|

市场调查报告书

商品编码

1773392

有机种子品种市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Organic Seed Varieties Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

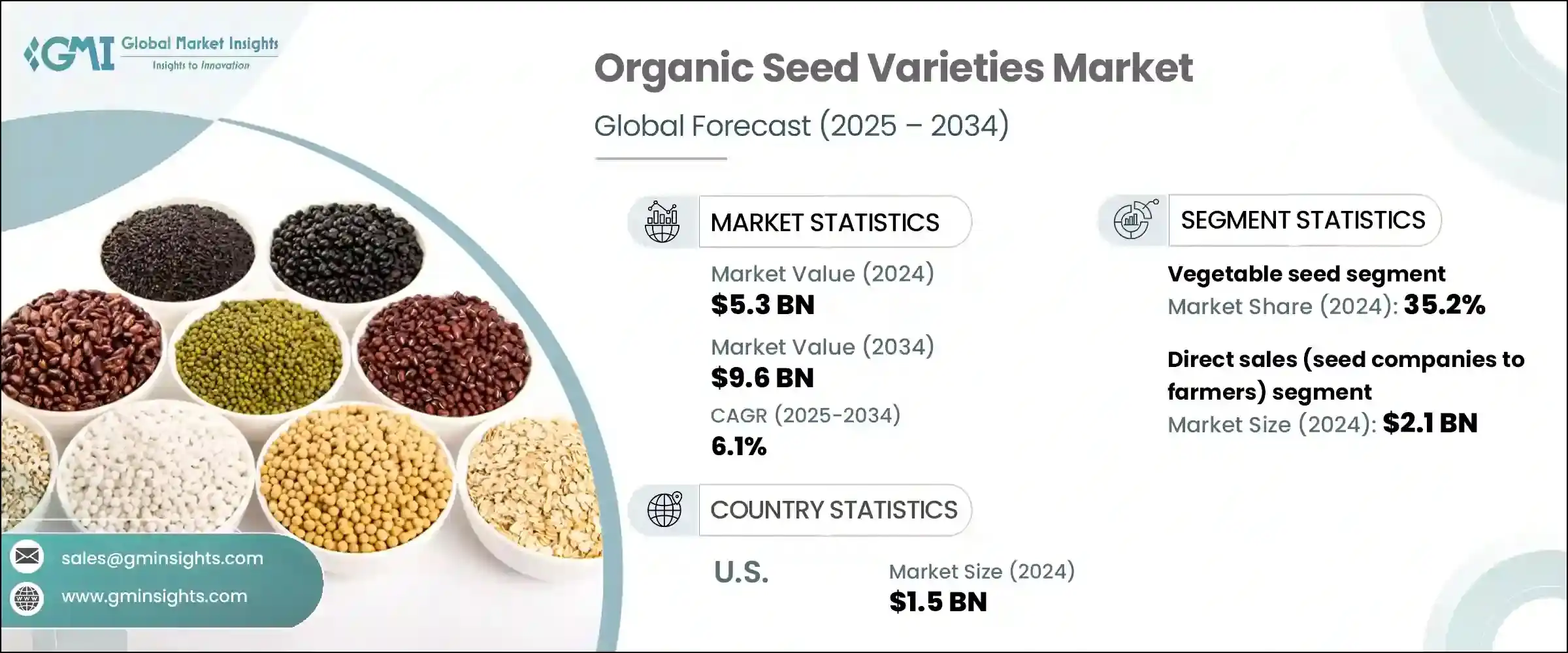

2024 年全球有机种子品种市场价值为 53 亿美元,预计到 2034 年将以 6.1% 的复合年增长率增长至 96 亿美元。这一增长是由消费者对健康、永续性和粮食安全的意识不断提高所推动的。随着越来越多的人转向更健康的生活方式和环保选择,对有机种子的需求持续上升。有机农业作为保护生物多样性、减少化学品使用和促进弹性农业实践的关键策略,发展势头强劲。有机种子,通常是传家宝品种或非常适合特定气候的种子,透过提高农民在恶劣环境下种植作物的能力,为粮食安全做出贡献。它们也有助于维护种子主权,对维护农业遗传多样性至关重要。气候变迁凸显了能够承受不可预测天气的抗逆作物的重要性,这进一步提振了市场。

