模达2,720亿美元,预计到2034年将以5.4%的复合年增长率成长,达到4,569亿美元。随着新建住宅和商业建筑需求的不断增长,尤其是在大都市和郊区,空心砖的需求量也显着增加。空心砖易于安装且经济高效,是大型建筑专案的理想选择。政府支持的经济适用房计画也鼓励使用经济实惠且永续的建筑材料,促进了这一成长趋势。空心砖具有天然的隔热和隔热性能,节能高效。它还能帮助降低冷气和供暖成本,这与人们对绿色建筑和节能建筑日益增长的关注相契合,因此成为具有环保意识的开发商的首选材料。

这些砖块有助于调节室内温度和噪音水平,使建筑物在气候变迁多端、噪音水平较高的城市环境中更加舒适。其结构减少了对砂浆的需求,并最大限度地减少了对高强度材料的需求,从而降低了整体建筑成本。轻质特性使运输和组装更快、更有效率,尤其是在劳动力和预算紧张的情况下。此外,模组化和预製建筑技术的日益普及,进一步增加了对空心砖的需求,因为它们与现代建筑实践相容,并有助于加快专案进度。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 2720亿美元 |

| 预测值 | 4569亿美元 |

| 复合年增长率 | 5.4% |

2024年,黏土空心砖市场占有40.4%的份额。随着建筑业转向高强度轻质材料,各种类型黏土砖的需求持续成长。粘土基砖仍然是主流选择,尤其是在低层建筑中,因为它们供应广泛且製造工艺经济高效。粘土砖的热工性能和强度特性使其在农村和发展中城市地区广泛应用,尤其是在新兴经济体,因为这些地区对材料的可负担性和可获得性至关重要。

2024年,承重墙领域使用的空心砖贡献了39.2%的市占率。这些墙体是现代建筑设计的基本组成部分,为住宅和商业项目提供耐用性和必要的结构支撑。虽然承重应用占主导地位,但由于其易用性和轻质特性,空心砖在非承重内墙中的使用也显着增长。空心砖日益普及,这与不断变化的设计需求息息相关,这些需求倾向于在新建筑中实现更快的安装速度和多样化的布局选择。

印度空心砖市场占82%的市场份额,2024年市场规模达289亿美元。快速的城市发展、广泛的建筑活动以及公共基础设施和住房计划的强劲势头,推动了印度空心砖市场的领先地位。印度强大的製造业生态系统和充足的高强度原料供应,进一步巩固了其市场主导地位。此外,小城市和二线市场的日益普及也扩大了国内消费基础。同时,旨在推广永续和节能建筑材料的政策措施,也进一步加速了各地区的空心砖使用。

一些最具影响力的空心砖行业参与者包括 Xella Group、H+H International A/S、UltraTech Cement Ltd、Biltech Building Elements Limited 和 Wienerberger AG。这些公司正透过产品创新和在关键地区的策略布局,积极推动市场发展。为了巩固其在空心砖市场的地位,领先的製造商正在运用多种成长策略。这些策略包括建立区域製造中心以降低物流成本并提高配送效率,投资自动化生产以在保持一致性的同时扩大产量,以及推出具有更高强度和热性能的先进产品。与房地产开发商和建筑公司的合作也被证明能够有效推动空心砖的普及。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 不断发展的建筑业