此外,随着人们对永续性和粮食安全的担忧日益加剧,世界各国政府正在加强对有机农业的支持力度。这包括增加资金、拨款和政策倡议,旨在促进有机种子生产,并推动生态友善农业实践的转型。政府的这种支持在促进有机种子产业发展方面发挥关键作用,鼓励大规模生产者和小农户转向有机农业方法。这些努力不仅有助于确保农业的长期永续性,也有助于实现生物多样性保护和减少农业化学品使用的更广泛目标。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 53亿美元 |

| 预测值 | 96亿美元 |

| 复合年增长率 | 6.1% |

2024年,蔬菜种子(从种子公司到农民)细分市场占据35.2%的市场。预计未来十年,该细分市场将以6.4%的稳健复合年增长率成长,反映出消费者对有机、本地种植农产品的偏好日益增长。随着越来越多的人注重健康,寻求无化学成分的蔬菜,家庭园艺者和商业种植者都越来越多地转向有机蔬菜种子品种。这一趋势推动了对蔬菜种子的需求,因为蔬菜种子被认为是促进营养和健康饮食习惯的关键。

2024年,直销市场规模达21亿美元,预计2034年将以6.3%的复合年增长率成长。此模式因其个人化服务而备受青睐,使种子生产商能够提供客製化解决方案,满足个别农户的独特需求。直销省去了中间商环节,有助于确保客户及时收到产品,从而建立更牢固的客户关係并提高客户满意度。此外,直销还能提供专家建议、物流支援和客製化的配送方案,这也使其成为大型农业经营者和小型独立农户的首选管道。

2024年,美国有机种子品种市场规模达15亿美元。市场对有机农产品的需求,加上政府的优惠政策和强大的有机供应链,共同支持了这一成长。随着有机农业标准日益严格,许多农民开始采用有机种子生产方式以符合法规要求,而种子公司也不断创新,拓展产品线。随着农业经营规模化和有机农场数量的不断增长,美国市场预计将持续扩张。

全球有机种子品种市场的顶级参与者包括 Farm Direct Organic Seeds、Baker Creek Heirloom Seeds、Fedco Seeds、High Mowing Organic Seeds 和 Johnny's Selected Seeds。为了巩固其地位,有机种子品种市场的公司专注于提供高品质、适应当地情况的种子品种,以满足特定的环境条件和消费者偏好。种子保存方面的创新和开发新的、抗逆性的品种是其策略的核心。此外,公司正在增加对研发的投资,以提高种子的产量和抗病性。许多公司也透过直销与农民建立更牢固的关係,并提供个人化服务,以确保满足农民的需求。环境永续性和支持当地经济已成为公司的关键卖点,因为它们既吸引了环保意识的消费者,也吸引了寻求永续解决方案的农民。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 北美:有机消费者日益成为主流

- 欧洲:永续食品生产实践将刺激有机种子的需求

- 亚太地区:向有机农业实践转型

- 产业陷阱与挑战

- 有机品种供应有限

- 价格溢价和认证负担

- 市场机会

- 作物多样化和利基市场增长

- 区域育种与气候适应

- 数位化和直接面向消费者的管道

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按作物类型

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 价值链分析

- 种子育种与生产

- 认证和测试

- 分销和零售

- 最终用途细分市场(商业种植者、小农户、家庭园丁)

- 永续性和生物多样性

- 有机种子在农业生态学和粮食安全中的作用

- 生物多样性保育倡议

- 种子主权与地方种子系统

- 认证和监管

- 美国农业部 NOP 认证的有机种子

- 欧盟有机认证种子

- 其他国家和地区认证

- 非基因改造认证种子

- 种子处理和包衣(符合有机标准)