- 更加重视能源效率

- 成本效益和减少材料使用

- 卓越的隔热和隔音性能

- 产业陷阱与挑战

- 来自替代建筑材料的竞争

- 波动的强度等级价格

- 区域建筑规范合规性

- 品质控制和一致性问题

- 市场机会

- 环保空心砖的开发

- 新兴市场的扩张

- 製造业的技术进步

- 与现代建筑技术的融合

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 黏土空心砖

- 混凝土空心砌块

- 粉煤灰空心砖

- AAC(加气混凝土)空心砌块

- 其他的

第六章:市场估计与预测:依强度等级,2021 年至 2034 年

- 主要趋势

- 低强度

- 中等强度

- 高强度

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 承重墙

- 外部承重墙

- 内部承重墙

- 其他的

- 非承重墙

- 隔间墙

- 填充墙

- 其他的

- 基金会

- 柱子和支柱

- 过樑和横樑

- 其他的

第八章:市场估计与预测:按最终用途产业,2021 - 2034 年

- 主要趋势

- 住宅

- 独栋住宅

- 多户建筑

- 经济适用房

- 其他的

- 商业的

- 办公大楼

- 零售空间

- 饭店业

- 医疗保健设施

- 教育机构

- 其他的

- 工业的

- 生产设施

- 仓库

- 其他的

- 基础设施

- 其他的

第九章:市场估计与预测:按建筑类型,2021 - 2034 年

- 主要趋势

- 新建筑

- 翻新和改造

第 10 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 直销

- 分销商和批发商

- 家居装饰店

- 网路零售

- 其他的

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十二章:公司简介

- AERCON AAC

- Biltech Building Elements Limited

- Eco Green Products Pvt. Ltd

- Fusion Blocks

- H+H International A/S

- Infra.Market

- Jindal Mechno Bricks Private Limited

- Magicrete Building Solutions Pvt. Ltd

- MRF Bricks

- NICBM

- Paver India

- SOLBET

- UltraTech Cement Ltd

- Wienerberger AG

- Xella Group

The Global Hollow Bricks Market was valued at USD 272 billion in 2024 and is estimated to grow at a CAGR of 5.4 % to reach USD 456.9 billion by 2034. The rising demand for new residential and commercial structures, particularly in metropolitan and suburban areas, is significantly boosting the need for hollow bricks. Their ease of installation and cost-effectiveness make them an ideal choice for large-scale construction projects. Government-backed affordable housing initiatives have also contributed to this upward trend by encouraging the use of economical and sustainable building materials. Hollow bricks provide natural insulation against heat and cold, making them energy efficient. Their ability to help reduce cooling and heating costs aligns with the growing focus on green buildings and energy-efficient construction, making them preferred material among environmentally conscious developers.

These bricks help regulate indoor temperatures and noise levels, making buildings more comfortable in urban environments with fluctuating climates and higher sound levels. Their structure reduces the need for excess mortar and minimizes the demand for high-strength materials, which cuts down overall construction costs. Lightweight properties make transportation and assembly faster and more resource-efficient, especially where labor and budgets are tight. Moreover, the growing adoption of modular and prefabricated construction techniques is further increasing the demand for hollow bricks due to their compatibility with modern construction practices and their contribution to accelerated project timelines.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $272 Billion |

| Forecast Value | $456.9 Billion |

| CAGR | 5.4% |

In 2024, the clay hollow bricks segment held a 40.4% share. The demand for these bricks continues to rise across various material types as the construction industry shifts toward high-strength yet lightweight options. Clay-based variants remain a dominant choice, particularly in low-rise developments, due to their wide availability and cost-efficient manufacturing processes. Their thermal performance and strength properties support their widespread use in both rural and developing urban regions, especially in emerging economies where affordability and access to materials are critical.

Hollow bricks used in the load-bearing walls segment contributed a 39.2% share in 2024. These walls are a fundamental part of modern building design, providing durability and essential structural support for residential and commercial projects alike. While load-bearing applications dominate, there is also notable growth in the use of hollow bricks in non-load-bearing interior walls due to their ease of use and lightweight nature. Their growing popularity is tied to evolving design needs that favor faster installation and versatile layout options in new buildings.

India Hollow Bricks Market held an 82% share and generated USD 28.9 billion in 2024. The country's leadership is driven by rapid urban growth, widespread construction activities, and the momentum created by public infrastructure and housing schemes. India's robust manufacturing ecosystem and ample availability of strength-class raw materials further strengthen its market dominance. Additionally, rising adoption in smaller cities and tier-two markets has broadened the domestic consumption base. Meanwhile, policy efforts aimed at promoting sustainable and energy-efficient building materials have further accelerated the use of hollow bricks across various regions.

Some of the most influential players shaping the Hollow Bricks Industry include Xella Group, H+H International A/S, UltraTech Cement Ltd, Biltech Building Elements Limited, and Wienerberger AG. These companies are actively contributing to the market's evolution through product innovation and strategic presence across key regions. To solidify their positions in the hollow bricks market, leading manufacturers are leveraging multiple growth strategies. These include setting up regional manufacturing hubs to reduce logistics costs and improve distribution efficiency, investing in automated production to scale output while maintaining consistency, and introducing advanced product variants with enhanced strength and thermal performance. Partnerships with real estate developers and construction firms have also proven effective in driving adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Strength Class

- 2.2.4 Application

- 2.2.5 End use industry

- 2.2.6 Production process

- 2.2.7 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing construction industry

- 3.2.1.2 Increasing focus on energy efficiency

- 3.2.1.3 Cost-effectiveness and reduced material usage

- 3.2.1.4 Superior thermal and acoustic insulation properties

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Competition from alternative building materials