- 合规成本和市场影响

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依作物类型,2021-2034

- 主要趋势

- 蔬菜种子

- 莴苣

- 番茄

- 菠菜

- 红萝卜

- 黄瓜

- 甜椒

- 谷物种子

- 小麦

- 玉米

- 米

- 大麦

- 燕麦

- 粟

- 藜麦

- 水果种子

- 瓜

- 西瓜

- 草莓

- 浆果品种

- 草本植物和花卉种子

- 罗勒

- 香菜

- 香菜

- 向日葵

- 百日草

- 万寿菊

- 油籽和替代谷物

- 大豆

- 亚麻

- 荞麦

- 苋菜

- 芝麻

第六章:市场估计与预测:按配销通路,2021-2034 年

- 主要趋势

- 直接销售(种子公司对农民)

- 零售通路(园艺中心、农场用品店)

- 网路销售与电子商务平台

- 合作社和采购俱乐部

- 批发和机构买家

第七章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第八章:公司简介

- Adaptive Seeds

- Baker Creek Heirloom Seeds

- Eden Seeds

- Farm Direct Organic Seeds

- Fedco Seeds

- High Mowing Organic Seeds

- Johnny's Selected Seeds

- Kusa Seed Society

- Quality Organic

- Resilient Seeds

- Seed Savers Exchange

- Southern Exposure Seed Exchange

- Victory Seeds

- Vitalis Organic Seeds

The Global Organic Seed Varieties Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 9.6 billion by 2034. This growth is being driven by increasing consumer awareness surrounding health, sustainability, and food security. As more people shift toward healthier lifestyles and environmentally conscious choices, the demand for organic seeds continues to rise. Organic farming is gaining momentum as a key strategy to preserve biodiversity, reduce chemical use, and promote resilient agricultural practices. Organic seeds, typically heirloom varieties or those well-suited to specific climates, contribute to food security by enhancing farmers' ability to grow crops in challenging environments. They also help to maintain seed sovereignty and are vital in maintaining genetic diversity in agriculture. Climate change has highlighted the importance of resilient crops that can endure unpredictable weather, further boosting the market.

Moreover, as concerns about sustainability and food security continue to rise, governments globally are intensifying their support for organic farming. This includes increased funding, grants, and policy initiatives designed to promote organic seed production and facilitate the transition toward eco-friendly agricultural practices. Such government backing plays a critical role in fostering the growth of the organic seed industry, encouraging both large-scale producers and smallholder farmers to shift towards organic farming methods. These efforts not only help ensure the long-term sustainability of agriculture but also support the broader goals of biodiversity conservation and reduced chemical usage in farming.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 6.1% |

The vegetable seed (seed companies to farmers) segment held a 35.2% share in 2024. This segment is projected to expand at a solid CAGR of 6.4% over the next decade, reflecting growing consumer preferences for organic, locally grown produce. As more individuals become health-conscious and seek chemical-free vegetables, both home gardeners and commercial farmers are increasingly turning to organic vegetable seed varieties. This trend is driving demand for vegetable seeds, which are considered essential for promoting better nutrition and healthier eating habits.

The direct sales segment was valued at USD 2.1 billion in 2024 and is expected to grow at a CAGR of 6.3% through 2034. This model is favored for its personalized service, allowing seed producers to offer tailored solutions that address the unique needs of individual farmers. By eliminating intermediaries, direct sales help ensure that customers receive products in a timely manner, fostering stronger relationships and higher levels of customer satisfaction. The ability to offer expert advice, logistical support, and customized delivery options also contributes to the success of direct sales, making it a preferred channel for both large-scale agricultural operations and smaller, independent farmers.

U.S. Organic Seed Varieties Market was valued at USD 1.5 billion in 2024. The demand for organic produce, coupled with favorable government policies and a strong organic supply chain, supports this growth. As organic farming standards become more stringent, many farmers are adopting organic seed production to comply with regulations, while seed companies continue to innovate and expand their product offerings. With large-scale agricultural operations and a growing number of organic farms, the U.S. market is poised for continued expansion.