- 3.2.2.2 Fluctuating Strength Class prices

- 3.2.2.3 Regional building code compliance

- 3.2.2.4 Quality control and consistency issues

- 3.2.3 Market opportunities

- 3.2.3.1 Development of eco-friendly hollow bricks

- 3.2.3.2 Expansion in emerging markets

- 3.2.3.3 Technological advancements in manufacturing

- 3.2.3.4 Integration with modern construction techniques

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Clay hollow bricks

- 5.3 Concrete hollow blocks

- 5.4 Fly ash hollow bricks

- 5.5 AAC (Autoclaved Aerated Concrete) hollow blocks

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Strength Class, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Low strength

- 6.3 Medium strength

- 6.4 High strength

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Load bearing walls

- 7.2.1 External load bearing walls

- 7.2.2 Internal load bearing walls

- 7.2.3 Others

- 7.3 Non-load bearing walls

- 7.3.1 Partition walls

- 7.3.2 Infill walls

- 7.3.3 Others

- 7.4 Foundations

- 7.5 Columns and pillars

- 7.6 Lintels and beams

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential

- 8.2.1 Single-family homes

- 8.2.2 Multi-family buildings

- 8.2.3 Affordable housing

- 8.2.4 Others

- 8.3 Commercial

- 8.3.1 Office buildings

- 8.3.2 Retail spaces

- 8.3.3 Hospitality

- 8.3.4 Healthcare facilities

- 8.3.5 Educational institutions

- 8.3.6 Others

- 8.4 Industrial

- 8.4.1 Manufacturing facilities

- 8.4.2 Warehouses

- 8.4.3 Others

- 8.5 Infrastructure

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Construction Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 New construction

- 9.3 Renovation and retrofitting

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Distributors and wholesalers

- 10.4 Home improvement stores

- 10.5 Online retail

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 AERCON AAC

- 12.2 Biltech Building Elements Limited

- 12.3 Eco Green Products Pvt. Ltd

- 12.4 Fusion Blocks

- 12.5 H+H International A/S

- 12.6 Infra.Market

- 12.7 Jindal Mechno Bricks Private Limited

- 12.8 Magicrete Building Solutions Pvt. Ltd

- 12.9 MRF Bricks

- 12.10 NICBM

- 12.11 Paver India

- 12.12 SOLBET

- 12.13 UltraTech Cement Ltd

- 12.14 Wienerberger AG

- 12.15 Xella Group

镁铬砖市场:2026-2032年全球市场预测(按产品类型、类别、形式、形状、最终用户产业、应用和销售管道)

镁铬砖市场:2026-2032年全球市场预测(按产品类型、类别、形式、形状、最终用户产业、应用和销售管道) 2026年全球污染吸收砖市场报告砖块市场:2026-2032年全球市场预测(依产品类型、製造流程、应用及通路划分)绝缘耐火砖市场:2026-2032年全球市场预测(按材质、产品类型、工作温度、应用和分销管道划分)

2026年全球污染吸收砖市场报告砖块市场:2026-2032年全球市场预测(依产品类型、製造流程、应用及通路划分)绝缘耐火砖市场:2026-2032年全球市场预测(按材质、产品类型、工作温度、应用和分销管道划分) 镁铬砖市场分析及预测(至2035年):类型、产品、应用、材质类型、技术、最终用户、安装类型、製程、组件、功能

镁铬砖市场分析及预测(至2035年):类型、产品、应用、材质类型、技术、最终用户、安装类型、製程、组件、功能 砖块:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

砖块:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球飞灰砖机市场规模、份额、趋势和成长分析报告:2026-2034年

全球飞灰砖机市场规模、份额、趋势和成长分析报告:2026-2034年 污染吸收砖市场规模、份额和成长分析(按产品类型、应用、原材料、技术、最终用户和地区划分)- 产业预测(2026-2033 年)

污染吸收砖市场规模、份额和成长分析(按产品类型、应用、原材料、技术、最终用户和地区划分)- 产业预测(2026-2033 年) 黏土砖市场-全球产业规模、份额、趋势、机会及预测(细分、按混凝土砌块类型、按製造工艺类型、按地区、按竞争情况,2020-2030 年预测)

黏土砖市场-全球产业规模、份额、趋势、机会及预测(细分、按混凝土砌块类型、按製造工艺类型、按地区、按竞争情况,2020-2030 年预测) 全球粘土砖市场

全球粘土砖市场