The top players in the Global Organic Seed Varieties Market include Farm Direct Organic Seeds, Baker Creek Heirloom Seeds, Fedco Seeds, High Mowing Organic Seeds, and Johnny's Selected Seeds. To strengthen their position, companies in the organic seed varieties market are focusing on offering high-quality, locally adapted seed varieties that cater to specific environmental conditions and consumer preferences. Innovations in seed preservation and the development of new, resilient varieties are central to their strategies. Furthermore, companies are increasingly investing in research and development to improve seed yield and disease resistance. Many are also building stronger relationships with farmers through direct sales and providing personalized services to ensure farmers' needs are met. Environmental sustainability and supporting local economies have become key selling points for companies, as they appeal to both eco-conscious consumers and farmers looking for sustainable solutions.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Crop type

- 2.2.3 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 North America: organic consumers are increasingly mainstream

- 3.2.1.2 Europe: sustainable food production practices to boost the demand of organic seeds

- 3.2.1.3 Asia pacific: transformation towards organic agriculture practices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited organic variety availability

- 3.2.2.2 Price premiums and certification burden

- 3.2.3 Market opportunities

- 3.2.3.1 Crop diversification and niche market growth

- 3.2.3.2 Regional breeding and climate adaptation

- 3.2.3.3 Digitalization and direct-to-consumer channels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By crop type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Value chain analysis

- 3.13.1 Seed breeding and production

- 3.13.2 Certification and testing

- 3.13.3 Distribution and retail

- 3.13.4 End use segments (commercial growers, smallholders, home gardeners)

- 3.14 Sustainability and biodiversity

- 3.14.1 Role of organic seed in agroecology and food security

- 3.14.2 Biodiversity conservation initiatives

- 3.14.3 Seed sovereignty and local seed systems

- 3.15 Certification and regulation

- 3.15.1 USDA NOP certified organic seeds

- 3.15.2 EU organic certified seeds

- 3.15.3 Other national and regional certifications

- 3.15.4 Non-GMO verified seeds

- 3.15.5 Seed treatment and coating (Organic-Compliant)

- 3.15.6 Compliance costs and market impact

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Crop Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trend

- 5.2 Vegetable seeds

- 5.2.1 Lettuce

- 5.2.2 Tomato

- 5.2.3 Spinach

- 5.2.4 Carrot

- 5.2.5 Cucumber

- 5.2.6 Bell pepper

- 5.3 Grain seeds

- 5.3.1 Wheat

- 5.3.2 Corn

- 5.3.3 Rice

- 5.3.4 Barley

- 5.3.5 Oats

- 5.3.6 Millet

- 5.3.7 Quinoa

- 5.4 Fruit seeds

- 5.4.1 Melon

- 5.4.2 Watermelon

- 5.4.3 Strawberry

- 5.4.4 Berry varieties

- 5.5 Herb and flower seeds

- 5.5.1 Basil

- 5.5.2 Cilantro

- 5.5.3 Parsley

- 5.5.4 Sunflower

- 5.5.5 Zinnia

- 5.5.6 Marigold

- 5.6 Oilseed and alternative grains

- 5.6.1 Soybean

- 5.6.2 Flax

- 5.6.3 Buckwheat

- 5.6.4 Amaranth

- 5.6.5 Sesame

Chapter 6 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Litres)

- 6.1 Key trend

- 6.2 Direct sales (seed companies to farmers)

- 6.3 Retail channels (garden centres, farm supply stores)

- 6.4 Online sales and e-commerce platforms

- 6.5 Cooperatives and buying clubs

- 6.6 Wholesale and institutional buyers

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Litres)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East & Africa

Chapter 8 Company Profiles

- 8.1 Adaptive Seeds

- 8.2 Baker Creek Heirloom Seeds

- 8.3 Eden Seeds

- 8.4 Farm Direct Organic Seeds

- 8.5 Fedco Seeds

- 8.6 High Mowing Organic Seeds

- 8.7 Johnny's Selected Seeds

- 8.8 Kusa Seed Society

- 8.9 Quality Organic

- 8.10 Resilient Seeds

- 8.11 Seed Savers Exchange

- 8.12 Southern Exposure Seed Exchange

- 8.13 Victory Seeds

- 8.14 Vitalis Organic Seeds